The Death of the Old Model. Part 2.

Gold’s New Structural Floor, from FX Hedge to Regime Hedge.

In part 1, we established why the old pricing model is dead. Now we look at where that takes us.

Haven’t read part 1 yet? Go there first, then come back :

Because the central banks buying this metal are not just changing the price. They are actively breaking the physical plumbing of the paper market. Gold has moved from the “diversification” column on the reserve manager’s spreadsheet to the “survival” column. And survival requires physical possession.

The freezing of foreign assets forced a permanent rethink of what constitutes a safe haven, sparking a run on physical commodities.

Watch how Credit Suisse’s Zoltan Pozsar predicted the birth of a commodity-backed monetary order in early 2022:

What this piece covers

The paper illusion vs. physical reality

The vault drain: Repatriation as a weapon

Bilateral settlement and the opaque consequence

The reserve crossover

Chokepoints, capital, and the sovereign hardening thesis

The exposure matrix

The paper float is draining. The dip-buyer is now the state.

The Paper Illusion vs. Physical Reality

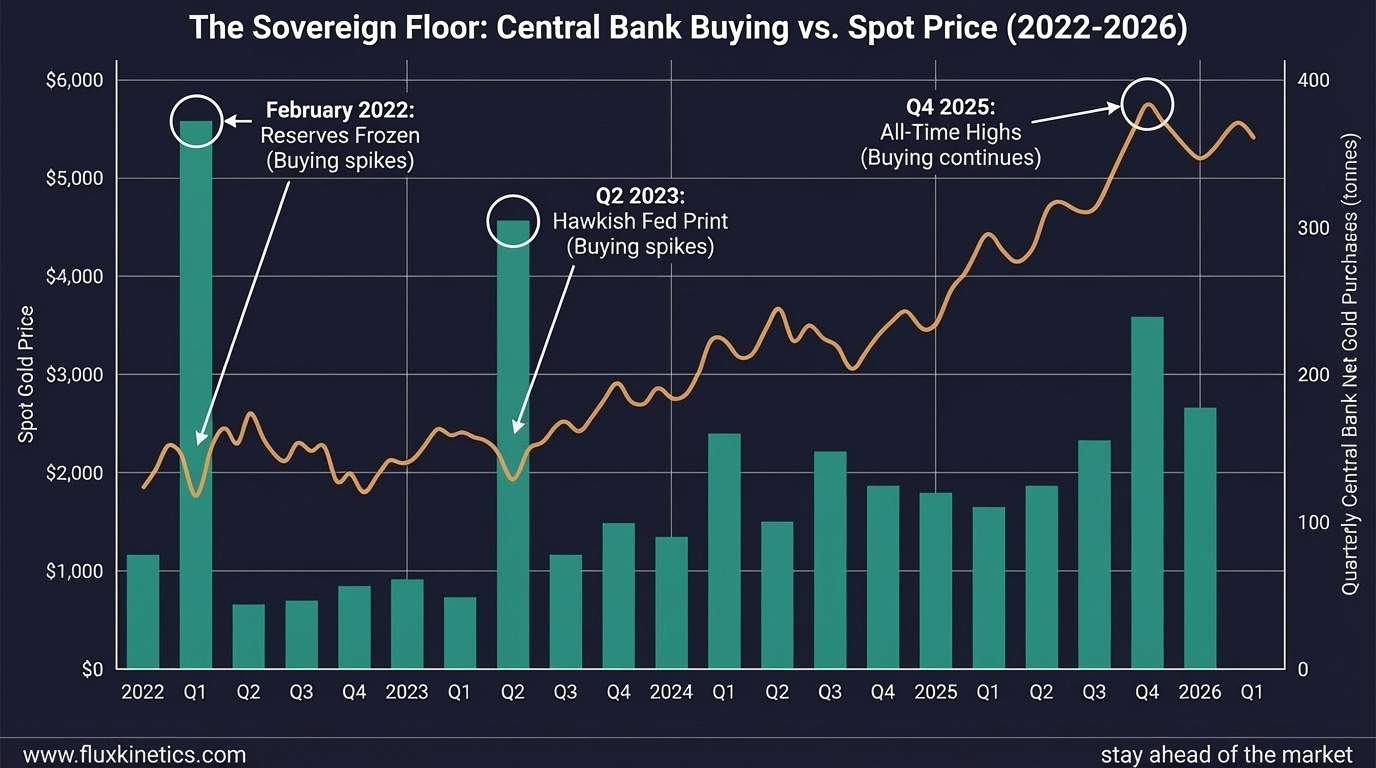

Central banks bought 863 tonnes of gold in 2025. But the question every institutional allocator should ask is not “how much are they buying?” It is “what kind of buyer is this?”

An ETF buyer is price-sensitive, momentum-driven, and can liquidate in an afternoon. A central bank buying gold for national security does not sell on a 5% drawdown.

This changes the architecture of corrections. Before 2022, gold corrections found support where marginal physical buyers and Asian jewellery demand kicked in. Now, corrections find support where sovereign reserve managers see value. When the paper market tries to trade down on a hawkish Fed print, the state steps in to accumulate.

That floor is higher, stickier, and far more aggressive.

“The buyer that sets the floor is not the buyer that sets the headlines. The state buys on dips. The ETF buys on momentum. Know which one you are trading against.”

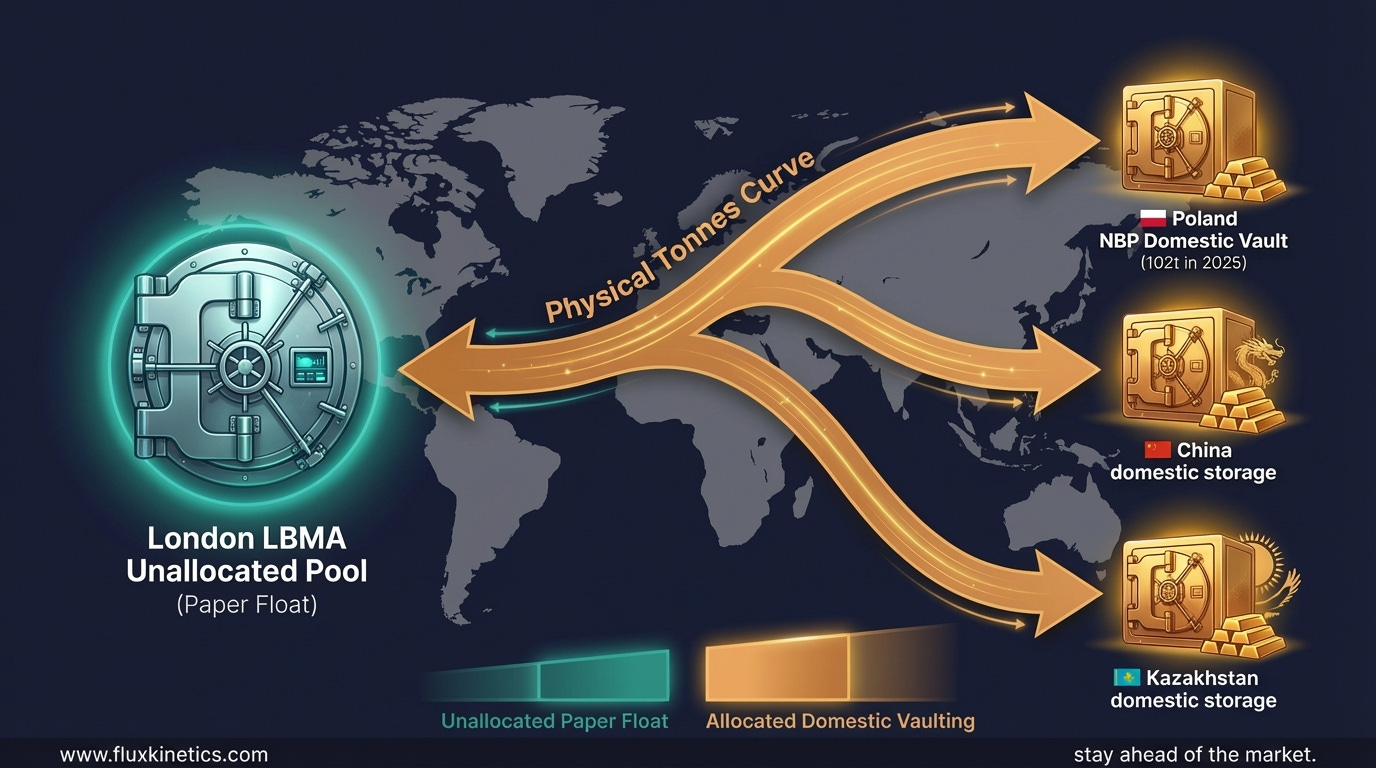

The Vault Drain: Repatriation as a Weapon

The non-negotiable chokepoint of the global gold trade is the LBMA unallocated float. This is the pool of gold in London vaults that backs the paper market. It functions like fractional reserve banking for bullion: multiple claims exist against each physical bar. As long as most holders never call for delivery at the same time, the system works.

But sovereigns are calling for delivery.

They no longer trust foreign custody. The story isn’t just that Poland is targeting 700 tonnes. The story is that Poland is building out domestic vault capacity in Warsaw to hold it. Kazakhstan is storing its record 57-tonne haul domestically. When Brazil bought 43 tonnes in three months, it didn’t leave those bars sitting in a London vault.

Every tonne repatriated to a domestic vault is a tonne permanently removed from the float that lubricates the paper gold market.

When trust in the global financial system fractures, governments rush to pull their physical assets out of the jurisdiction of their rivals.

Watch how the global market executed a massive logistical scramble to repatriate sovereign metal in mid-2023:

If official sector buying stays above 800 tonnes per year and an increasing share moves to domestic custody, the float drains. Not overnight. Slowly. Then all at once.

Bilateral Settlement and the Opaque Consequence

As we established in Part 1, Trading Economics data flagged that 57% of 2025’s central bank purchases were unreported.

Here is the mechanical consequence of that opacity: Bilateral settlement.

More than half of official-sector demand is now bypassing the traditional clearinghouses. It does not flow through COMEX. It does not hit the LBMA. It settles government-to-government, refinery-to-central-bank.

Mine production in 2025 was 3,672 tonnes. Growth runs at roughly 1% per year. Total supply, including recycling, was 5,002 tonnes. When you subtract the massive ETF inflows and retail bar/coin demand, the physical market is tightening in a way that no paper instrument can relieve. The market is pricing gold with incomplete demand data, right up until a physical supply squeeze forces a gap up.

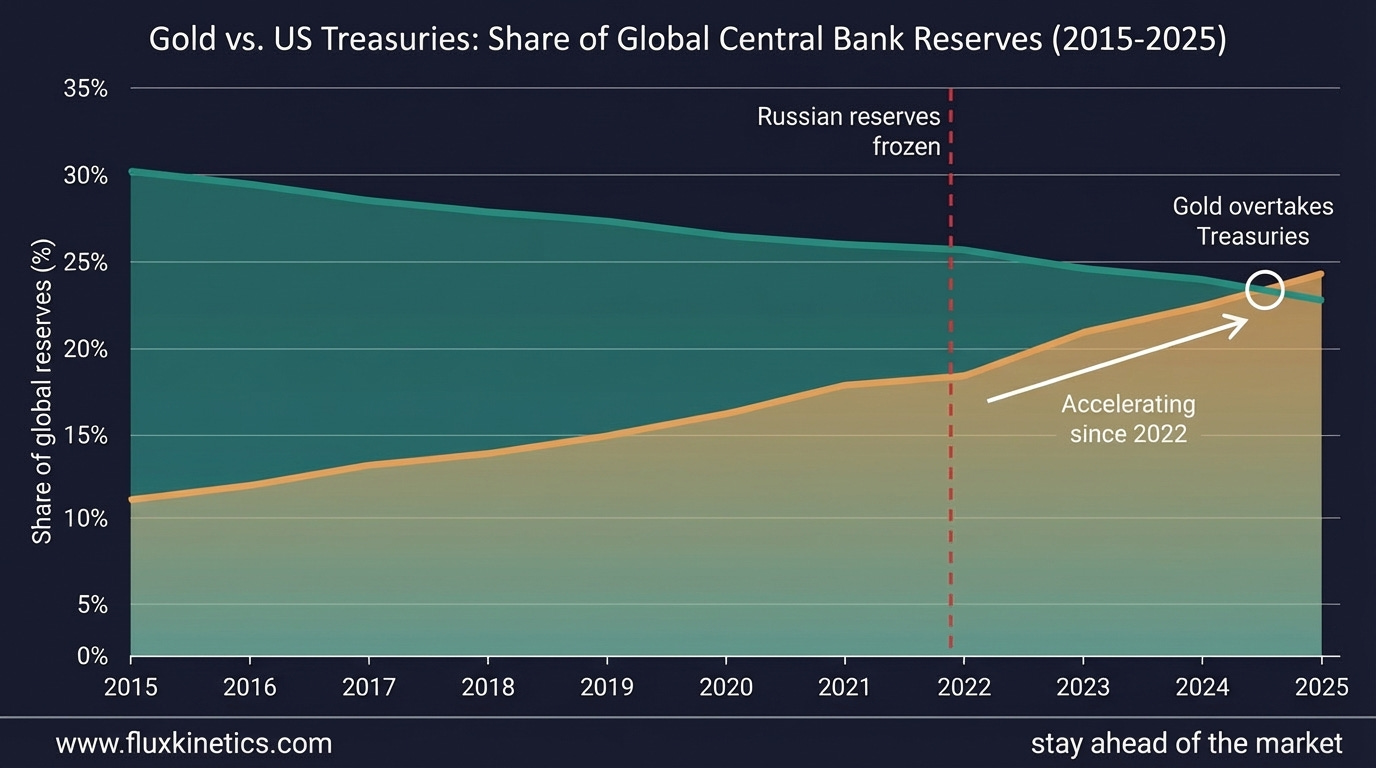

The Reserve Crossover

This vault drain has pushed the global monetary system across a historic threshold.

Gold officially overtook US Treasuries as the largest reserve asset held by foreign central banks in 2025. Gold’s share of global reserves climbed to roughly 18% in 2024 and continued higher through 2025, while the dollar’s share declined from above 30% in the mid-2010s to roughly 23%.

This is not a blip. It is a regime change in reserve composition. The foundation of global sovereign savings is shifting from sovereign paper to physical elements.

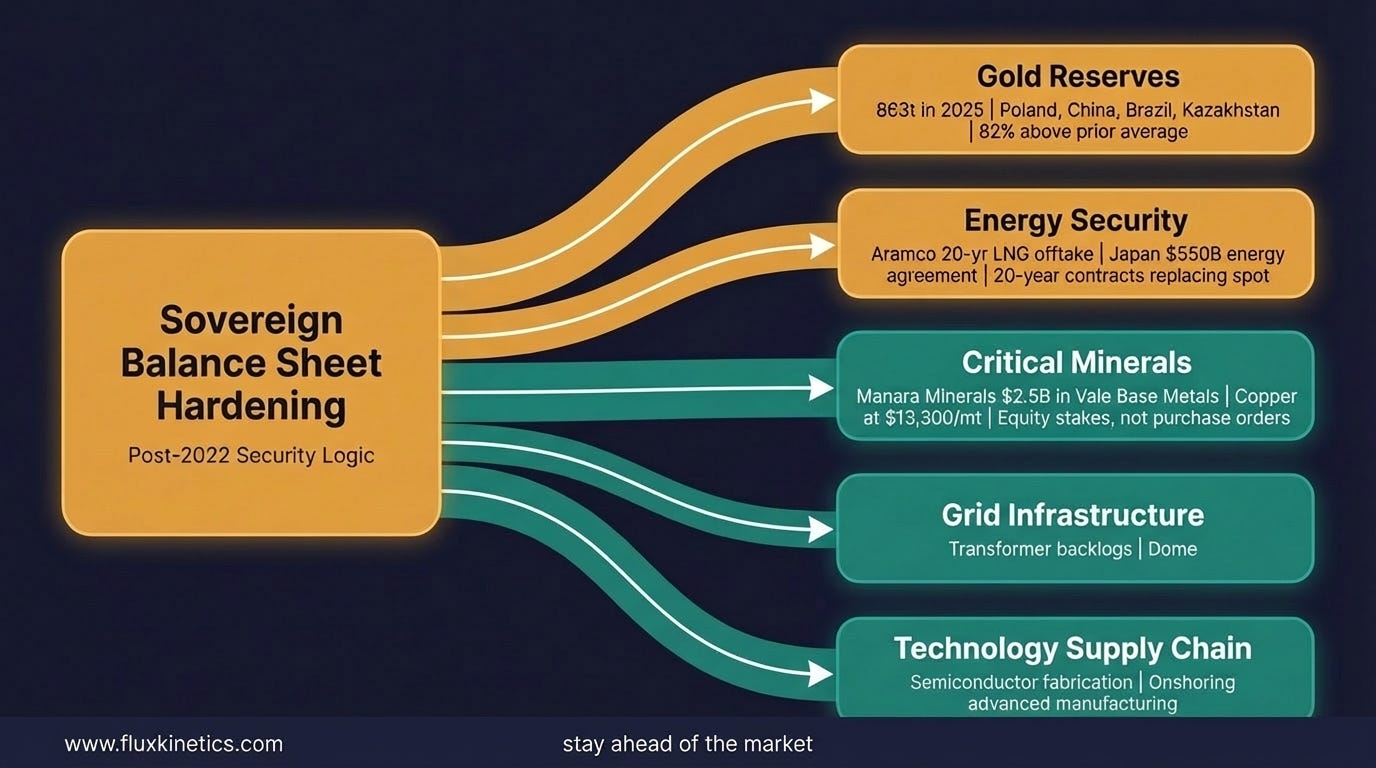

Chokepoints, Capital, and the Sovereign Hardening Thesis

This is where gold connects to the broader Flux Kinetics thesis. The gold vault drain is just the canary in the coal mine.

The same sovereign balance sheets accumulating bullion are hardening their positions across every physical commodity that matters. Saudi Arabia’s Manara Minerals closed a $2.5 billion acquisition of a 10% stake in Vale Base Metals, securing exposure to copper and nickel supply chains. Aramco Trading signed a 20-year LNG offtake agreement. Nations are locking down power transformer manufacturing capacity.

The scramble for unprintable assets is rapidly expanding from the central bank vault to the industrial supply chain, forcing a brutal repricing of physical chokepoints.

Watch how global superpowers escalated the war over physical supply chokepoints in 2025:

Gold. Copper. LNG. Uranium. Transformers. These are not separate stories. They are one strategy: harden the national balance sheet against a world where financial claims can be frozen, supply chains can be weaponised, and the assumption of open markets is no longer safe.

“Gold is not the trade. It is the balance sheet. The same logic shows up in copper equity, LNG off-takes, and transformer orders.”

The Exposure Matrix

If central bank buying sustains above 800 tonnes per year, and if even two or three major unreported buyers surface with revised holdings data, gold’s structural floor resets above $4,500 per ounce permanently, with corrections that rarely breach 10%.

Here is how you adapt:

Stress-test your custody assumptions. If you hold gold via unallocated accounts in London or Zurich, understand that the float backing those claims is shrinking. Calculate your ratio of allocated to unallocated holdings. If your gold cannot be delivered to you within 48 hours, you are holding a claim on a thinning pool.

Map your buyer-type exposure. Pull the breakdown of who holds gold in your portfolio’s reference market. If you are positioned for a correction that assumes ETF liquidation, ask whether the sovereign bid absorbs the dip before your entry triggers.

Connect gold exposure to your broader hard-asset thesis. If you are long copper, LNG, or grid infrastructure but short or flat gold, you are implicitly betting that the same sovereigns securing energy and metals supply will stop securing their reserves. That is an inconsistent position. Audit it.

One counterargument is worth naming. If central banks slow purchases or reverse, the sovereign floor disappears and gold reprices hard. That risk is real. But the $300 billion in frozen Russian reserves already happened. The rethink of custody is structural, not cyclical. The floor may wobble, but it is not going back to where it was.

The volatility structure itself has shifted. Gold is not a commodity trade anymore. It is the reserve side expression of a global sovereign hardening cycle. The vaults are draining. The question now is not whether you understand that. It is whether your portfolio does.

Coming next:

Silver is doing two jobs at once. The market hasn’t priced that tension yet.

Every grid in the world needs the same copper. Someone is going to run short.

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

Important distinction between the marginal ETF flows and the reserve accumulation, because if the buyer that can set the floor is a state, then volatility isn’t tied up as much to Fed prints anymore.

The shift from paper abstraction to physical control is a story about loss of trust. When systems stretch too far from underlying reality, they crack. Austrian Economics called it the “crack-up boom” - a late-stage rush into anything tangible as confidence in the financial layer erodes. What you’re describing is an admission: the old promises are no longer enough, so nations are reaching for what cannot be frozen, printed, or rehypothecated. Value is finding its way back to what can be held and sovereignly secured.