The Real Silver Problem Is Refining

China controls the gate. The deficit is eating the buffer.

In a Zurich vault, a family office adviser stacks another pallet of silver bars. Six hundred miles south on a factory floor outside Milan, a solar procurement manager makes her third call this week trying to lock in refined silver paste before the next Chinese export window closes. Both want the same metal. Neither can get enough.

Watch this video goes beyond cyclical demand to explore the structural shift in the silver market:

Silver hit a record near 99 dollars an ounce earlier this year. It has pulled back and now trades around 79 dollars. Many analysts say it just followed gold higher in 2025 and is cooling off now. They point to solar makers switching to copper and say the industrial story is fading. They tell people to buy silver only if they want gold with extra volatility.

That view misses the real issue. The part almost no one is talking about is not demand. It is refining and who controls the gate.

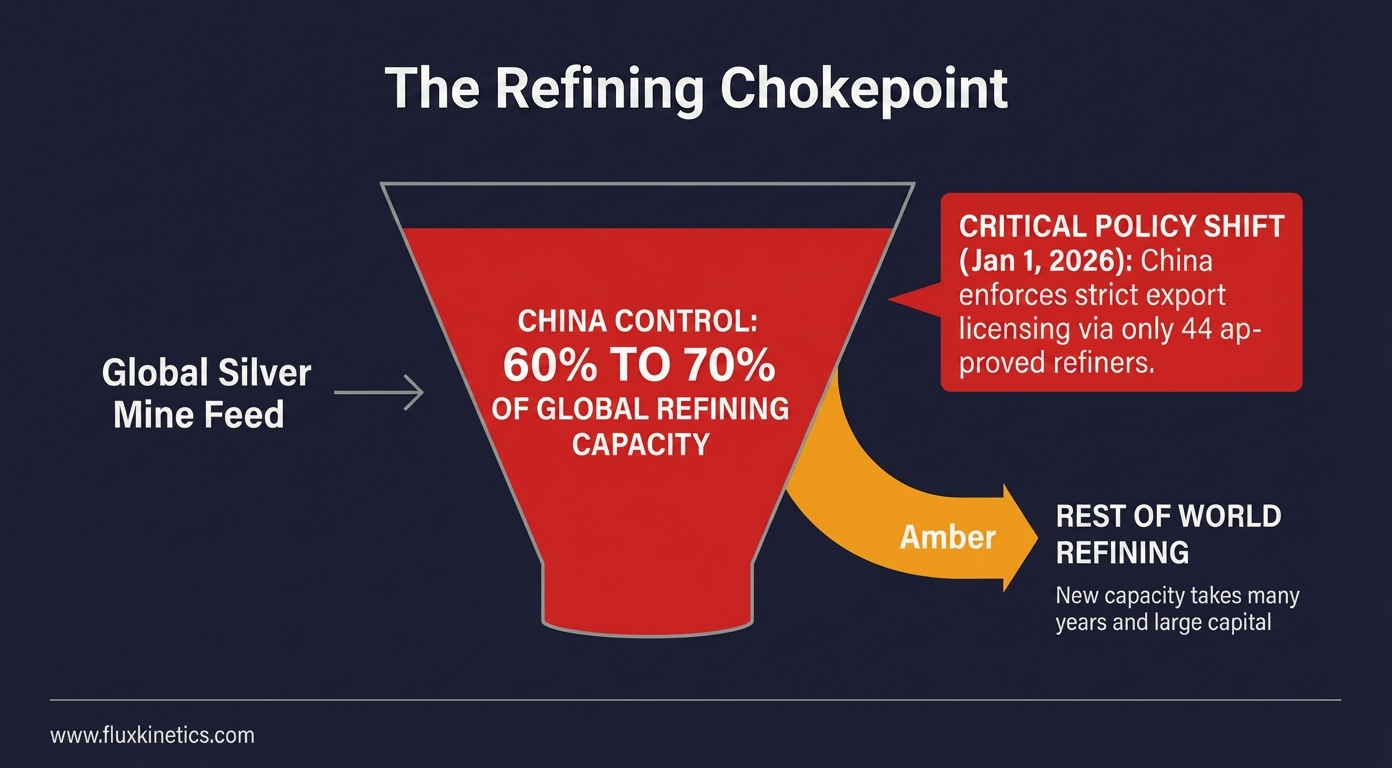

China produces up to 70 percent of the world’s refined silver. On January 1, Beijing replaced the old quota system with a strict export licensing regime. Only 44 approved companies can export refined silver now. This move treats silver like a strategic material similar to rare earths. You do not need a full ban to restrict supply. A licensing desk and a short list of names is enough.

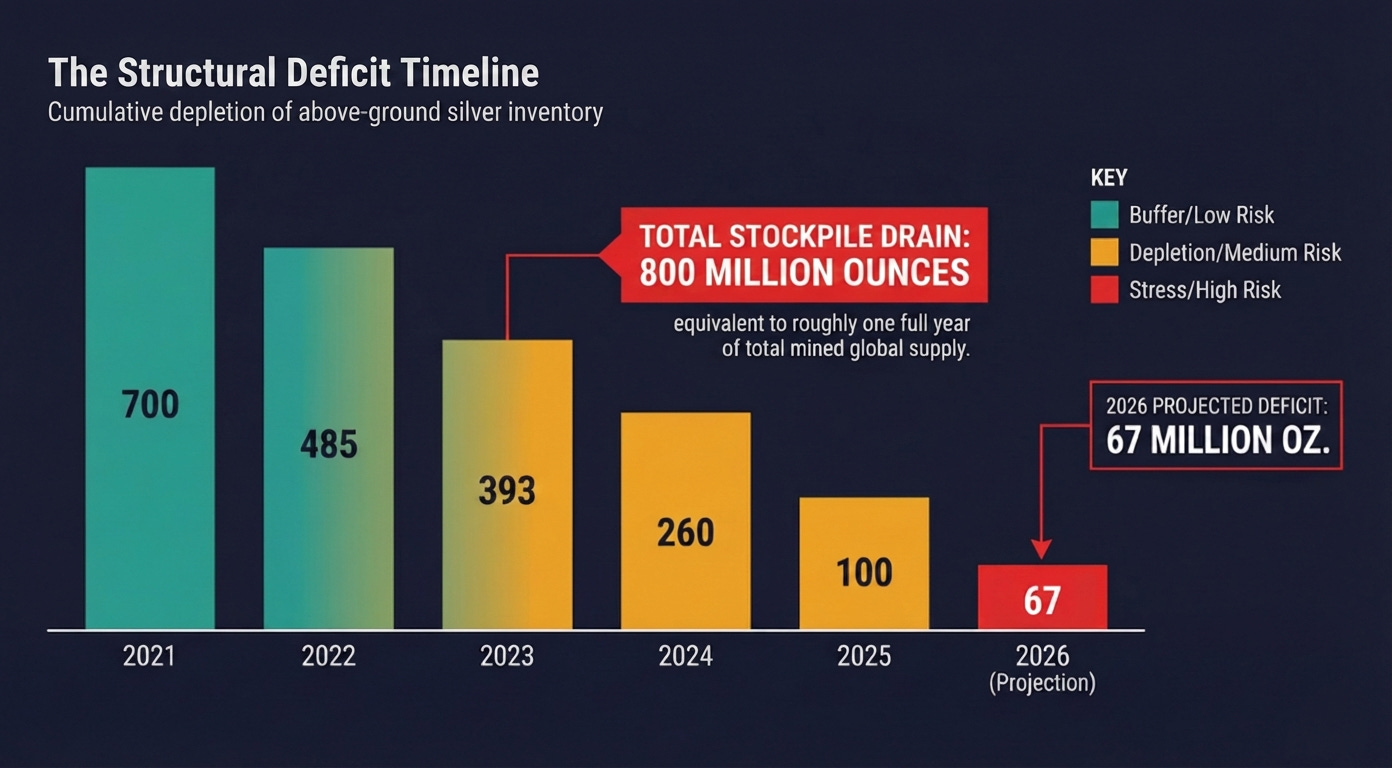

The global silver market has run a structural deficit since 2021. 2026 will be the sixth straight year of shortfall with a gap of 67 million ounces. That number sounds small next to total supply of roughly 1.05 billion ounces. It is not small.

From 2021 through 2025 the market pulled more than 750 million ounces from above ground inventories. That is nearly one full year of all silver mined worldwide. Those stocks are the buffer that keeps prices from swinging wildly. The buffer is shrinking fast.

Six years of deficits do not create a sudden shortage. They show the shortage was already building.

Mine production is expected to grow just 1 percent in 2026.

Recycling helps but will not close the gap.

New primary silver mines take five to ten years to start up.

The supply response to higher prices will take time. The United States added silver to its critical minerals list in late 2025. Building new refining capacity outside China will take years and a lot of capital. The bottleneck is already in place.

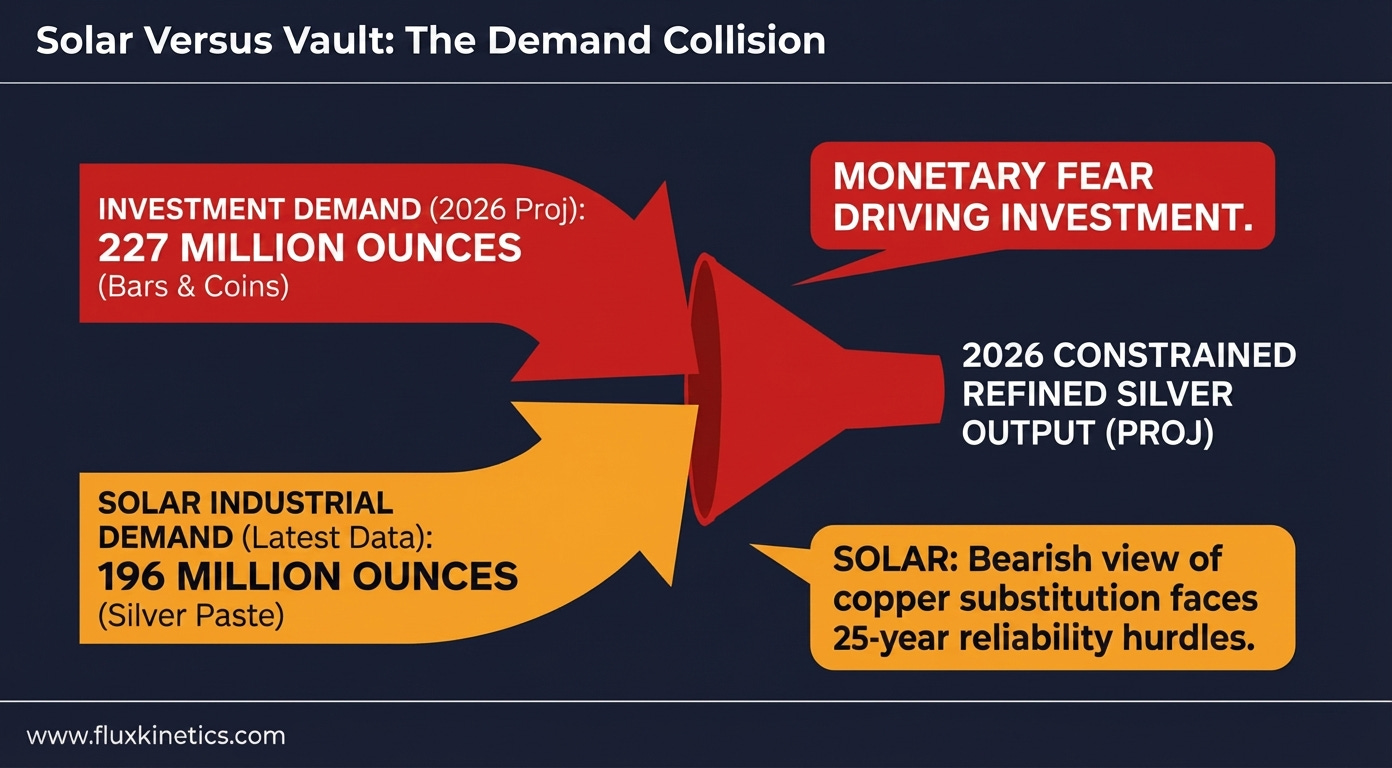

Industrial demand makes up about 59 percent of total silver use. The solar sector alone consumed roughly 187 million ounces in 2025 data. Silver paste carries electricity across solar cells and has become a big cost item.

Solar companies want to switch to copper to cut costs. Chinese firms like LONGi and Jinko are pushing hard on this. If it works they will save billions. The switch is not easy.

Copper oxidises fast.

Long-term reliability data for 25-year warranties is still limited.

Solar silver use may drop some but demand from data centers, EVs and power infrastructure keeps growing.

In case you’ve missed my previous article about Gold, read it now for Free:

Investment buying is rising too. Physical bar and coin demand is forecast to hit 227 million ounces this year. Industry and investors are competing for the same limited supply of refined silver.

The pressure shows up on the COMEX. Registered silver for immediate delivery has dropped sharply. Delivery requests are higher than normal.

In February, Wheaton Precious Metals signed a 4.3 billion dollar streaming deal with BHP for silver from a mine in Peru. Filings show it settles in metals credits. There is no physical delivery of bars to Wheaton. Even big players rely on paper structures. This makes the real physical limit at Chinese refiners even more important. Paper works until someone actually needs the bars.

Investors should look past the price screen, must map their exposure to separate the monetary safe-haven from the industrial reality.

If you hold physical bullion, physical-backed ETFs, or primary silver miners, you are playing the monetary narrative and stand to benefit from the supply squeeze.

If you own solar panel makers, grid hardware firms, or specialty chemical fabricators, you are exposed to the industrial reality. You are holding the companies that must pay whatever the refining gatekeepers demand to keep their assembly lines running. One side of your portfolio profits from the bottleneck. The other side pays for it. Know which one you own.

Watch these two signals :

The gold to silver ratio. A reading below 50 means silver is being valued as money.

Also track COMEX registered inventory. A drop below 70 million ounces is a red flag.

Silver is no longer just a volatile version of gold. It is a physical market pulled in two directions by investment demand and industrial need. The buffer is 750 million ounces thinner than five years ago. The main refining gate sits under government control that now lists silver as strategic.

This is a supply chain limit forming right now. It matters for solar costs and the speed of the energy shift.

Coming next:

The Gold To Silver Ratio As A Stress Gauge For The Energy Transition

The Real Economics Behind Small Modular Reactors (SMR)

Share this with that person who still thinks silver is just a volatile version of gold, and bring them into the conversation. That is who Flux Kinetics is written for.

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

China ran this exact script with rare earths in 2010. Quotas, restrictions, panic. Fifteen years later — same playbook, different metal.

What’s surprising nobody built an exit over six deficit years while there was still time.

The copper switch may trim demand. But the refining bottleneck holds regardless of what’s inside the panel. The gate is the gate.