Why Small Modular Reactor Economics Still Don’t Add Up

Hyperscalers are signing gigawatts. The fuel plant exists on paper.

Meta signed for 6.6 gigawatts in January. Oklo hasn’t poured concrete. Between those two facts sits the real SMR story of 2026, and it is not the one the press release cycle is selling.

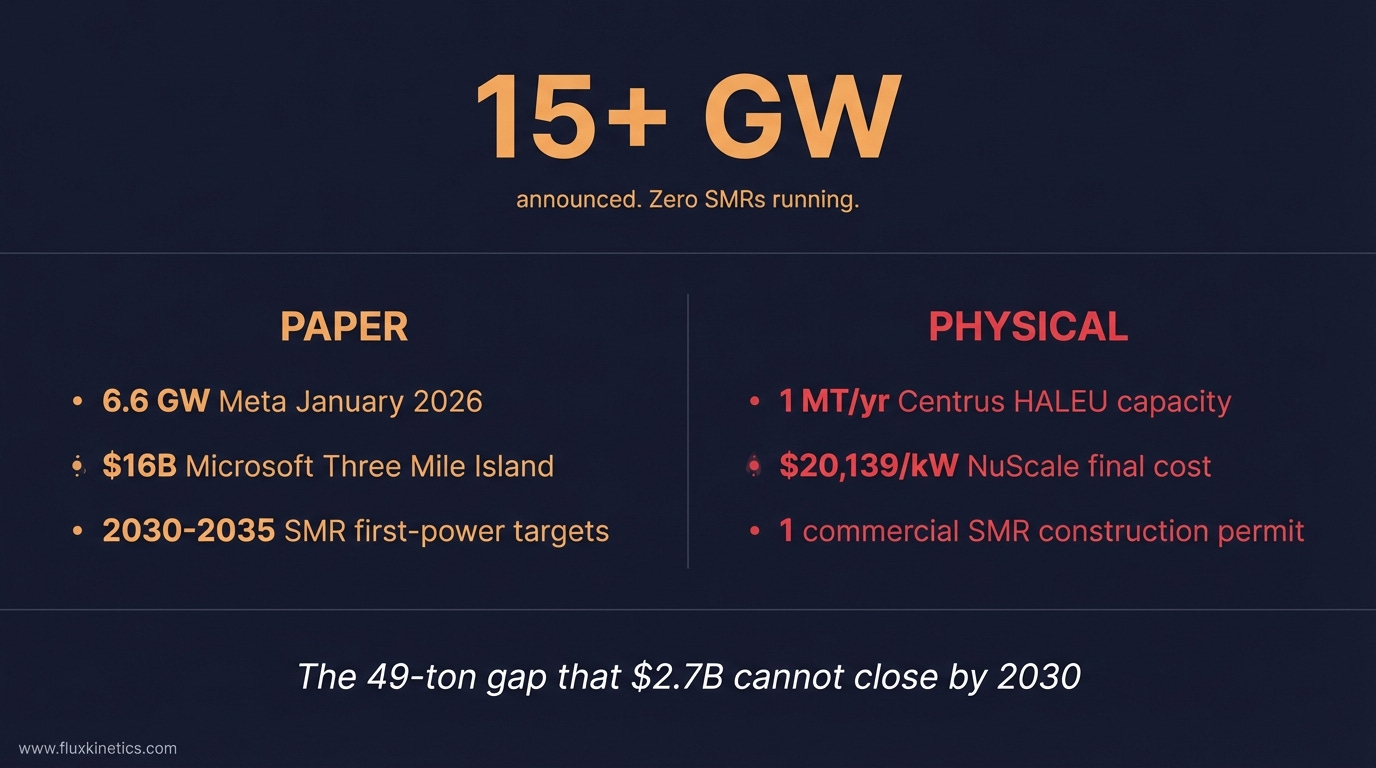

The Small Modular Reactor (SMR) industry has spent eighteen months converting hyper scaler balance sheets into nameplate announcements. Microsoft restarted Three Mile Island via Constellation for sixteen billion dollars. Amazon committed more than twenty billion to its Susquehanna campus plus equity in X-energy. Google took 500 megawatts of Kairos Power on paper for post-2030 delivery. Meta’s January 9 announcement bundled Vistra, Oklo, and TerraPower into a 6.6 GW two-decade frame. Add it all up and the hyper scaler nuclear book exceeds 15 GW of stated commitment…

Here is the catch. Roughly 9 GW of that book is what matters most to the SMR thesis specifically, and none of it has a running reactor. The comfortable story says capital has broken the nuclear logjam. The plumbing says capital has only rented optionality.

This piece covers the 2028-2032 window, because that is when paper PPAs either become physical electrons or become write-downs.

Watch how CNBC maps the AI-driven energy scramble that pushed Amazon, Microsoft, Google and Meta into nuclear power:

Brief contents

The NuScale number won’t go away

Where the capital is actually committed

The HALEU chokepoint in plain English

The LEU+ pivot nobody is pricing

The operator’s exposure matrix

“Hyperscalers are not buying electrons. They are buying optionality on electrons.”

The NuScale number won’t go away

NuScale Company’s overnight construction cost landed at $20,139 per kilowatt in its final 2023 estimate. That is within a rounding error of Vogtle, the large-reactor project in Waynesboro whose cost overruns the SMR industry was explicitly founded to escape. The target power price reached $89 per megawatt-hour with full federal subsidies, roughly $119 without. The Carbon Free Power Project was cancelled in November 2023…

That was the data point. The explanation is worse.

UAMPS, main costumer of this NuScal project, attributed the 75% construction cost escalation, from $5.3 billion to $9.3 billion, to commodity inflation in the supply chain. Fabricated steel plate rose 54% between 2021 and 2023. Carbon steel piping rose 106%. Copper wire and cable rose 32%. Interest rate assumptions added approximately 200 basis points to the project’s financing stack. None of those inputs have reset to 2020 levels. Steel is still elevated. Financing costs are elevated. The NRC regulatory pathway is marginally faster than 2023 but not dramatically so.

Watch how physicist Sabine Hossenfelder explains why small reactors still face the same cost problem that killed NuScale:

The industry response has been to argue that NuScale was first-of-a-kind, undersized at 462 MW post-downsizing, and architecturally inferior to newer designs. There is truth in each point.

An other major company developping SMR, Holtec, has publicly-cited SMR-300 construction cost range is $12-15 million per megawatt, which is $12,000 to $15,000 per kilowatt, 25% to 40% below NuScale’s final number: That is progress.

However, progress from a twenty-thousand-dollar kilowatt is not the same as proof of a four-thousand-dollar kilowatt. The IEA’s 2040 cost-parity target for US and European SMRs is $4,500/kW. That requires a 70-80% cost reduction from Holtec’s best-case directional number, in an environment where the structural steel supply chain remains tight and nuclear-grade fabrication capacity is capacity-constrained globally.

The industry call on that trajectory is possible. The ten-year operating history says unlikely.

“Progress from a twenty-thousand-dollar kilowatt is not the same as proof of a four-thousand-dollar kilowatt.”

Where the capital is actually committed

The hyperscaler deals break into two categories, and the press coverage rarely separates them.

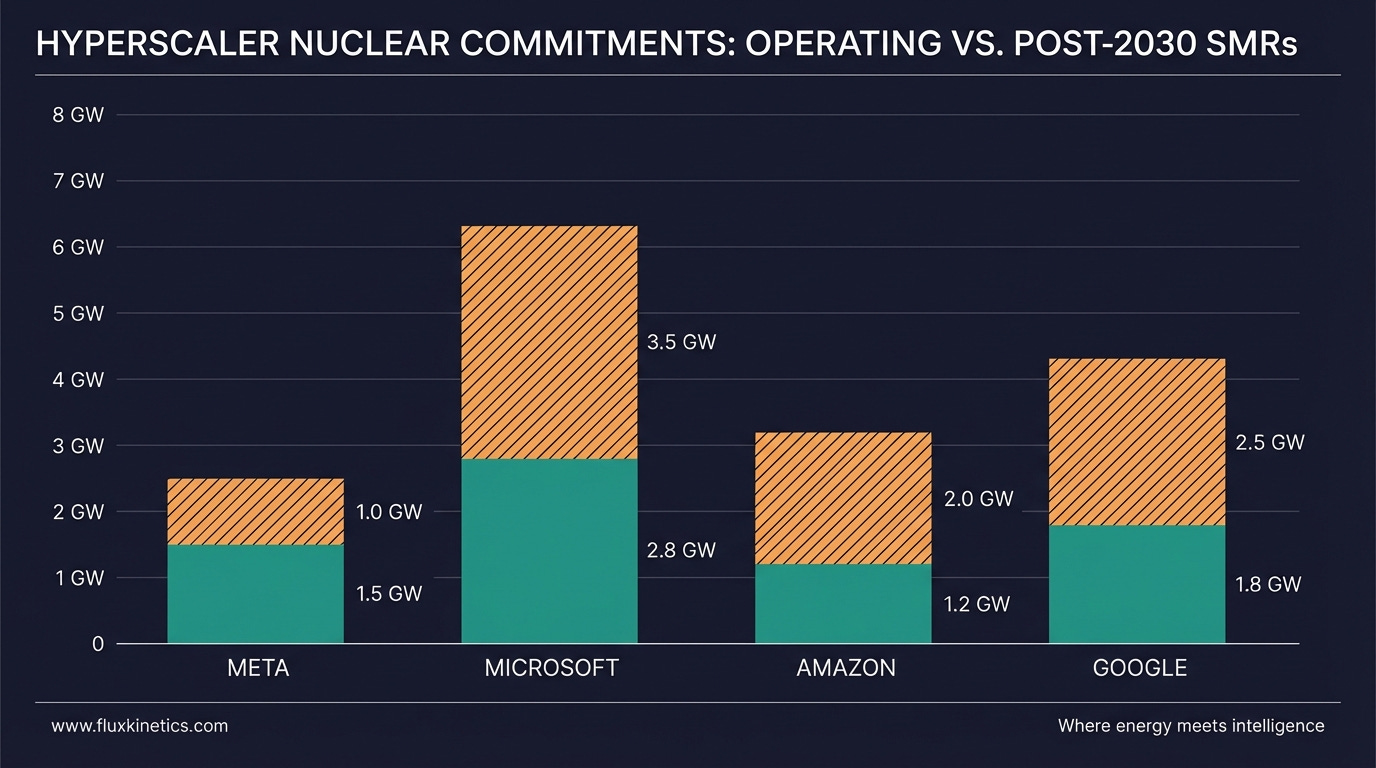

The first category is existing operating nuclear capacity. Microsoft’s Three Mile Island restart. Meta’s 2.2 GW purchase from Vistra’s Ohio plants, plus 433 MW of incremental plant upgrades. Google’s NextEra Duane Arnold reopening discussions. Amazon’s Susquehanna direct campus arrangement. These are near-term, commercially proven, and genuinely consequential for grid economics in PJM and MISO U.S regions.

📬 Never miss a signal

If this is your first time reading Flux Kinetics, every weekly note lands free in your inbox. No noise, no filler, just what actually moved the tape.

The second category is SMR-specific. Meta-Oklo for up to 1.2 GW with a 2030 first-reactor target. Meta-TerraPower for up to 2.6 GW across eight Natrium reactors with a 2032 first-power target. Google-Kairos for 500 MW post-2030. Amazon-X-energy, undisclosed final GW, post-2030.

Read together, these SMR-specific commitments total roughly 5-7 GW of announced hyperscaler capacity scheduled for 2030-2035 first power. None of the reactors have been built anywhere in the world on a commercial basis as of April 2026. TerraPower’s Natrium cleared its final NRC safety evaluation in December 2025 and received a construction permit in Wyoming in March 2026. That is the first commercial advanced-reactor construction permit issued in years and a genuine milestone. Oklo broke ground in September 2025 on a DOE Reactor Pilot Program, not a commercial unit.

The PPAs themselves are structured with deliberate looseness. Meta’s director of global energy, Urvi Parekh, told the Wall Street Journal the timelines are “challenging” and the agreements reflect willingness to be “bold.” Translation: these are optionality contracts, not take-or-pay pipeline commitments.

This is not a dig at the hyperscalers. It is how sophisticated counterparties with 12-figure cash flows buy 6-year forward energy optionality. They are not pretending otherwise. The sell-side coverage is.

The HALEU bottleneck in plain English

Approximately 90% of US advanced reactor designs run on HALEU (high-assay low-enriched uranium) enriched to between 10% and 19.75%, compared to 3-5% for conventional reactor fuel. HALEU enables the compact reactor designs, longer refueling cycles, and smaller footprints that make SMRs commercially interesting in the first place.

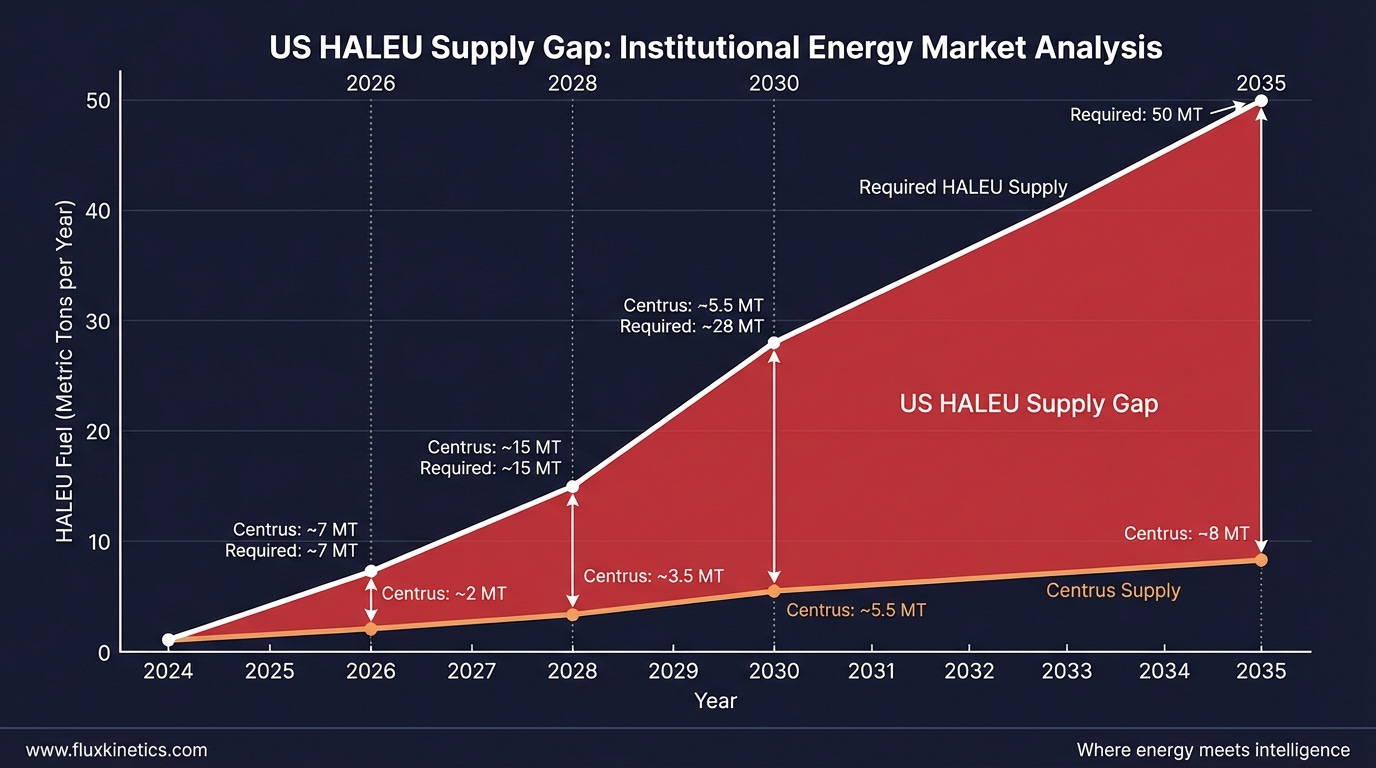

US commercial HALEU production capacity in early 2026: one metric ton per year, produced by Centrus Energy at its Ohio facility.

US HALEU demand forecast by 2035: 50 metric tons per year..

That is a 49 metric ton gap, and it does not close by writing checks.

The DOE announced a $2.7 billion nuclear fuel award in February 2026. Centrus, General Matter, and Orano Federal Services each received $900 million . The funding is directionally right. The physics is uncooperative. A new centrifuge cascade takes 3-5 years to construct, commission, and ramp. Regulatory approvals for HALEU fabrication facilities are more stringent than for conventional fuel. Each reactor design may require its own dedicated fuel fabrication plant.

Here is the part that is not in the bull-case decks. The US currently imports 71.7% of its enriched uranium. Russia supplies 24-27% of that total . The Prohibiting Russian Uranium Imports Act banned Russian LEU imports in May 2024 with waivers allowed through 2028. If waivers expire on schedule and domestic capacity has not filled the gap, the binding constraint on SMR deployment between 2028 and 2030 is fuel, not reactors.

That is a very bad sign for any investor who bought Oklo stock at today's highly inflated prices... just a thought.

The LEU+ pivot nobody is pricing

Here is the signal hidden in the filings.

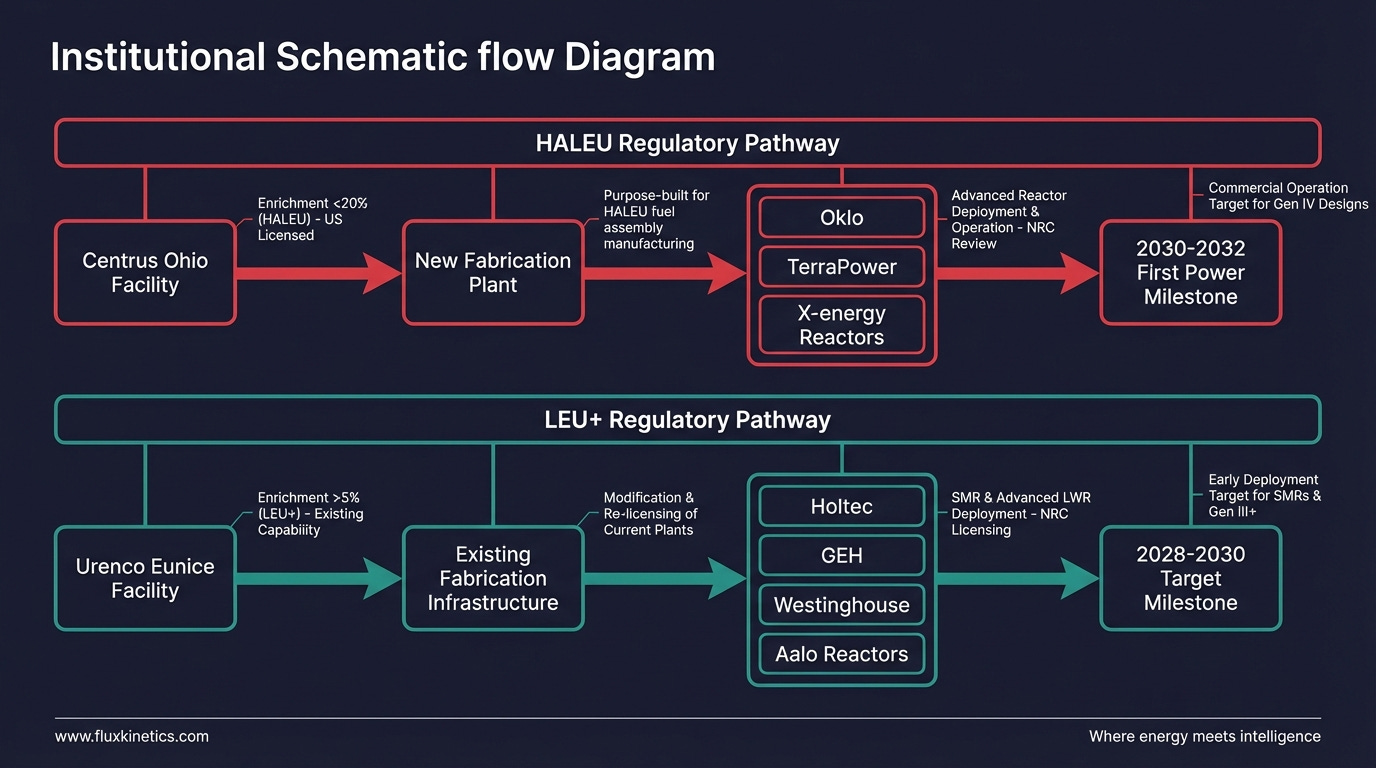

A quieter industry is moving in parallel. Holtec’s SMR-300, GE Hitachi’s BWRX-300, Westinghouse’s AP300, and Aalo Atomics’ commercial reactor all use LEU+, uranium enriched between 5% and 10%, a middle tier that leverages existing centrifuge infrastructure at Urenco’s Eunice, New Mexico facility.

Urenco USA received NRC authorisation for LEU+ production in September 2025 and expects to reach commercial production by mid-2026.

Westinghouse told Reuters Events that LEU+ reactors will have a supply-chain advantage “because the Nuclear Regulatory Commission (NRC) has already provided approval for LEU+ fuel designs, manufacturing and transportation for some enrichers and fuel vendors.” That is a consequential sentence. It means the regulatory tail risk that overhangs HALEU is absent for LEU+.

The implication is that the SMR industry is bifurcating. HALEU-dependent designs, Oklo, TerraPower Natrium, X-energy, face a genuine fuel-supply constraint through at least 2029. LEU+ designs face a far smaller fuel-supply constraint and a faster regulatory pathway for the fuel itself.

In case you’ve missed my previous article about current Silver Chockpoint :

The hyperscaler PPA book does not distinguish between these categories. The physical delivery schedules will.

I have been in enough project control rooms to know which side of that line I would want my money on.

“The regulatory tail risk that overhangs HALEU is absent for LEU+. The industry is bifurcating.”

The Flux Kinetics exposure matrix

If you are an investor, operator, or corporate buyer with capital at risk in this space, here are five diagnostics to implement taking into account current world situation:

Audit your fuel assumption. Pull the technical data sheet on any SMR you are exposed to. Confirm whether it runs on LEU, LEU+, or HALEU. If HALEU, read Centrus Energy’s most recent production capacity disclosure and compare to the reactor’s first-core requirement. If the first-core HALEU requirement exceeds Centrus’s published annualized capacity, you have a 2028-2030 fuel timing risk that is not in the sell-side model.

Separate paper PPAs from construction commitments. For any hyperscaler-nuclear deal you are trading, distinguish the GW secured against existing operating plants versus the GW contingent on SMRs reaching first power. If the SMR-contingent portion exceeds 60% of the announced total, the deal is mostly optionality.

Check the NRC construction permit status. As of April 2026, TerraPower’s Natrium in Kemmerer, Wyoming is the only commercial advanced-reactor construction permit in hand. Others are in queue. Treat permit-in-hand vs permit-pending as a bright-line risk tier.

Stress-test the commodity input deck. If your SMR financial model assumes 2020 steel prices or pre-2022 financing costs, it is not a model, it is a marketing document. Rebuild with current fabricated steel plate and carbon steel piping indices, plus 200 basis points of financing risk premium.

Track the LEU+ Urenco ramp as your tell. Urenco USA’s Eunice facility mid-2026 commercial production milestone is the single highest-signal deployment tell for the SMR industry between now and end-of-year. If it slips, LEU+ pivots slip with it and the bifurcation thesis weakens.

The close

Meta signed for 6.6 GW in January. Oklo hasn’t poured concrete. Those two facts will still be true in 2027, and probably in 2028. By 2029, the market will know which SMR designs actually ship fuel and which ones ship press releases.

Watch how the Wall Street Journal explains why US nuclear plants still depend on Russian enriched uranium, the fuel-security problem SMRs inherit:

The future hook runs like this. If Urenco USA hits commercial LEU+ production by mid-2026 and Holtec or GE Hitachi receives its first NRC construction permit by end-2027, the LEU+ cohort takes the commercial lead and the hyperscaler PPA book starts repricing around fuel availability rather than reactor nameplate. If either milestone slips more than 12 months, the entire SMR deployment timeline pushes to 2033+, and the Meta-Oklo-TerraPower paper capacity becomes accounting write-down risk for counterparty investors, not the hyperscalers themselves.

The thesis breaks if Centrus or General Matter hit 20+ MT/year HALEU capacity by 2028 on budget, or if a new enrichment technology clears commercial throughput inside 24 months. Neither is impossible. Both require that nuclear fuel physics finally cooperate with announcement cycles, which is not how it usually goes.

You are no longer reading the press release. You are reading the nuclear contract.

⚡ One last thing

If this changed how you see this topic, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm .

📨 Share • 📬 Subscribe • 💬 Leave a comment

Coming next:

The Gold To Silver Ratio As A Stress Gauge For The Energy Transition

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.