The truce was good news.

Here is why that makes things worse.

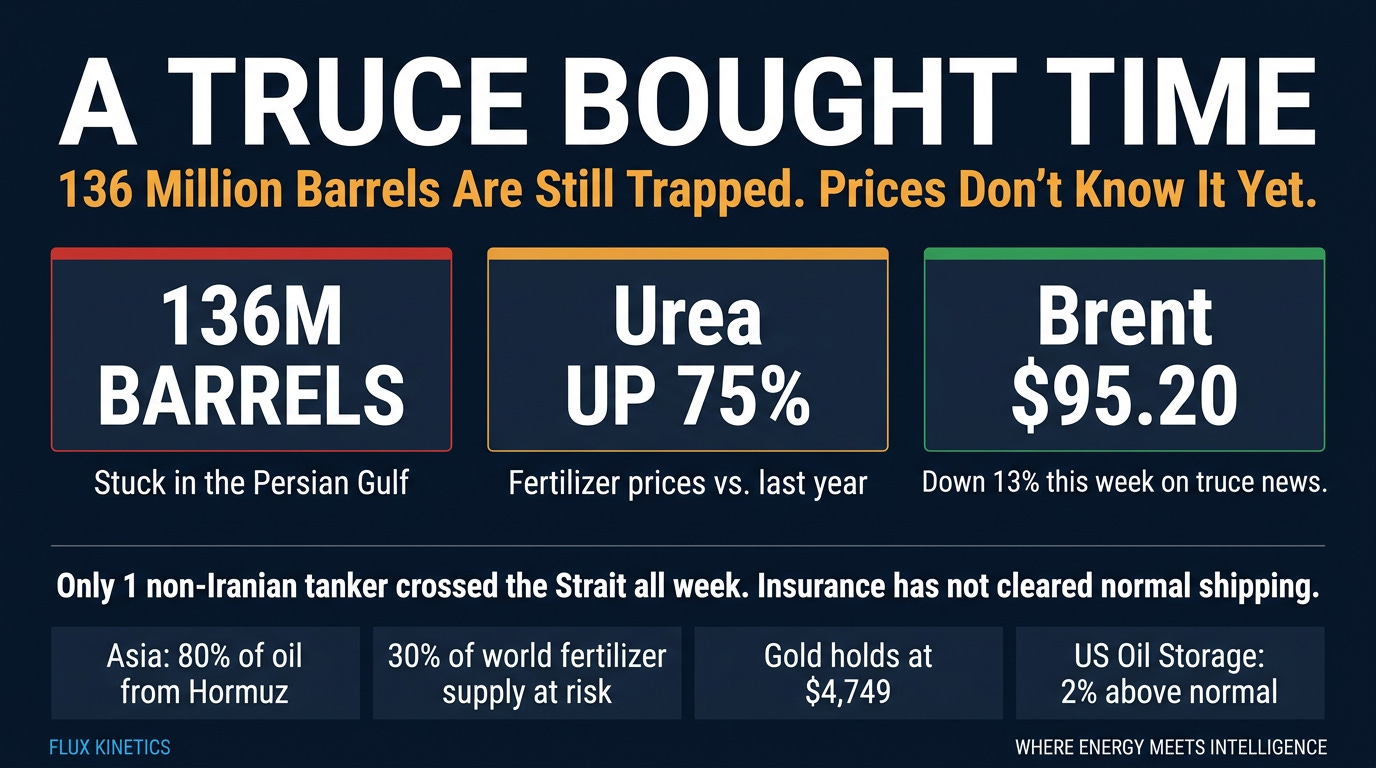

Vital Nitrogen nutrients and 136 million barrels of oil are still stuck, and that changes everything.

While the world watched oil prices crash this week, a much quieter,and potentially more devastating, crisis is brewing for global agriculture. The Strait of Hormuz isn’t just an energy chokepoint, its dictates the flow of roughly 30% of the world’s seaborne fertiliser(Qatar, Saudi, Iran). Right now, farmers desperately need nitrogen-based nutrients for planting season, but prices have already jumped sharply. Urea alone is up 75% from last year.

In case you have missed my previous deep dive about the Hormuz Food Stress:

Here is the part most people missed: even with a two-week truce on paper, almost nothing is actually moving. Only one non-Iranian tanker crossed the Strait all week. Insurance companies have not given the green light for normal shipping, leaving essential agricultural inputs, along with an estimated 136 million barrels of oil and fuel products, physically trapped in the Persian Gulf.

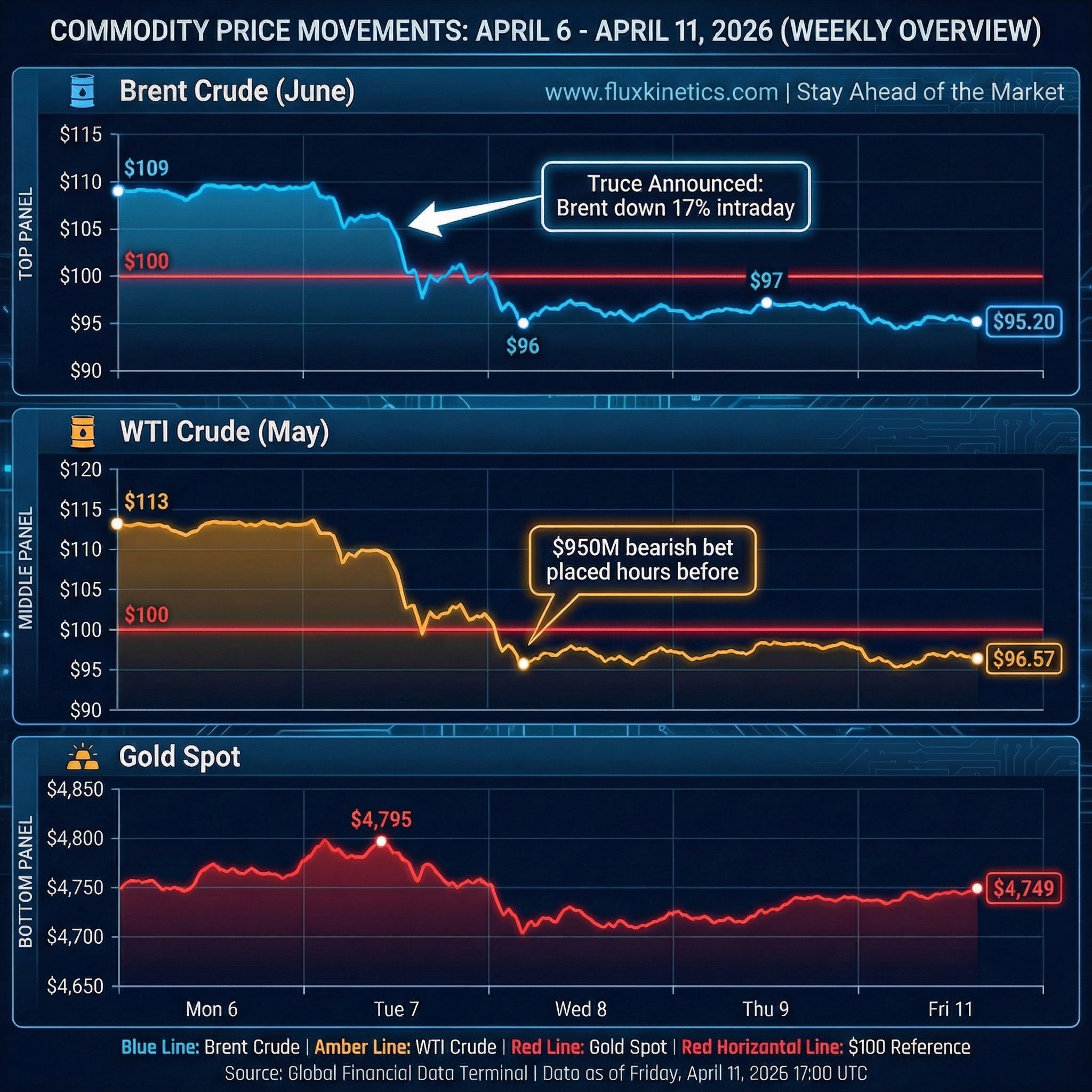

The truce gave financial markets hope, sending paper energy prices plummeting. Brent crude oil settled at $95.20 per barrel on Friday, down almost 13% for the week, and WTI closed at $96.57. But the real-world physical market has not caught up yet, and sustained bottlenecks for these trapped fertilisers will inevitably lead to higher global food prices.

Major banks like Goldman Sachs cut their price forecasts sharply. At the same time, U.S. oil storage tanks are filling up faster than expected. The government reported that commercial crude inventories rose by 3.1 million barrels to 464.7 million barrels, the seventh week in a row of increases. That is now 2% above the normal level for this time of year.

In simple terms: the paper price dropped hard on truce news. The actual supplies are still stuck, and tanks in the U.S. are filling up with oil that many refineries overseas cannot easily use.

This Week’s Settle:

Oil: Brent ended at $95.20. Only one non-Iranian tanker got through the blocked shipping lane, leaving 136 million barrels stranded.

Natural Gas: The main U.S. price (Henry Hub) fell to around $2.65. Meanwhile, the U.S. set a new record exporting 11.7 million tons of LNG in March.

Gold: Ended near $4,749 per ounce after hitting almost $4,800 earlier in the week. It tested the $4,700 support level three times and held.

Silver: Settled around $76.22 per ounce.

Lithium: The vital battery metal saw prices fall slightly to about $20,100 per tonne.

These numbers dictate everything from gasoline prices and heating bills to food costs and the price of goods relying on industrial metals

Oil for delivery soon is trading at a massive premium to oil for later in the year, a gap of about $14 to $22 on Brent and WTI. This structure usually indicates the market believes there is an immediate, severe shortage.

The type of oil is the crucial missing detail. The crude normally shipped through the Strait of Hormuz is heavier and sour, meaning it contains more sulfur. Many refineries across Europe and Asia are specifically built to process this exact grade. The oil currently building up in U.S. storage is lighter and sweeter. It is essentially the wrong fuel for their engines.

The Flux Kinetics Number: 136 million barrels.

That is the volume of oil and fuel still waiting behind the Strait. Until that number starts dropping, the lower prices flashing on trading screens will remain highly disconnected from physical reality.

The Strait of Hormuz Flow Map below illustrates how one narrow waterway dictates this flow. With agricultural impacts already making headlines, the energy shortage is running on a parallel track. Asia gets 80% of its oil from this exact route, meaning the physical freeze happening right now is setting the stage for massive supply chain disruptions globally.

The Insider View:

The U.S. has stepped into the role of the world’s swing supplier of natural gas through LNG exports, helping to fill gaps caused by damage in Qatar and the Hormuz disruption. However, pipeline capacity, not just export terminals, remains the real limiting factor.

U.S. LNG exports hit a record 11.7 million metric tons in March. That is 17.7% above February’s 9.94 million tons. The largest single month in U.S. history. Europe absorbed 7.49 million tons, roughly 64% of total U.S. shipments. The premium between European TTF and Henry Hub is so wide that every operational train in Louisiana and Texas is running at or above nameplate capacity.

Plaquemines LNG is the facility underneath the headline. Venture Global received DOE authorisation in March for a 13% increase in exports, adding 0.45 Bcf/d to its already operational capacity

Watch: Asia Gets 80% of Its Oil from the Strait of Hormuz. What’s Next? | WSJ

LNG export capacity is projected to more than double between 2024 and 2028, with exports expected to rise from 11.9 Bcf/d to 21.5 Bcf/d by 2030. The FID wave is real. The pipe to feed it remains the constraint.

Gold stayed strong and held above $4,700 despite the drop in oil. Central banks and Asian buyers continued to purchase on dips. Silver is currently playing two roles, acting as both a precious metal and a vital industrial component for solar panels and electronics.

My Flux Kinetics Trade:

I am treading carefully this week because geopolitical talks could swing prices wildly in either direction. With the next 10 days of negotiations, we might think that the market recovered and it will be calm, but we still have to be cautious.

I entered a long position in gold at $4,755 (futures contract), with a stop loss below $4,690 and a target of $4,950.

I entered this position because the short correction movement was still bullish; we didn’t make any lower low. Fortunately, we closed again up at $4,800 and we hold the $4700.

If you are not into any trade, and we break strongly above $4850, a momentum trade can be played toward the same target given previously at $4950.

If you want to be more patient, then I would buy a deep at $4600 with the stop loss at five $4500.

The Week Ahead:

April 14: The IEA releases its new report on global oil supply losses.

April 15: The next U.S. inventory report drops, reflecting the first full week after the truce news.

Strait Traffic: If several non-Iranian tankers start moving smoothly by mid-week, prices could fall further toward $90. If traffic stays frozen, $95 will likely hold as a floor, and we could retest the $100 mark.

The Investor’s Perspective

The gap between the $95 oil on your screen and the closed shipping lanes in reality is where the actual market story lives. Those looking for exposure might consider companies operating pipelines, storage facilities, or LNG terminals rather than taking direct positions on the price of crude. Energy infrastructure historically outperforms when physical delivery markets are chaotic.

For those following energy news, this situation shows how one narrow waterway can affect gasoline prices, fertiliser for farms, and even the cost of food at the grocery store.

If this changed how you see the week, send it to one person who needs to see it too.

Coming this week → Silver’s Two Masters: The Metal That Can’t Serve Both

Thanks for reading my work,

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

Everyone rushed to celebrate the truce while the oil headlines took over, but who’s actually tracking what this does to food supply chains? The agriculture angle feels like the story nobody wants to talk about yet..

The headlines shift and it creates the sense that something has been resolved.

Meanwhile, the actual system - ships, inputs, timing - runs on a different reality.

That disconnect is where most people get caught off guard ... and there does not seem to be any political wisdom that might redirect trajectory.