The Global Food Chokepoint

Why a Hormuz Blockage is also Caloric Crisis.

The Strait of Hormuz is 21 miles wide at its narrowest point. Twenty million barrels of oil flow through it daily. Everyone watches the crude. Nobody watches the nitrogen.

The prevailing read is that a Hormuz closure is an energy crisis. The market models oil spikes, European gas scrambles, and the world eventually paying more to move goods. The agricultural impact is treated as a secondary effect driven by diesel costs.

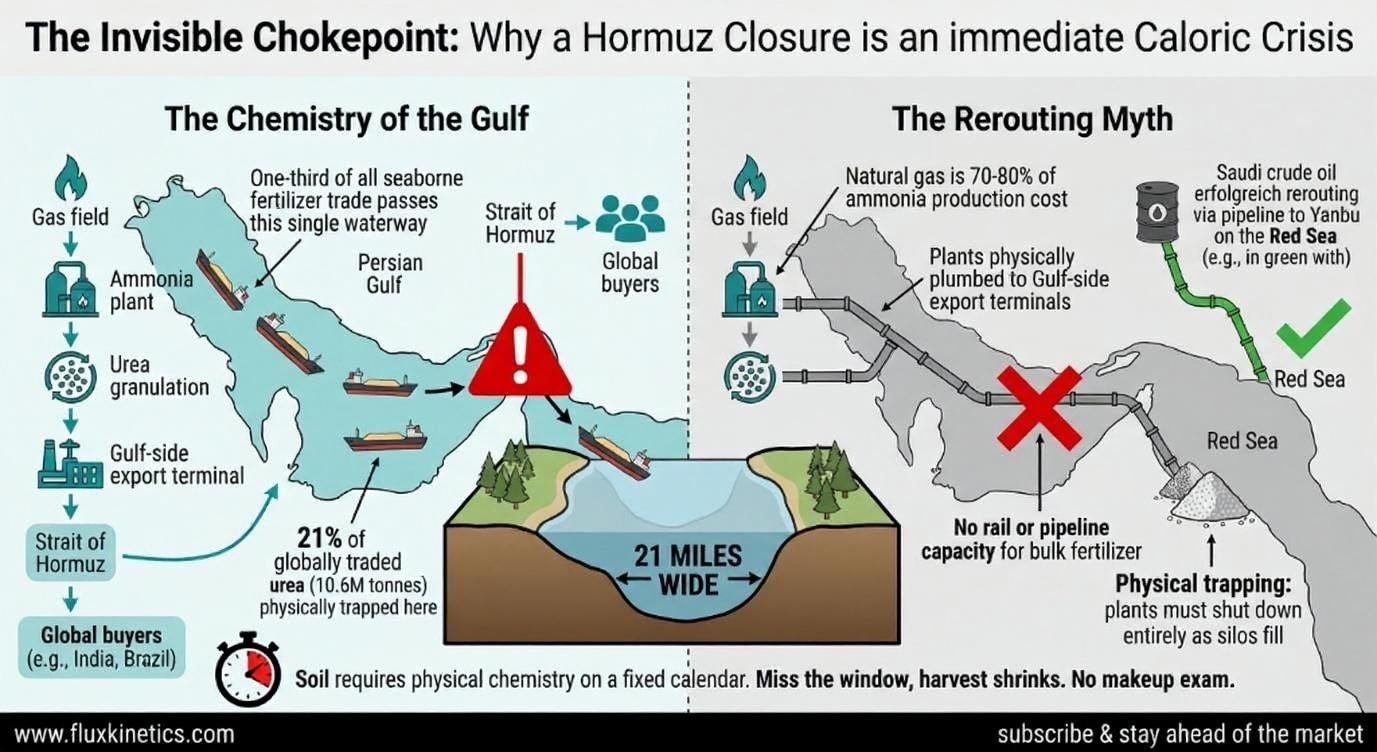

Here is what almost everyone misses. A Hormuz blockage is not just an energy shock. It is an immediate caloric crisis. The soil does not care about paper contracts. It requires physical chemistry on a fixed calendar. Miss the window and the harvest shrinks. There is no makeup exam.

Brief contents

The Chemistry of the Gulf

The Importer Squeeze

The African Backfill

The Capital Shift

The Exposure Matrix

The Chemistry of the Gulf

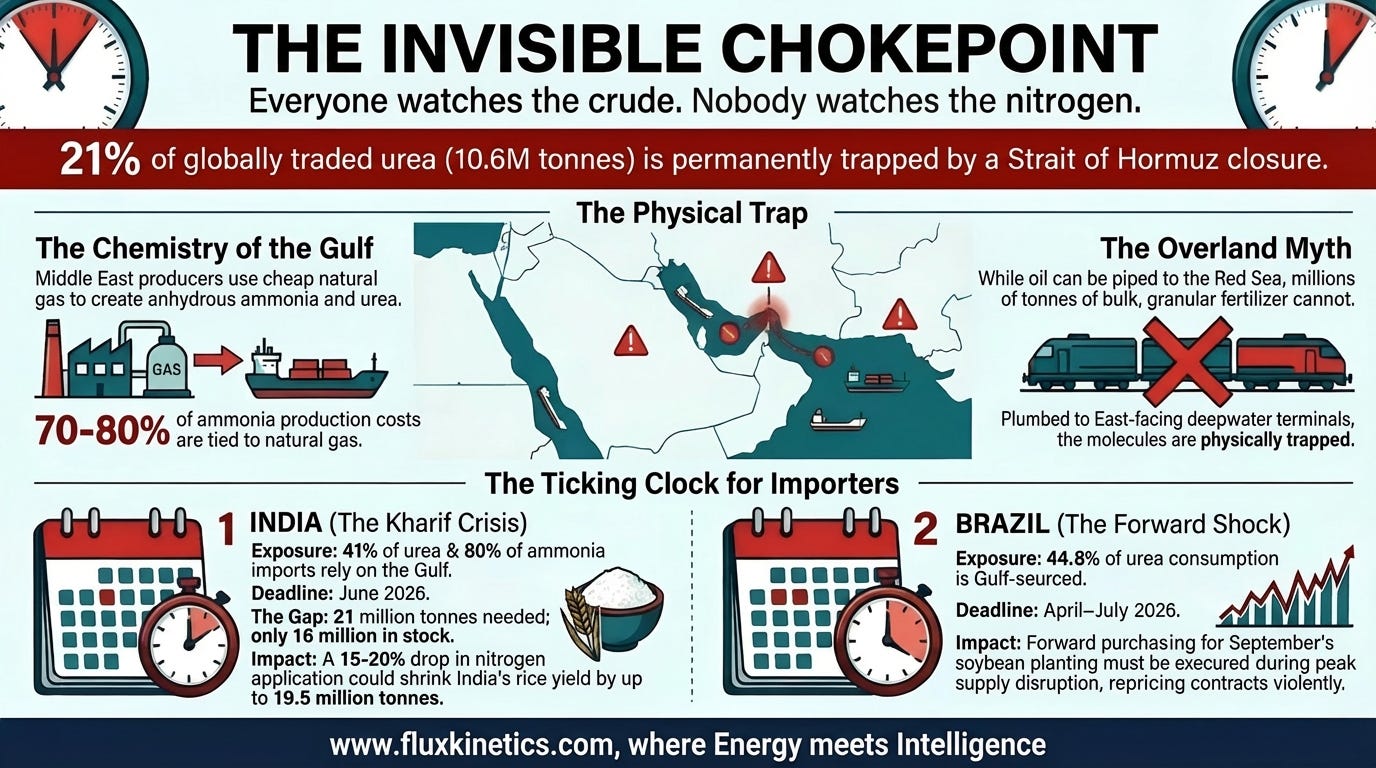

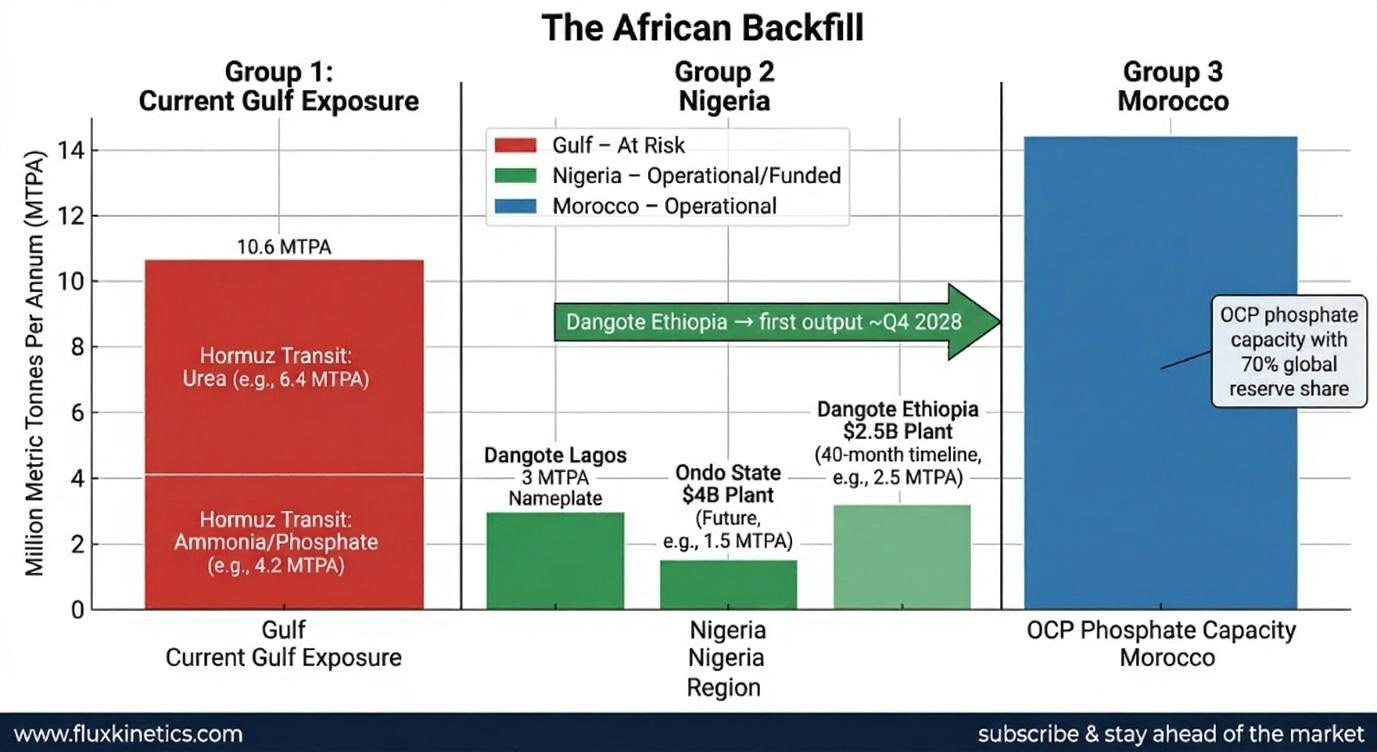

Middle Eastern nations turn cheap domestic natural gas into anhydrous ammonia. They upgrade that ammonia into urea. They load it onto dry bulk vessels and ship it through the Strait of Hormuz. One-third of all seaborne fertilizer trade passes through this single waterway, per the Carnegie Endowment (March 2026). For urea alone, the number is sharper: 21% of globally traded urea, roughly 10.6 million metric tonnes per annum, comes from Gulf exporters directly exposed to a Hormuz closure. That is per Rystad Energy’s 2025 trade mapping, published via OilPrice.com on March 31, 2026. The top three are Saudi Arabia, Qatar, and the UAE.

Natural gas accounts for 70 to 80% of ammonia production costs. The Gulf producers sit at the bottom of the global cost curve because their feedstock is the cheapest in the world. When you block the strait, you do not just delay shipments. You remove the baseline pricing anchor for global nitrogen.

Here is the part that makes it permanent until it reopens. The region’s ammonia and urea plants are physically plumbed to Gulf-side export terminals. There are no overland rail systems capable of moving millions of tonnes of granular urea to the Red Sea. Saudi Arabia can reroute crude oil through its Yanbu terminal on the Red Sea coast, and exports there have already surged to 4.6 million barrels per day. Fertilizer does not work that way. The processing plants, storage silos, and deepwater loading infrastructure are all east-facing. The urea is trapped.

The storage fill up within days once the export terminals choke. Plant operators must throttle back production or shut down entirely. India has already lost roughly 800,000 tonnes of its normal 2.6 million tonne monthly urea production because the government restricted industrial gas supply to the 70-75% range to conserve LNG stockpiles.

The plants are slowing. The molecules are not moving. The clock is running.

The Importer Squeeze

Follow the pipe. The ships leaving the Gulf head primarily to two places: India and Brazil. These are the two largest agricultural basins on earth that depend on imported nitrogen, and both are staring at a fixed planting calendar that does not negotiate.

Start with the numbers. India was the world’s single largest urea importer in 2025, bringing in 10.2 million metric tonnes. More than 41% of that was sourced from countries whose exports transit the Strait of Hormuz. India also sources close to 80% of its ammonia and sulfur imports from the Gulf region. Ammonia is the building block. Sulfur is used to produce phosphate fertilizers. Both are now bottlenecked.

The calendar is the weapon. India’s kharif season, the main monsoon planting window for rice, cotton, and pulses, requires urea to be in warehouses by June. The Indian government expects total kharif fertilizer demand of 39 million tonnes. Current stocks are 18 million tonnes. The gap is 21 million tonnes. The government has already pulled forward global tenders, ordering 13.5 lakh tonnes (1.35 million tonnes) of urea by mid-February and scrambling to source replacements from Russia, Belarus, and Morocco. However, the physical distance dictates the delay. You cannot reroute millions of tonnes from the Atlantic basin without paying current extreme freight premiums and waiting weeks for vessels to reposition.

Now look at the price. Urea FOB Middle East futures settled at $750 per tonne on April 1, 2026. That is up 74% year-over-year. In the US, NOLA barge urea prices rose from an average of $475/tonne in late February to $520-$550/tonne within the first week of the closure. The University of Illinois farmdoc daily team documented a 28% urea price increase in just the first three weeks after the closure began, noting it was faster than the response to the 2022 Russia-Ukraine fertilizer shock.

Brazil is the other exposed basin. In 2023, 44.8% of Brazil’s urea consumption came from Gulf sources transiting Hormuz. Brazil’s safrinha (second-season) corn crop, which represents roughly 80% of total corn production, was planted through February and March. That crop has already absorbed fertilizer, the bigger problem is forward purchasing. Brazilian farmers buy nitrogen for the next soybean cycle (September planting) during April through July. If Gulf supply remains offline through Q2, those purchase contracts will reprice violently.

To put this in caloric terms: if Indian farmers apply 15-20% less nitrogen this kharif season, rice yields fall by a roughly proportional amount. India produces around 130 million tonnes of rice annually. A 15% yield decline is 19.5 million tonnes. India consumes most of its rice domestically. That math does not work for a country of 1.4 billion people without triggering either government subsidy escalation or food inflation.

The African Backfill

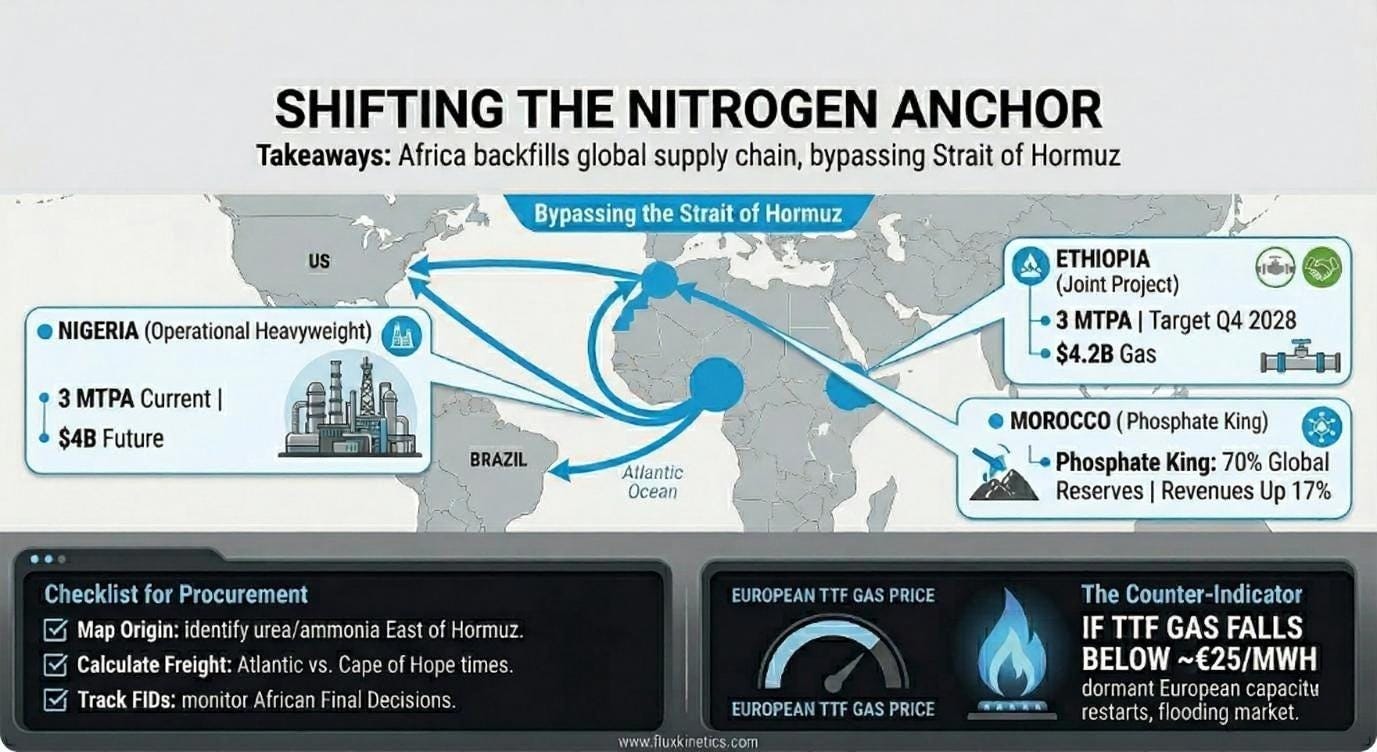

Capital goes where the molecules are. And right now, the molecules that bypass the Strait of Hormuz are in West Africa and North Africa.

Start with Nigeria. The Dangote Fertiliser plant in Lagos is Africa’s largest granulated urea facility, with a nameplate capacity of 3 million metric tonnes per annum. The company exports roughly 37% of its output, with the United States as a major destination.

Demand has surged since the Hormuz closure: “Demand has increased significantly because of shortages in the international market,” said Devakumar Edwin, Vice President of Dangote Industries, in a March 2026 interview with Bloomberg.

We need to keep in mind that nameplate capacity is not the same as deliverable supply, and this is where the opportunity gets specific. Dangote’s Lagos plant has been running below full capacity due to intermittent domestic gas supply. Nigerian port congestion at Apapa and Tin Can Island adds 7-14 days of delay to vessel loading. These are real bottlenecks. The current crisis creates the financial incentive to solve them because the price premium now justifies the infrastructure investment which is already arriving.

In February 2026, Ondo State signed an MOU with Resident Fertiliser for a $4 billion petrochemical fertilizer plant in Nigeria’s southern senatorial district . That is on top of Dangote’s $2.5 billion joint venture with Ethiopian Investment Holdings to build a second 3 million MTPA urea plant in Gode, Ethiopia, with completion targeted within 40 months (signed August 2025). This is not speculation. These are signed agreements with disclosed dollar amounts and timelines. Dangote has publicly stated the continent will be self-sufficient in fertilizer within 40 months (June 2025).

Now look at Morocco: OCP Group controls approximately 70% of global phosphate rock reserves. Morocco is not a nitrogen play. It is a phosphate play. The Hormuz closure affects phosphate too: 16.9% of India’s DAP/MAP consumption and 19.6% of America’s DAP/MAP supply came from Gulf sources in 2023. Morocco has the reserves, the processing infrastructure, and the Atlantic coastline to backfill that volume without touching the Strait of Hormuz. OCP reported revenues up 17% in 2025, reaching MAD 114 billion.

This thesis has a vulnerability. It sits on gas prices. If North American or North African natural gas experiences a rapid structural collapse, dormant European ammonia capacity could restart. The EU cut ammonia production by 70% temporarily in Q4 2021 when gas prices spiked. Many of those plants remain mothballed. If European TTF gas drops below the restart threshold, that idle capacity floods the market. That would blunt the Gulf supply shock and weaken the African backfill thesis. Watch European TTF gas as the key counter-indicator.

The Capital Shift

The shift is physical and it is documented.

India is in active talks with Russia, Belarus, and Morocco to diversify fertilizer imports away from the Gulf. India’s RCF has already extended its latest urea tender load date by 30 days due to the Hormuz closure. The government has extended Indian Potash Ltd’s State Trade Enterprise status for urea imports through March 2027. These are not analyst projections. They are procurement actions taken by a sovereign government racing a planting calendar.

On the production side, Dangote Fertiliser is fielding a surge in orders. The Ondo State deal signals a second major Nigerian production hub. The Ethiopia plant, backed by a $4.2 billion gas supply agreement signed in March 2026, adds another 3 MTPA by roughly Q4 2028.

Meanwhile, the headline energy capital remains focused on Permian Basin consolidation. Devon Energy and Coterra Energy are working through a $57 billion merger. That deal gets the front pages. The $4 billion Ondo State fertilizer plant and the $2.5 billion Dangote Ethiopia plant do not. But the physical operators, the trading houses that move actual molecules, are positioning in Africa because they know the chokepoint is fragile and the planting calendar is fixed.

The Exposure Matrix

This is the operational section. If you run procurement for an agricultural company, a food manufacturer, or a sovereign import agency, here is your checklist. It is specific.

Map your nitrogen origin. Pull your supplier manifest. Identify any urea or ammonia molecules originating east of the Hormuz chokepoint. Per the NDSU data, here is your direct exposure by product: if you are sourcing urea for the US market, 17.1% of national consumption transits Hormuz. For Brazil, it is 44.8%. For India’s ammonia, it is 80.6%.

If you do not know your percentage, you are already behind.

Stress test the transit route. Calculate the cost of replacing your Gulf-sourced volume from the Atlantic basin. The freight spread between West Africa and the Persian Gulf is the critical variable. As of early April 2026, Dangote’s Lagos facility is the closest large-scale Atlantic-basin urea source to both the US Gulf Coast and Brazilian ports. Calculate vessel repositioning time. For a Supramax from Lagos to NOLA, estimate 18-22 days. From the Arabian Gulf to NOLA (via Cape of Good Hope, since Suez is still available but freight rates are elevated), estimate 35-45 days.

Track the calendar deadlines. These are the dates that turn a supply disruption into a yield crisis:

India kharif urea stocking deadline: bulk must be warehoused by end of May 2026 for June-July application. The government says 18 million tonnes are in stock against 39 million tonnes of demand. The gap closes or it doesn’t.

Brazil soybean input purchasing window: April through July 2026. Forward contracts for September planting will reprice based on spot urea availability during this window.

US corn belt spring application: underway now through May. US exposure is moderate (17% of urea, 20% of DAP/MAP from Gulf) but NOLA barge prices are already up and climbing.

Track the African FIDs. Monitor Final Investment Decisions for West African and East African gas-to-fertilizer projects. These are the dates that signal when structural relief actually arrives:

Dangote Lagos expansion→ ongoing, details undisclosed. Current 3 MTPA plant running below capacity. Any gas supply improvement increases output immediately.

Dangote Gode, Ethiopia→ $2.5 billion, 3 MTPA. Signed August 2025. $4.2 billion gas supply deal signed March 2026. Target completion: ~40 months from commencement, approximately Q4 2028.

Ondo State (Resident Fertiliser)→ $4 billion MOU signed February 2026. No construction start date disclosed. Monitor for FID and groundbreaking.

Model the counter-scenario. European TTF natural gas price is your single most important counter-indicator. If TTF drops below roughly EUR 25/MWh on a sustained basis, mothballed European ammonia plants become economically viable to restart. That flood of Western production would ease the supply shock and reduce the premium on African and Atlantic-basin sourcing. As of early 2026, European ammonia production remains at depressed levels following the 2021-2022 gas crisis, with many plants still offline.

We are entering a period where agricultural yields are tied directly to maritime security. The consensus models the oil. The operators track the urea.

You are now looking at the global food system through the lens of physical chemistry.

Share this with the procurement officer who still thinks urea pricing is just a number that follows natural gas.

In case you have missed my previous article about the Pump Price rise and decline :

Coming next:

Silver’s Two Masters: The Metal That Can’t Serve Both

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

The argument that a Hormuz closure is a caloric crisis before it's an energy crisis deserves more attention than it gets in mainstream coverage and you make it with real specificity. Loved this piece.🌟

EEK!!!