5.5 Million Barrels Built. The Curve Didn’t Care.

The tanks filled while the IEA warned of April tightness.

The EIA dropped the number on Wednesday. Crude inventories rose 5.5 million barrels to 461.6 million for the week ending March 27. That is near a three-year high. Yet Brent settled the week above $110 as the IEA warned supply balances tighten further in April. Barrels kept flowing into tanks at the same time the front of the curve kept pricing scarcity.

Here is what almost everyone missed this week. The 5.5 million barrel build is a domestic phenomenon. PADD 3 Gulf Coast storage absorbed the bulk : the same region that took a 6.2 million barrel build the prior week. Refinery inputs averaged 16.4 million barrels per day at 92.9% usege, 220,000 bpd lower than the previous week. The crude is not sitting because refiners are shut. It is sitting in tanks because the export and processing infrastructure cannot clear it fast enough. Barrels are trapped in the wrong geography. The physical market overseas is starving.

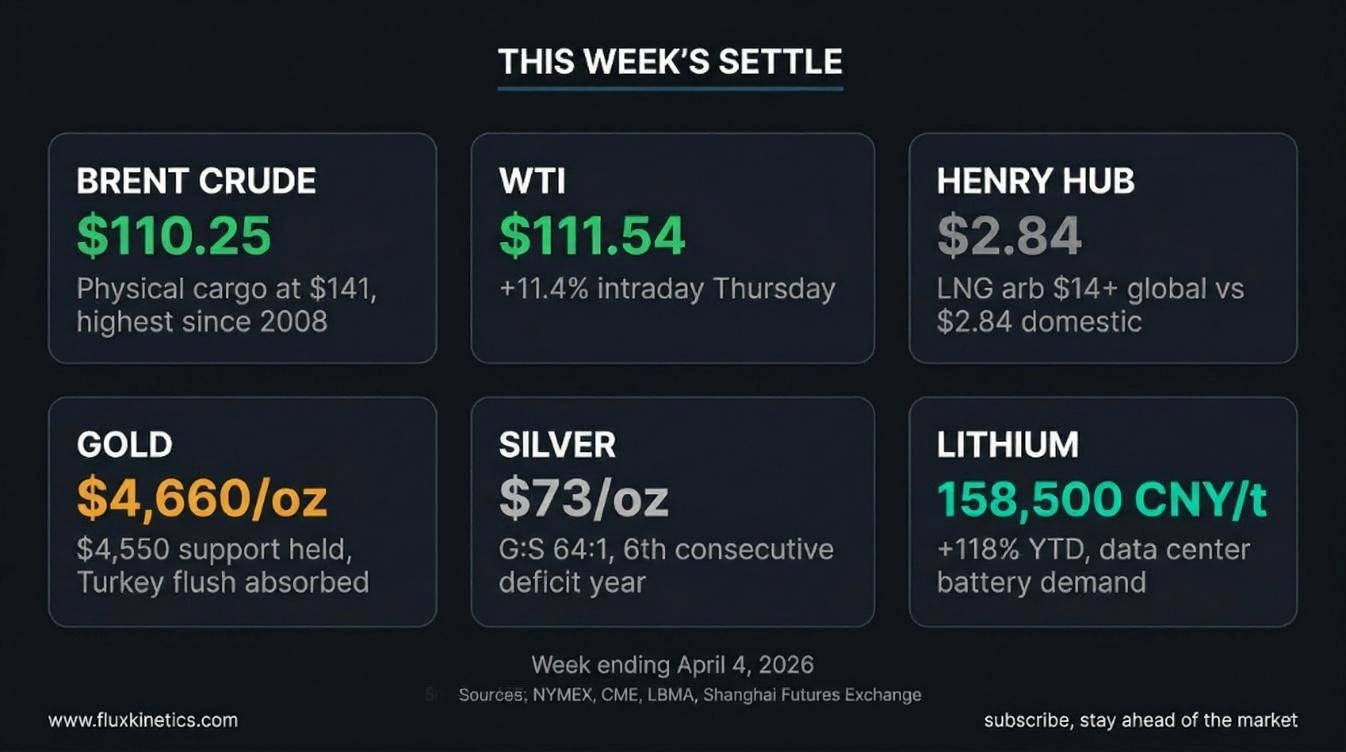

This Week’s Settle

Oil: Brent (ICE June) settled Friday at $109. WTI (NYMEX May) settled at $111.54 after an 11.4% intraday surge on Thursday. Physical dated Brent hit $141.36, the highest since 2008.

Gas: Henry Hub prompt-month near $2.84/MMBtu.

Gold: Spot gold closed near $4,660/oz, holding above the $4,550 main key zone.

Silver: Spot silver near $73/oz. Gold-to-silver ratio compressed to 64:1.

Lithium: China battery-grade lithium carbonate at 158,500 CNY/tonne ($22,000/tonne USD), up 118% year-to-date.

Brief Contents

The Physical vs. Paper Divergence

LNG and Infrastructure

Metals and Critical Minerals

Week Ahead: What to Watch

Flux Kinetics Action Items

The Physical vs. Paper Divergence

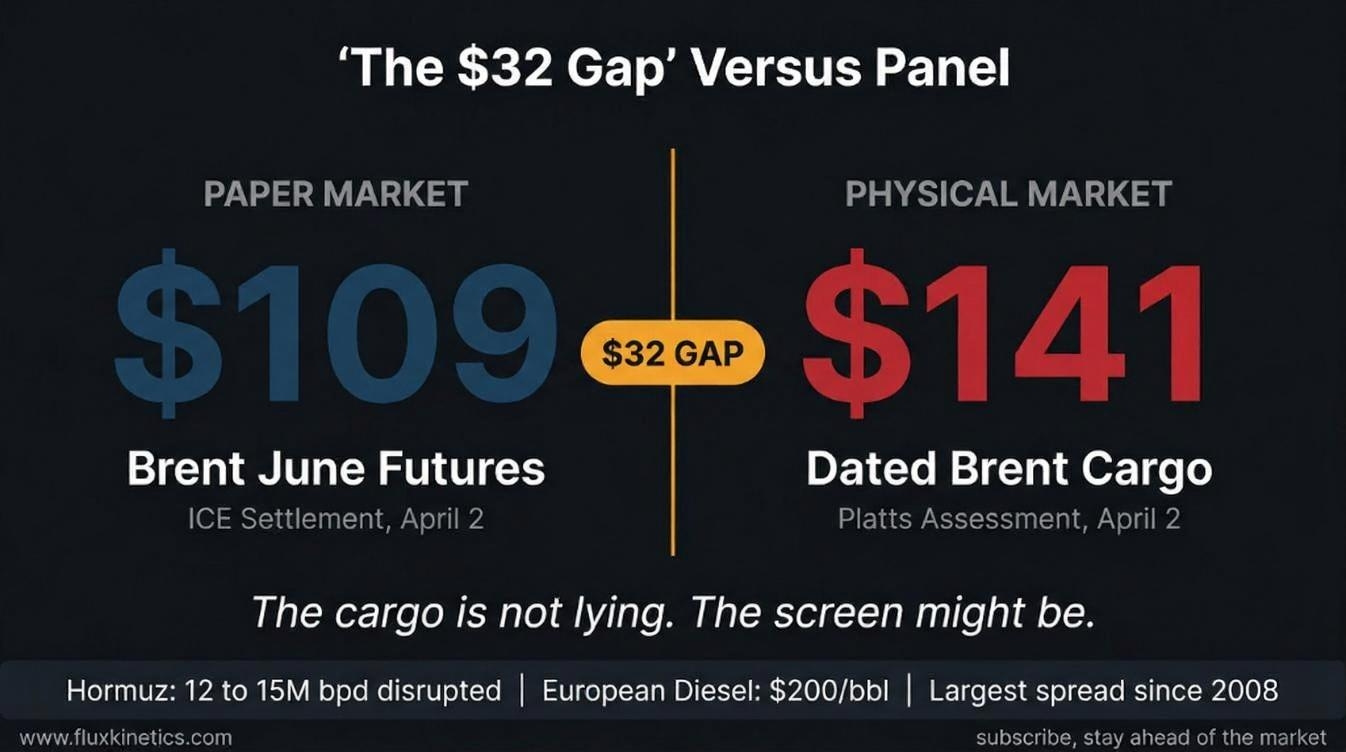

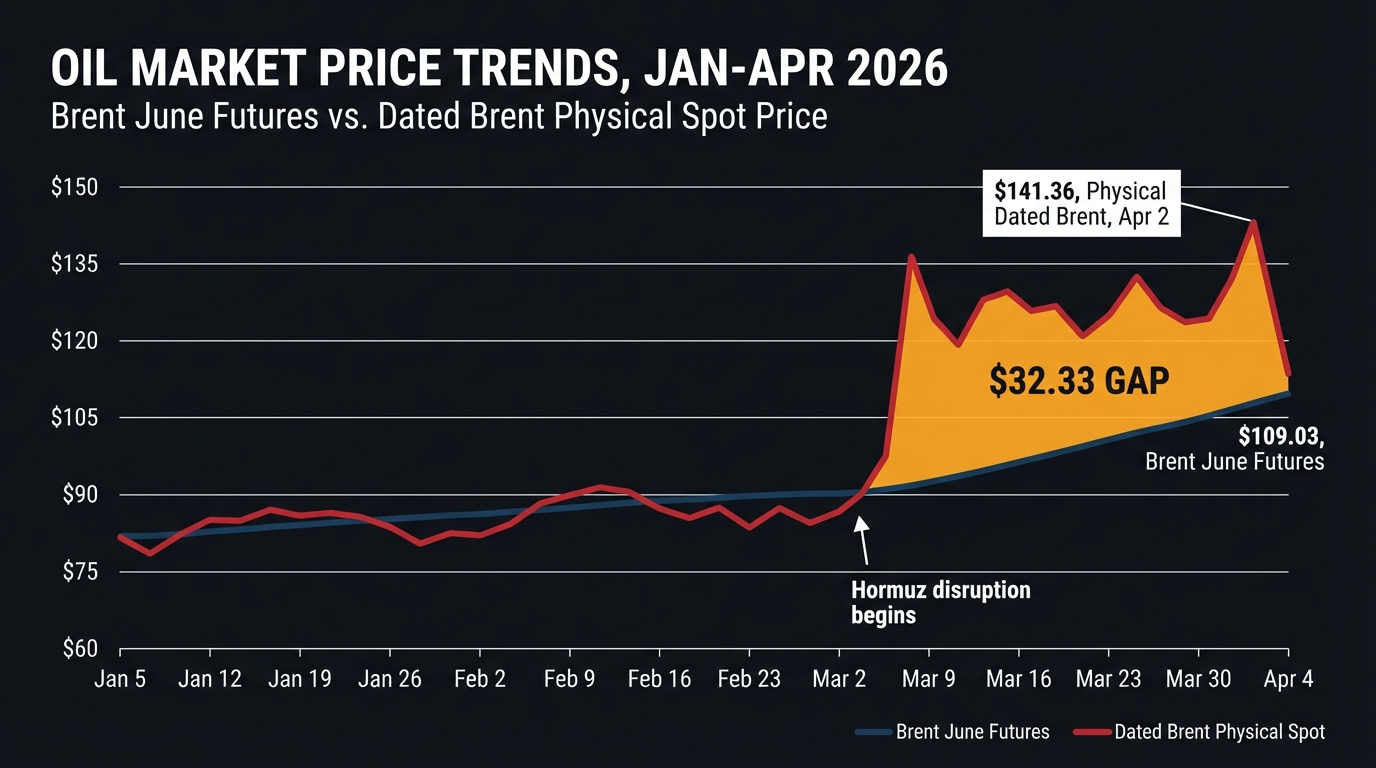

This is the story the headline misses. On April 2, physical dated Brent, the price for an actual cargo of crude loading in the North Sea, surged to $141.36. The June Brent futures contract settled that same day at $109.03

That is a $32.33 gap. The largest physical-over-paper premium since 2008.

Chevron CEO Mike Wirth warned that futures are based on “scant information” and do not reflect the actual disruption. European diesel futures breached $200 per barrel for the first time since 2022. These are not forecasts. These are settlement prices.

The driver is the Strait of Hormuz. Roughly 12 to 15 million barrels per day of Middle Eastern supply, about 15% of global production, is disrupted. Iraq’s Basra exports are running at a fraction of normal. The physical market is scrambling for molecules. The paper market is looking at Cushing inventories and calling it oversupply.

When the front month screams $109 and a cargo in the North Sea trades at $141, one of them is lying. The cargo is not lying.

The backwardation is the steepest in years. The 6-month time spread between front and back is running over $20. Dec-26 WTI settled near $80. Jan-27 WTI near $75. The back end of the curve does not believe this disruption survives the summer.

But there is a quality problem the curve cannot show you. The Strait of Hormuz moves medium-sour crude. The barrels building in PADD 3 are light-sweet. Refiners in Europe and Asia configured for sour feedstock cannot simply swap in Permian crude. The barrels are not interchangeable. You can look at a headline inventory number and call it surplus. But if the barrel in the tank is the wrong grade for the refiner that needs it, it might as well not exist.

The Flux Kinetics Number: $32.33. That is the physical-paper spread on dated Brent. The largest since the 2008 financial crisis. Until this gap closes, the headline futures price is not telling you the truth about the physical market.

The Supply Response That Exists on Paper

OPEC+ met Sunday, April 5, and agreed to raise May output quotas by 206,000 barrels per day. The market shrugged. Rightly so. Saudi Arabia, UAE, Kuwait, and Iraq cannot physically increase exports because the transit corridor is closed. The IEA launched a record 400-million-barrel emergency reserve release in March. The DOE initiated a 172-million-barrel SPR exchange on April 6. These are real barrels, but they take weeks to reach refiners

You cannot export molecules through a closed strait. The OPEC+ hike is a press release, not a cargo.

LNG: Hormuz’s Second Casualty

The Strait of Hormuz is not just an oil chokepoint. It is the transit corridor for a massive share of global LNG volumes. The disruption has blown a hole in global gas supply chains that U.S. infrastructure is racing to partially fill. The DOE authoriSed a 22% increase in LNG exports from the Elba Island terminal this week, Kinder Morgan’s facility in Georgia. U.S. LNG feed-gas flows remain steady. Golden Pass LNG continues commissioning near Sabine Pass, but a single terminal authorisation cannot patch a structural supply gap of this scale.

Henry Hub at $2.84 with global LNG spot above $14/MMBtu tells you the arbitrage is wide open. The constraint is not the molecule. It is the pipe to the terminal.

Metals and Critical Minerals

Gold held the $4,550 main key zone this week. After the Turkey central bank liquidation event (60 tonnes sold in two weeks), dip-buying absorbed the flush. The $4,342 floor held. Friday’s close near $4,660 confirmed the support.

Silver at $73 is doing two jobs. Monetary hedge and industrial metal. The gold-to-silver ratio at 64:1 is compressing from its March high near 66. Silver’s industrial demand story (solar panels, EV busbars, data center electrical components) is structural.

Copper at $5.64/lb. S&P Global presented data at CERAWeek showing the deficit is structural. Transformer lead times are running 30+ months. Every grid upgrade, every data center, every EV charging station needs copper and cannot get enough of it.

Lithium carbonate at 158,500 CNY/tonne is up 118% year-to-date. The EV narrative stalled, but data center battery backup demand (LFP cells, lithium-heavy, cobalt-free) is the new demand driver. At $22,000/tonne, the market is pricing in the storage spring.

My Flux Kinetics Trade: If you took the long trade from last week article, congratulations, you’ve reached Target 1 !

29th March 2026 : “Close above the Main Key Zone (4550$), long trade toward 4700$.”

I will be extra cautious this week as the geopolitical decisions will create wide volatility. Watch the Main Key Zone for a rebound with a tight stop. Focus on protecting your capital this week as top priority, no set up.

Week Ahead: What to Watch

April 7-8: Iran-related headline risk. Any Hormuz reopening signal collapses the physical premium overnight. Any escalation sends physical cargoes toward $150.

April 9: EIA Weekly Petroleum Status Report.

April 10: IEA Oil Market Report for April.

Projects: Golden Pass LNG first cargo window remains open. Delfin FLNG pipeline approval pending.

The screen says $109. The cargo says $141. The spread between those two numbers is where the truth lives this week.

Flux Kinetics Action Items

For Traders: This week, you need to be cautious. Trade the range. Do not anchor to a direction while a war sets the bid. Focus on saving your capital and hedge accordingly.

For Operators: Secure medium-sour feedstock now. If you run a refinery configured for Gulf crude grades, every week of Hormuz closure tightens your supply further. Light-sweet substitution has limits. The quality mismatch is real and worsening.

For Investors: Buy the builders. Midstream operators with Gulf Coast LNG pipeline exposure and Western Canadian pipeline expansion are the structural winners. Avoid surplus-cycle commodity ETFs that track paper prices while the physical market diverges.

If this changed how you see the week, send it to one person who needs to see it too.

In case you have missed my previous article about the Pump Price rise and decline :

Coming next:

The Global Food Chokepoint: Why a Hormuz Blockage is also Caloric Crisis.

Silver’s Two Masters: The Metal That Can’t Serve Both

Share this with the person who always asks what actually moved this week and why. That is who Flux Kinetics is written for.

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

You speak to our faith in systems we barely understand. We’ve come to believe that because something exists, it is available. But reality doesn’t that way. There is distance between having and accessing. Between what sits and what flows. We’ve optimized for efficiency, for just-in-time everything … until the smallest disruption reveals how little slack we’ve allowed for. And when that slack disappears, what we called abundance shows itself as dependence.