Oil at $100. Storage at Record Highs.

The number that breaks the rally narrative wide open.

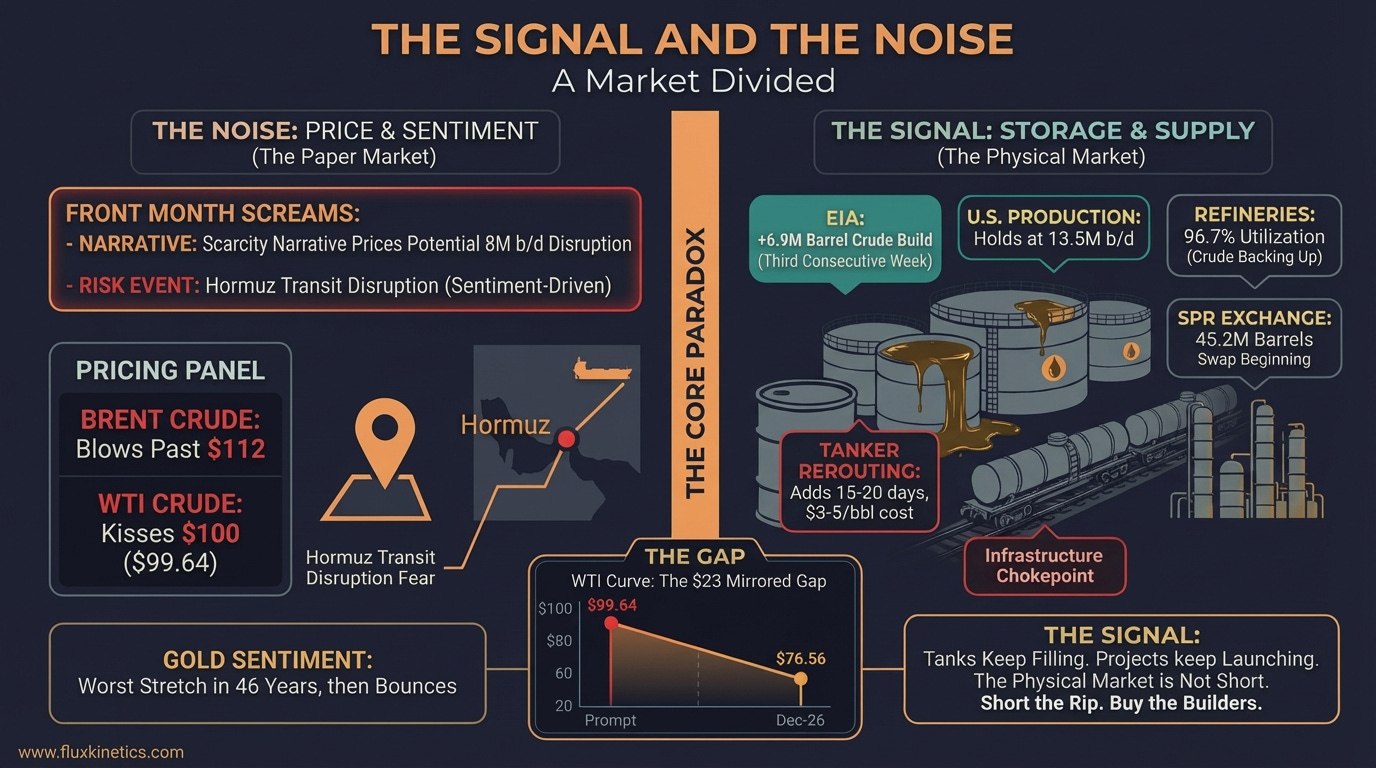

The May WTI contract closed Friday at $99.64, up 5.5% on the session alone, touching levels not seen since June 2022. Brent settled above $112 on the ICE. And yet, buried underneath the price fireworks, Wednesday’s EIA report showed U.S. commercial crude inventories climbed 6.9 million barrels to 456.2 million barrels. That is the third consecutive weekly build. Barrels are backing up into PADD 3 storage even as the Gulf Coast refinery complex runs at 96.7% capacity, the highest in months. The crude is arriving faster than it can be processed or exported. Meanwhile, Golden Pass LNG is pulling over 300 million cubic feet per day of feed gas as it nears its first cargo.

Here is what almost everyone missed this week. ConocoPhillips CEO publicly stated he expects the crude market to flip into contango, a forward curve structure where future month prices trade above the front month, signalling bearish fundamentals and ample supply expectations. That is the head of one of the largest U.S. producers telling you the front-month premium is a mirage built on headlines, not sustained physical tightness. When a producer with that much exposure starts talking about a bearish curve structure, it means the hedging desks are already positioned. The signal is not in the spot price. It is in the back of the strip. Dec-26 WTI settled at $76.56. That is a $23 discount to the front month. The back end of the curve does not believe this rally survives the summer.

This Week’s Settle

Oil: Brent (ICE May) settled Friday at $112.57, sharply higher on the week (+11.2%).

Gas: Henry Hub prompt-month settled near $3.03/MMBtu.

Gold: Spot gold closed Friday near $4,505/oz, higher on the session (+2.6%) but lower on the week (-3.5%).

Silver: Spot silver closed Friday near $70.50/oz, higher on the session (+2.8%) but softer on the week (-4.1%), as the gold-to-silver ratio compressed slightly to 64:1.

Lithium: China battery-grade lithium carbonate at 158,000 CNY/tonne (~$22,000/tonne USD), fractionally higher on the week (+0.96%).

Brief Contents

The Oil and Curve Story

The LNG and Infrastructure Story

The Metals and Critical Minerals Story

Projects, Policy, and Capital Flows

Week Ahead: What to Watch

Action Items

THE OIL AND CURVE STORY

WTI gained over 10% this week. Brent blew past $112. On Thursday alone, Brent settled up nearly 6% at $108.01. Friday added another 4.2%. The front of the curve is pricing a sustained supply removal from the Hormuz transit corridor, roughly 8 million barrels per day of normal throughput that has been disrupted for a month.

But the physical story underneath the headline is not a shortage story. Not in the United States.

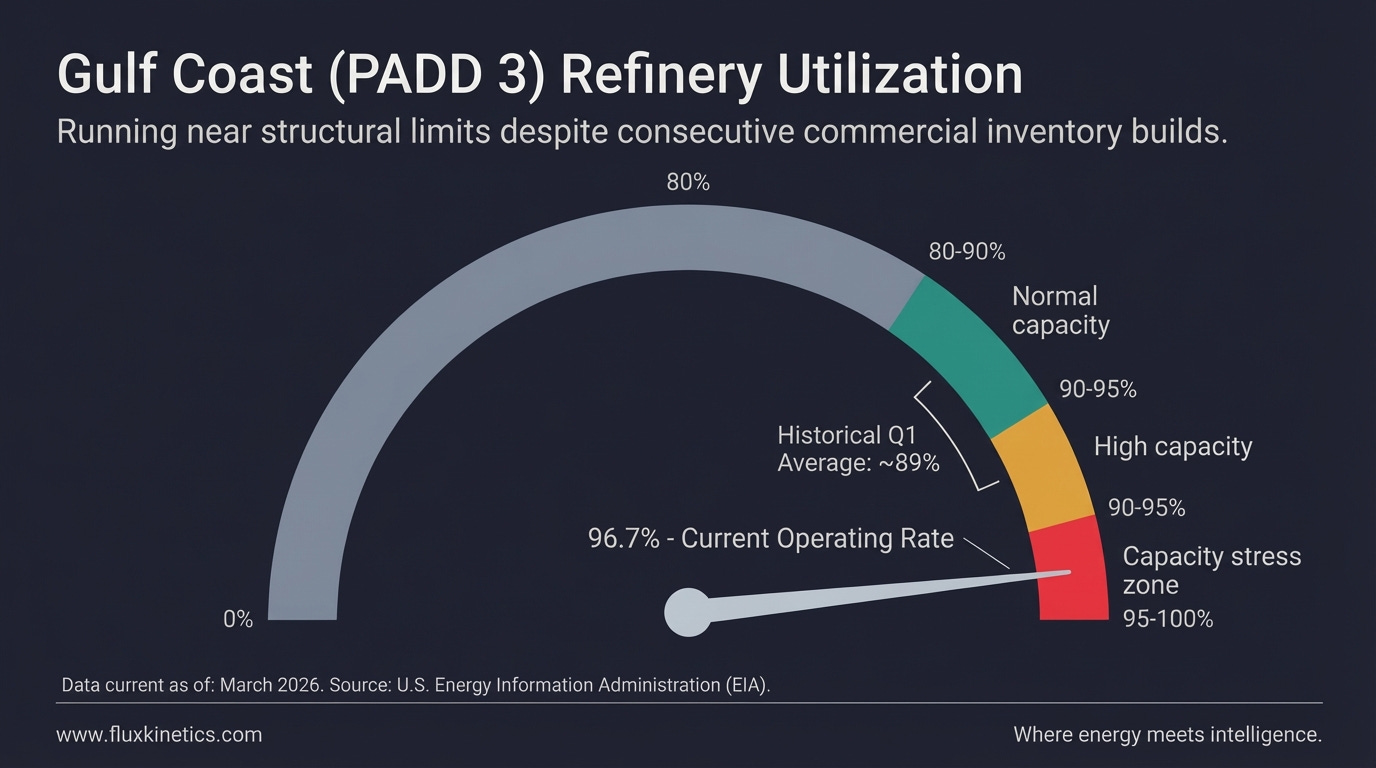

Wednesday’s EIA print showed commercial crude stocks at 456.2 million barrels, up 6.9 million barrels against a consensus expectation of just 0.5 million. Refinery inputs averaged 16.6 million barrels per day. That is near peak capacity. Crude is not sitting idle because refiners are shut. It is sitting in tanks because the domestic supply machine is producing faster than the export and processing infrastructure can clear it. PADD 3 usage hit 96.7%. Cushing stocks are climbing. The America First Refining project at the Port of Brownsville, the first new U.S. oil refinery in 50 years, just had its groundbreaking confirmed for April 2026. That 168,000 b/d facility backed by Reliance will process light shale crude. But it will not contribute a single barrel of throughput for years.

The back of the curve knows this. Dec-26 WTI settled at $76.56. Jan-27 WTI settled at $75.42. The 6-month time spread between front and back is now over $23, the steepest in years. “Backwardation” is the structure where the nearest delivery month trades at a premium to future months, typically reflecting perceived near-term tightness. But when inventories are building while the curve stays in steep backwardation, the tightness is in sentiment, not in barrels. That is the definition of a paper-driven premium.

“When the front month screams and the back month whispers, listen to the whisper.”

The Flux Kinetics Number: 6.9 million barrel. That is this week’s EIA crude build. The third consecutive weekly build in the middle of what the headline calls the worst supply disruption in the history of the oil market.

THE LNG AND INFRASTRUCTURE STORY

This was the biggest week for U.S. LNG project momentum in years. 3 distinct developments landed in the same 5-day window, and together they redraw the map of North American gas liquefaction capacity for the next decade.

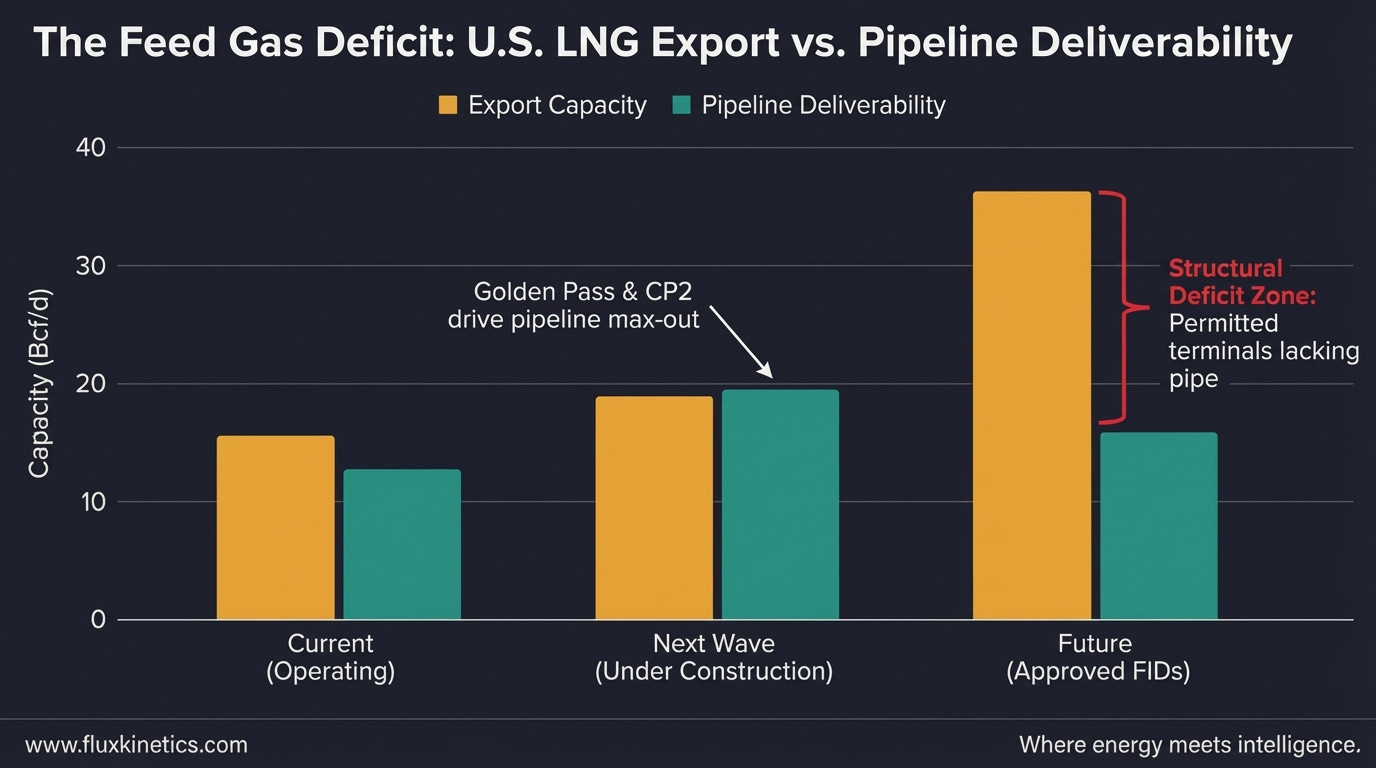

First: Golden Pass LNG. The $10-billion, 18.1 million tonne per annum (mtpa) export terminal in Sabine Pass, Texas, is now pulling over 300 million cubic feet per day of feed gas as it advances commissioning on Train 1. Exxon CEO Darren Woods said in January he expected first LNG in “very early March.” That deadline slipped, but infrared monitoring and LSEG data show liquefaction is imminent. RBN Energy confirmed this week that Golden Pass is expected to produce its first cargo by late March. When Train 1 comes online, it adds roughly 2.17 Bcf/d of incremental LNG feed gas demand to the Lower 48 by year-end. That is not a forecast. It is pipe that is already connected, pulling gas, and cooling down.

Second: Venture Global secured an $8.6 billion project financing and took FID on Phase 2 of its CP2 LNG project in Cameron Parish, Louisiana. That brings total CP2 financing to $20.7 billion and positions Venture Global to become the largest LNG producer in the United States, with a combined peak capacity of 29 mtpa across its facilities. The DOE also authorised Plaquemines LNG to export 3.85 Bcf/d, a 13% increase over its prior green light. Nearly 70% of 2026 Plaquemines cargoes are already contracted.

Third: TC Energy signed commercial agreements with LNG Canada this week to advance Phase 2 of the Coastal GasLink (CGL) pipeline expansion. The deal would double CGL’s throughput capacity, feeding an expanded LNG Canada terminal in Kitimat, British Columbia. Canadian Prime Minister Carney has fast-tracked it as a “project of national significance.” This is the most important Western Canadian gas infrastructure deal in a decade.

In addition, sitting in the background: Delfin Midstream confirmed at CERAWeek that its 13.2 mtpa floating LNG (FLNG) project offshore Louisiana is ready for FID as soon as its feed gas pipeline receives regulatory approval. Shell CEO Wael Sawan hinted at potential FIDs on Venezuelan offshore gas projects that would pipe through Trinidad for LNG export. ExxonMobil expects FID on the $20-24 billion Rovuma LNG project in Mozambique in the second half of 2026.

The driver most coverage missed this week is the bottleneck between these FIDs and physical molecules. Business leaders at CERAWeek in Houston warned publicly that the United States lacks the pipeline infrastructure to fill the gap between approved liquefaction capacity and actual feed gas delivery. Eight terminals are operating. Eight more are under construction. Nine have been approved but feed gas pipeline capacity into the Gulf Coast LNG corridor is near its limit. You cannot liquify molecules you cannot deliver to the terminal.

“The cargo that doesn’t exist cannot replace the one under construction.”

The Insider View: LNG stocks priced in the North American export boom two years early. The physical market is only now learning that pipeline capacity to terminals, not permits, is the real chokepoint. Midstream operators with Gulf Coast pipeline exposure win here. Pure LNG developer stocks have already had their run.

THE METALS AND CRITICAL MINERALS STORY

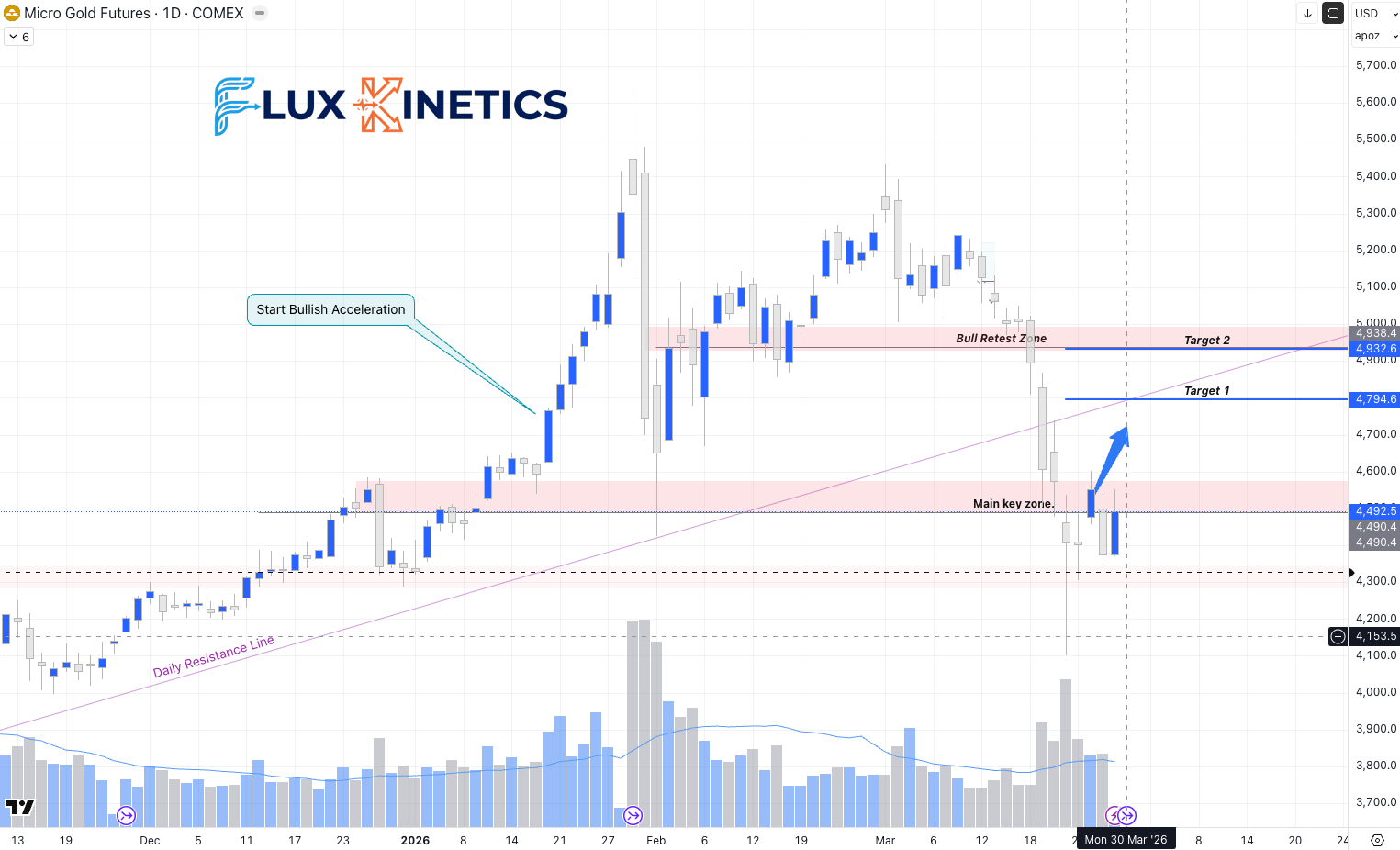

Gold had its worst stretch in 46 years, and then it bounced.

Friday’s close near $4,505 came after a multi-week selloff that took gold more than 20% below its January all-time high above $5,500. The proximate catalyst for Thursday’s final flush was Turkey’s central bank, which sold and swapped approximately 60 tonnes of gold, over $8 billion in value, in the two weeks since early March. Reserves fell 6 tonnes in the week of March 13 and another 52.4 tonnes in the week of March 20. Most was used in swap transactions to secure foreign currency liquidity. When a top-ten central bank buyer becomes a forced seller, the floor drops.

Friday reversed the flush. Dip-buying came in hard after support held near $4,342. Gold surged 2.6% on the day. Silver outperformed at +2.8%, closing near $70.50. The gold-to-silver ratio compressed to 64:1, which remains elevated relative to the sub-45 reading from January but off the March high near 66.

Copper surged to fresh records at CERAWeek, with S&P Global presenting data showing the supply crunch is structural. At $5.49 per pound, copper is pricing the physical deficit. A Reuters poll of 31 analysts placed the median 2026 copper price forecast at $11,975 per tonne. Unlike gold, the copper story is not about hedging or safe haven flows. It is about transformers, busbars, and cable trays that physically cannot be manufactured fast enough to wire up the data center and grid storage buildout.

My Flux Kinetics Trade: The main Key Zone has broken down sharply reaching a 4100$ level, with an immediate rejection, following by a test of the same zone with a second rejection. Opening of the session will be crucial with short term trading advised knowing the current volatility:

Close above the Main Key Zone (4550$), long trade toward 4700$.

Close below Main Key Zone (4480$), short trade toward 4372$.

“Turkey sold 60 tonnes. The floor held. That tells you who was buying.”

PROJECTS, POLICY, AND CAPITAL FLOWS

The project cycle accelerated this week across every segment of the energy value chain. This is what a capital reallocation wave looks like when it arrives all at once.

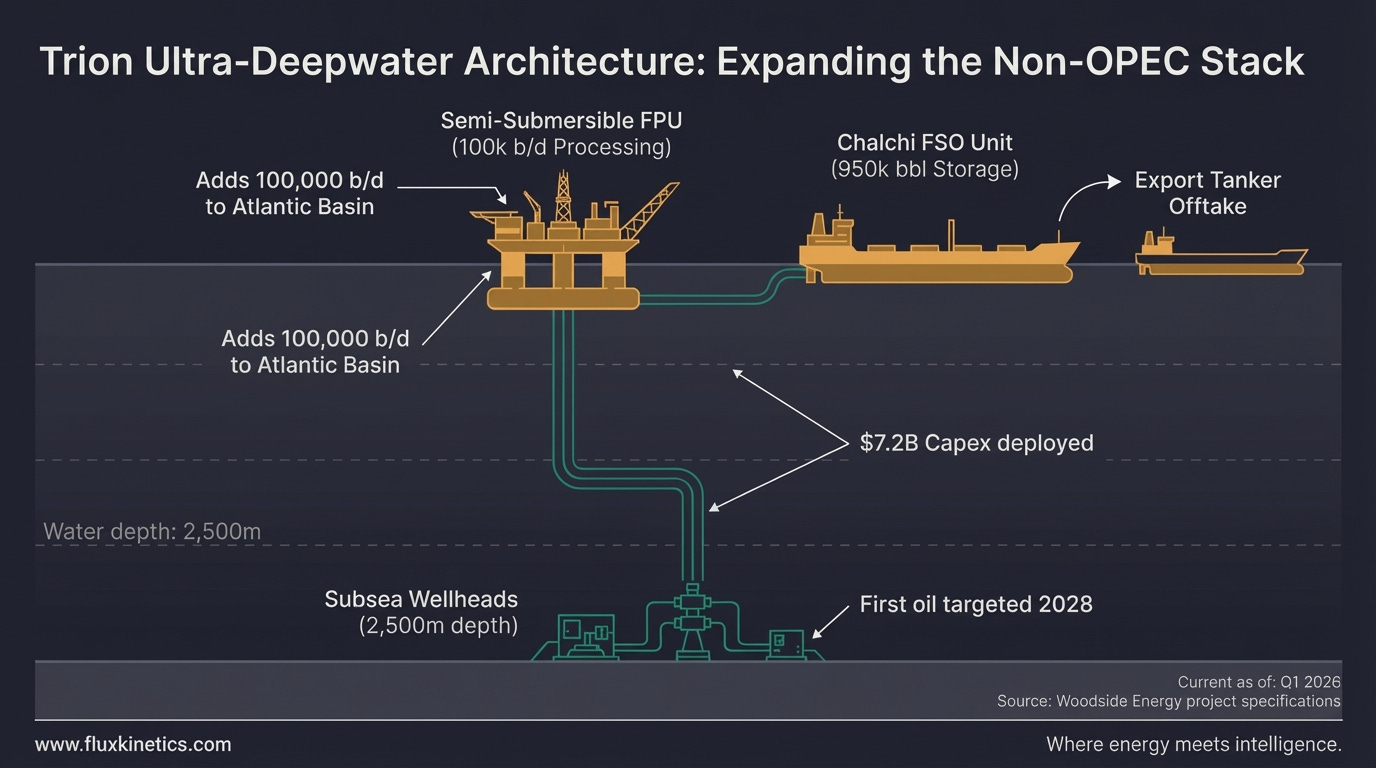

On the upstream side, Woodside Energy and PEMEX launched the drilling campaign at the Trion field in the Gulf of Mexico, Mexico’s first ultra-deepwater oil development. The $7.2 billion project is 50% complete. The Deepwater Thalassa drillship arrived in Mexican waters in early March. At peak production, targeted for 2028, Trion will contribute 100,000 b/d, roughly 6-7% of Mexico’s current daily output. Production will load into the Chalchi floating storage and offloading (FSO) unit, which holds 950,000 barrels. That is 100,000 b/d of non-OPEC, non-U.S., deepwater crude entering the Atlantic Basin supply stack before the end of the decade.

The Brownsville refinery announcement, backed by India’s Reliance, is a $3 billion construction project that will process 168,000 b/d of U.S. light shale crude. Groundbreaking is set for April 2026. This will be the first new U.S. oil refinery in nearly 50 years. It does not change the near-term supply picture, but it changes the structural capacity trajectory for U.S. downstream processing and export competitiveness through the end of the decade.

The Flux Kinetics Policy Pulse: Energy CAPEX are still moving forward. New projects development start to be released based on new prices. The best time to secure an increased ROI is now.

Week Ahead: What to Watch

April 1: March Nonfarm Payrolls. OPEC+ April Production Adjustments Begin.

April 2: EIA Weekly Petroleum Status Report.

Projects: Golden Pass First Cargo Window. Delfin FLNG Pipeline Approval.

“The FID wave is here. The pipe to feed it is not.”

Flux Kinetics Action Items

For Traders: Short term trades are the best ones now. Close above 101$ with a retest activate a long trade toward 118$

For Operators: Woodside’s Trion drilling campaign means new FSO logistics and vessel scheduling in the Gulf of Mexico. If you supply deepwater support services, the order book just expanded.

For Investors: Buy the builders. The infrastructure owners and midstream operators with exposure to U.S. LNG feed gas pipelines and Western Canadian pipeline expansion are the structural winners of this cycle.

If this changed how you see the week, send it to one person who needs to see it too.

In case you have missed my previous article about the Pump Price rise and decline :

Coming next:

Silver’s Split Personality: Monetary Metal Meets Industrial Chokepoint.

Copper at the Wall: When Every Grid Needs the Same Ton.

Share this with the person who always asks what actually moved this week and why. That is who Flux Kinetics is written for.

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.