What the UAE’s OPEC Exit Really Means

Everything you need to know

A plain-English guide to the cartel, the math, and why Abu Dhabi walked

Dear Executives, Traders & Investors, Brilliant minds and Friends

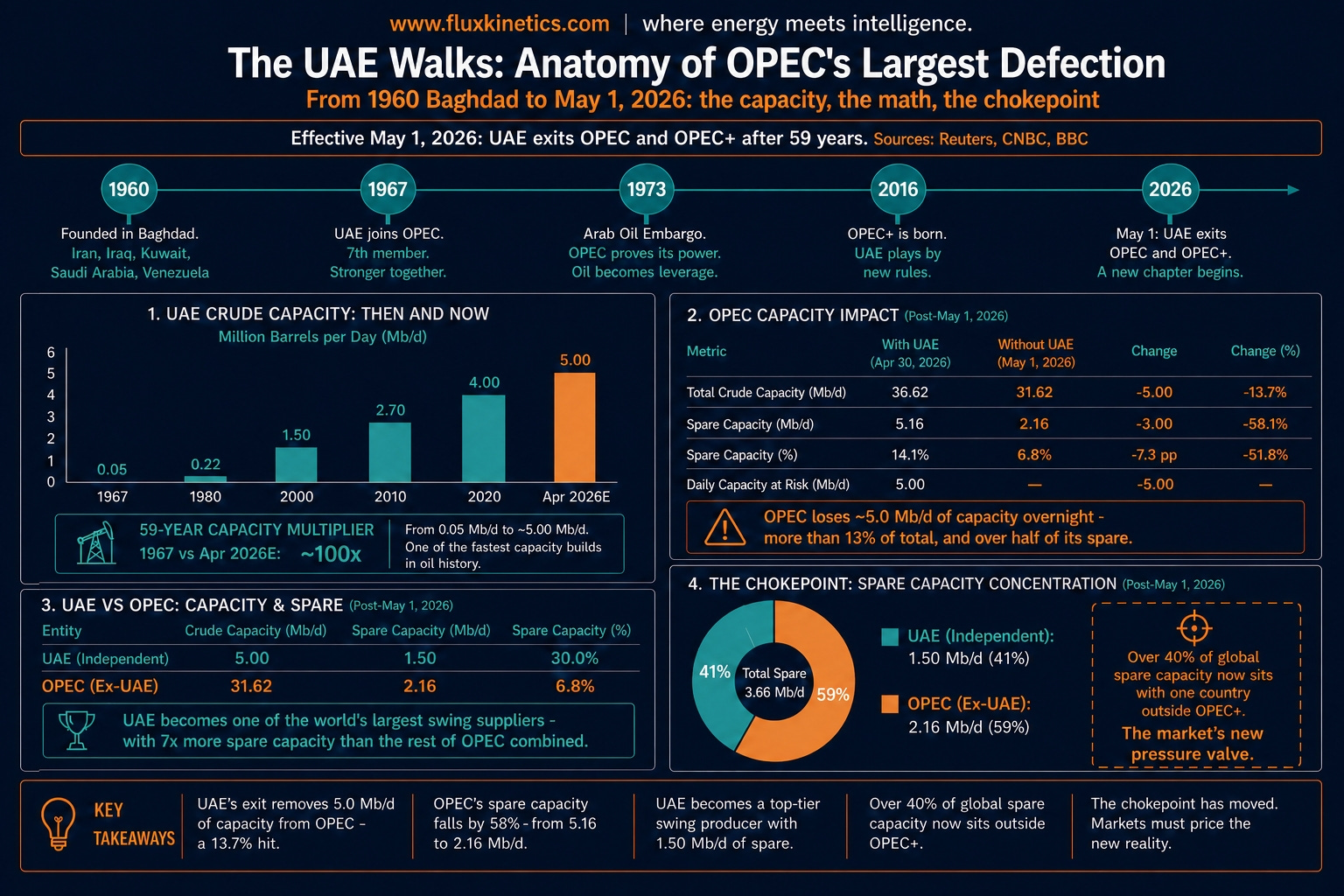

On April 28, 2026, the UAE said it would leave OPEC and OPEC+, effective May 1. UAE Energy Minister Suhail Al Mazrouei told Reuters the decision followed a review of the country’s production policy and future energy strategy. He also said the move had not been discussed with any other country.

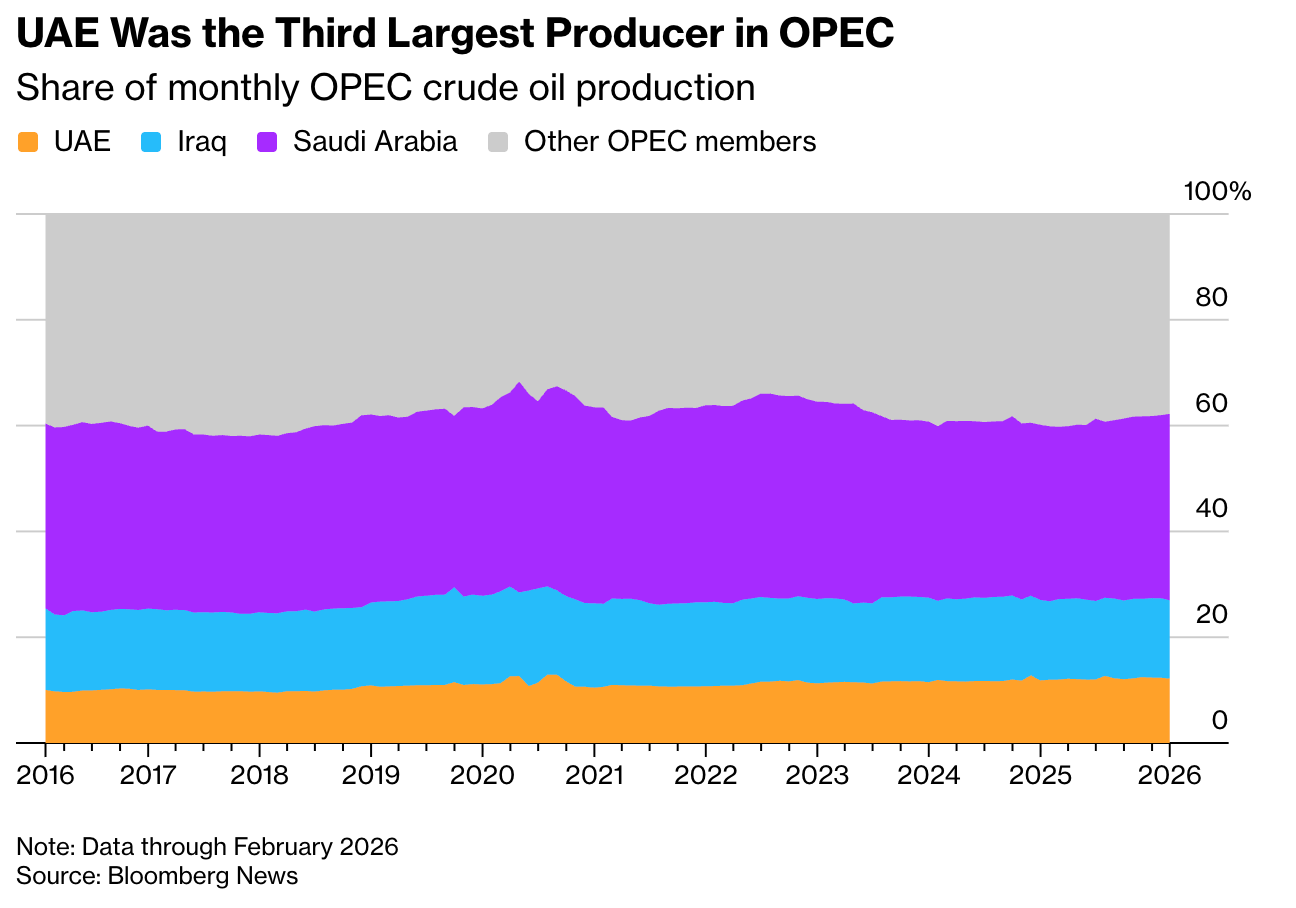

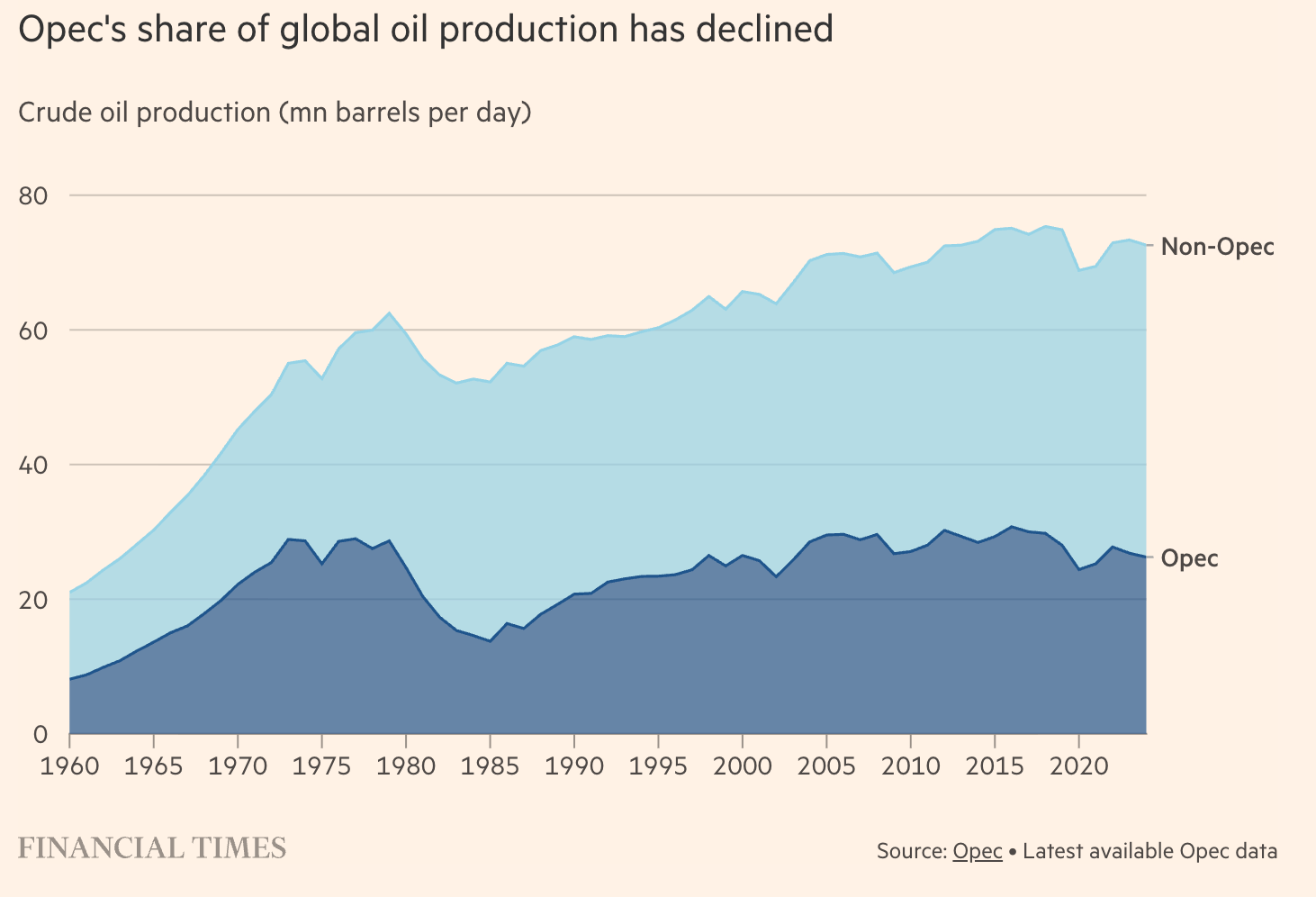

One of OPEC’s largest producers, third or fourth depending on the month and methodology, is leaving after nearly six decades inside the tent.

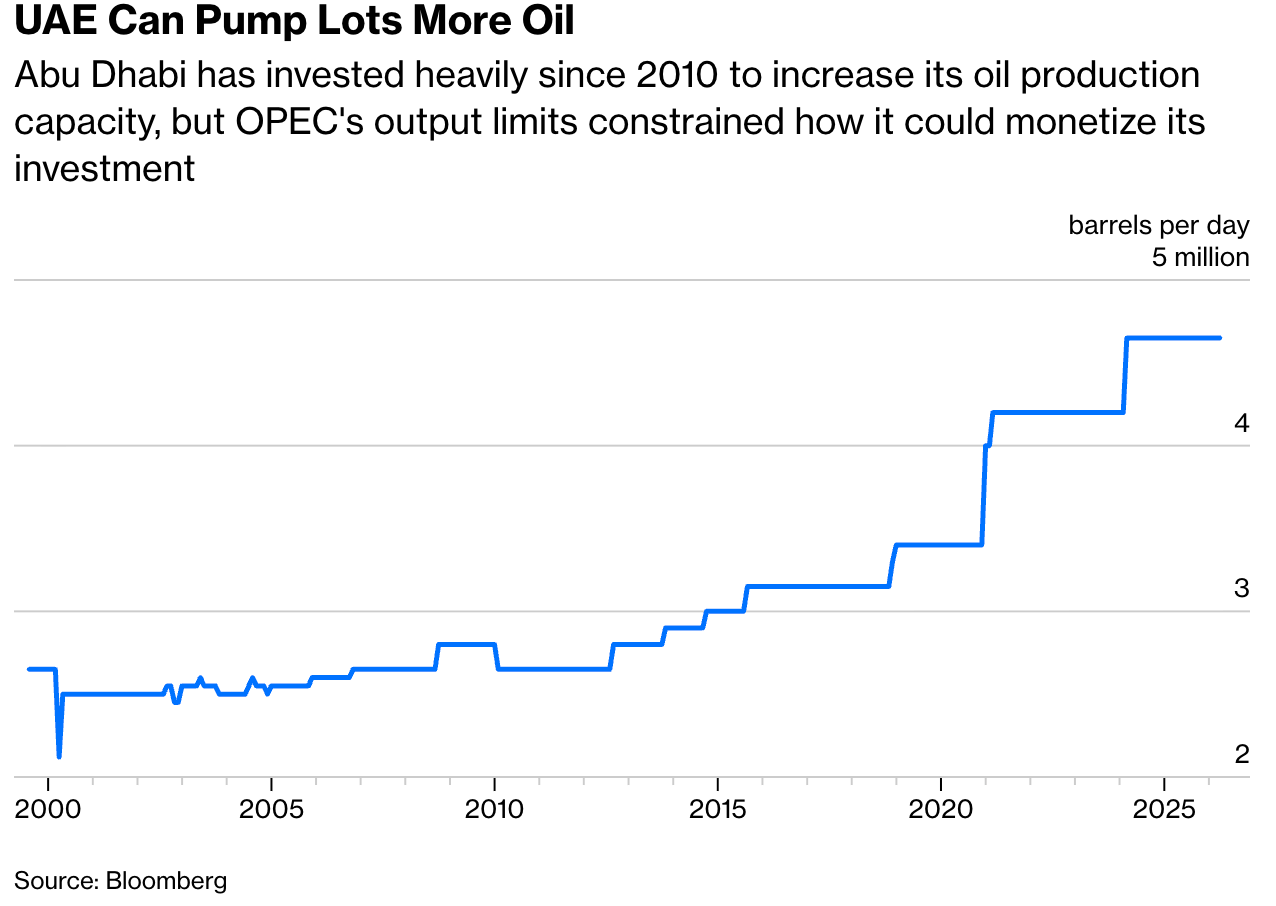

The headlines called it a shock…It was not. The capacity-quota gap inside the UAE has been widening for five years. ADNOC has been building capacity toward 5 million barrels a day while the UAE remained constrained by an effective OPEC+ limit in the roughly 3.2 to 3.5 million barrel a day range, depending on whether voluntary adjustments are included.

That leaves a capacity-quota gap of roughly 0.8 to 1.3 million barrels a day, barrels Abu Dhabi has invested to produce but could not fully monetise without breaching OPEC+ discipline. At today’s prices, that is real money walking out the door every quarter.

I explain in this deep dive, from the ground up, what OPEC actually is, why the UAE walked, and what changes for the world’s oil market over the next 12 to 24 months.

If you have never read a cartel primer, start at the top. If you trade this market, skip to the second half.

What This Article Covers

A short history of OPEC, in plain English

How the cartel actually works

Why the UAE walked

The capacity quota math

What changes from May 1

A short history of OPEC, in plain English

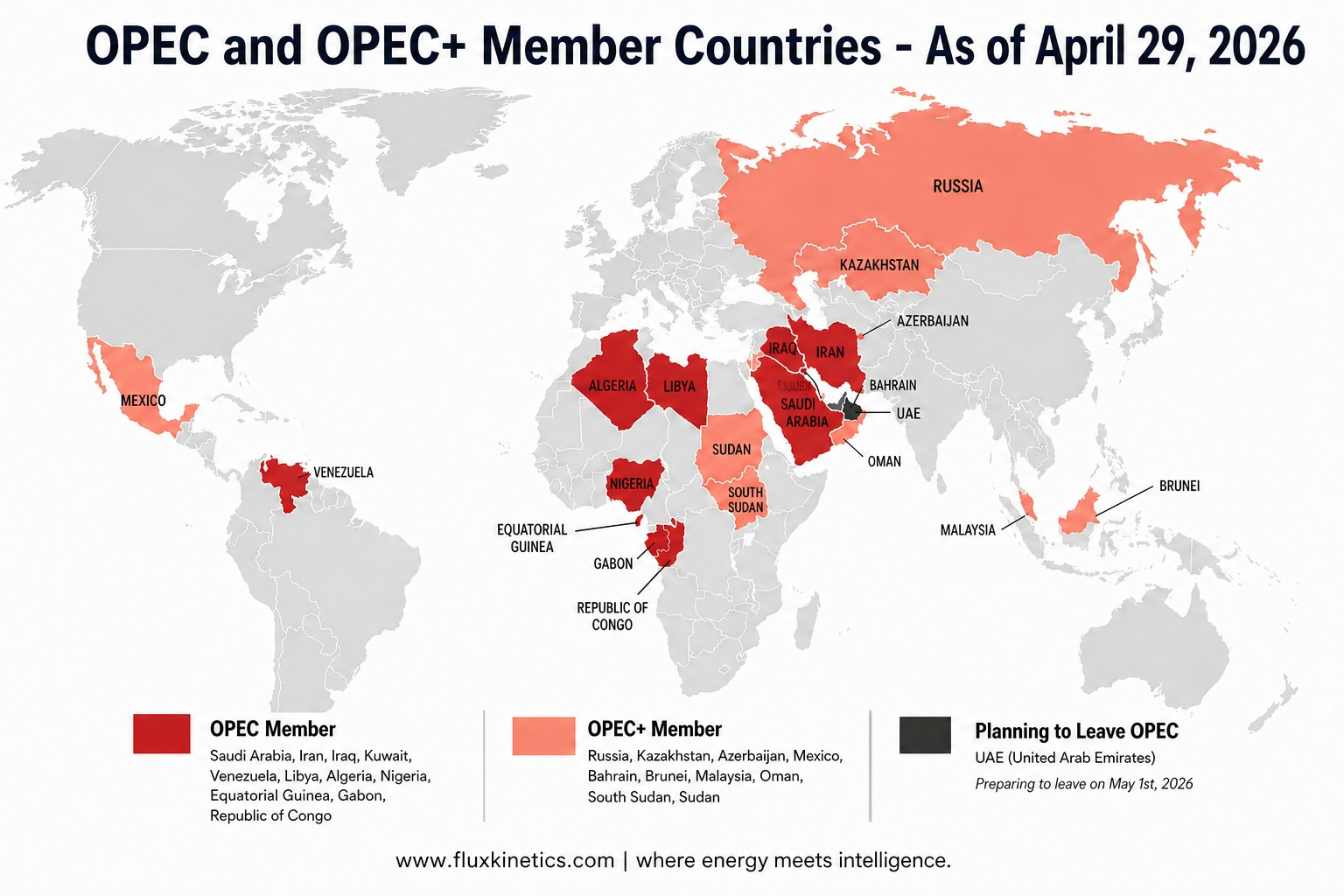

OPEC stands for the Organization of the Petroleum Exporting Countries. It was created at the Baghdad Conference from September 10 to 14, 1960. Five countries signed the founding agreement: Iran, Iraq, Kuwait, Saudi Arabia and Venezuela. The headquarters has been in Vienna since 1965.

The reason for founding was straightforward. In the late 1950s, large Western oil companies, the so-called Seven Sisters, set the price of crude oil unilaterally. They cut the posted price twice in two years without consulting producing countries. The producers got together and decided they would coordinate their decisions instead of being price-takers.

Other producers joined over the decades. Qatar in 1961. Libya and Indonesia in 1962. The UAE, originally as Abu Dhabi, in 1967. Algeria in 1969. Nigeria in 1971. Several others followed.

At the time of the UAE announcement, OPEC had 12 member countries after Angola exited in January 2024 over a quota dispute. Once the UAE exit takes effect, that falls to 11. The bigger group, OPEC+, was created in December 2016, when OPEC members joined with 10 non-OPEC producers, most importantly Russia, to coordinate output cuts after the 2014 oil price collapse. OPEC+ together represents roughly 40-something percent of global oil supply on any given month.

That is the whole structure. A coordination club, with a Secretariat in Vienna, that meets several times a year and decides who pumps how much.

How the cartel actually works

OPEC and OPEC+ work through quotas. Each member is given a production ceiling expressed in barrels per day. Quotas are set against agreed reference baselines, political numbers that are supposed to reflect production capability, but often lag behind reality. Members vote to adjust quotas when prices or demand shift.

That is the theory. The practice is messier. Compliance is voluntary. There is no enforcement mechanism beyond political pressure and reputation. When a member’s real capacity grows faster than its baseline, the quota starts to feel like a tax. The country is sitting on barrels it cannot sell.

That is exactly what happened to the UAE.

📬 Never miss a signal

If this is your first time reading Flux Kinetics, every weekly deep dive lands free in your inbox. No noise, no filler, just what actually moved the tape.

I have watched cartels in three different commodities over fifteen years. The pattern repeats. Members who lost an internal argument about their fair share never forget. They build capacity quietly while the meeting minutes say everyone agreed.

Why the UAE walked

Recent reporting places the UAE’s effective OPEC+ limit in the 3.2 to 3.5 million barrel a day range, depending on whether voluntary adjustments are included... Reuters cited a quota of about 3.5 million barrels a day, while CNN cited an effective cap near 3.2 million. Per the BBC citing OPEC’s own figures, the UAE produced 2.9 million barrels a day in 2024.

UAE output was around 3.4 million barrels a day before the Hormuz disruption. Capacity is higher. EIA has cited ADNOC’s official production capacity around 4.5 million barrels a day, with other estimates in the 4.3 to 4.4 million barrel a day range.

The strategic target remains 5 million barrels a day by 2027.

That gap is the entire story. Spare capacity that cannot be produced generates no revenue.

“Our exit at this time is the right time for it, because it will have a minimum impact on the price.” said Suhail Al Mazrouei, UAE Energy Minister, to CNBC, April 28 2026

Here is the financial logic, in numbers anyone can run. If you think about it, freer production could generate roughly $50 billion or more in additional annual revenue once UAE capacity expansion completes.

At one million additional barrels a day and $90 oil, you are looking at $32.9 billion a year. At 1.5 million barrels and $100 oil, $54.8 billion. That is on top of what the country already earns…

Now look at the capital being deployed alongside that opportunity. ADNOC’s board approved a $150 billion capex plan for 2026 to 2030. The international investment arm, called XRG, was valued at $151 billion, up from roughly $80 billion at its launch a year earlier. That is the financial preparation of a company about to operate under different rules.

The capacity quota math

Strip the politics back. The UAE has been arguing for a higher baseline since 2021, when an OPEC+ meeting nearly collapsed publicly over Abu Dhabi’s refusal to extend cuts without recognition of its expanded capacity. The dispute was patched but it seems the grievance was not

.Five years of capacity build-out followed. ADNOC’s $150 billion capex was not a contingency plan for a possible exit. It was the construction of an industrial machine that needs to run above the quota ceiling to pay for itself.

OPEC+ share of global oil supply fell to 44% in March 2026, down from roughly 48% in February. That decline was driven primarily by current shipping constraints in the Gulf region, where vessel traffic has been disrupted, forcing production shut-ins and leaving Brent trading between $108 and $113 a barrel through the second half of April.

This is not purely a structural market-share loss, It does show how quickly OPEC+ control can shrink when physical flows break. May share will print lower again as one of the group’s largest producers walks.

Here is the catch: Quota freedom is worthless without flow path. The Habshan-Fujairah pipeline, which carries UAE crude past the Strait of Hormuz to the Gulf of Oman, has a capacity of 1.5 million barrels a day. That pipeline is the only route to market that does not depend on Hormuz traffic. Until shipping in the Strait become normal, UAE’s exportable upside is capped well below its production capacity.

The exit is sovereign. The export plumbing is not.

What changes from May 1

Three things shift the day the UAE leaves.

First, Saudi Arabia becomes the only credible swing producer inside the remaining OPEC core. Saudi Arabia carries roughly 3 million barrels a day of spare capacity, per The Middle East Insider’s April 22 estimate. That number used to be the cartel’s collective insurance. As of May 1 it is one country’s. Every barrel Riyadh withholds to defend price now subsidises UAE market share. That arithmetic does not survive long.

Second, the cartel’s enforcement credibility is now publicly testable. Angola left in January 2024 over a quota dispute. The cartel was unbothered. Angola produced about 1.1 million barrels a day. The UAE produces far more, with a capacity target of five. Iraq has a capacity-quota gap. Kuwait has one. Kazakhstan has one. None of them have ADNOC’s balance sheet, but every one of them now has a public template showing the cost of leaving is known and survivable.

🔁 Found this useful?

Flux Kinetics runs on word of mouth. If this analysis sharpened how you see OPEC, one forward to the right person is worth more than any algorithm.

📨 Share this issue

Third, the shape of UAE itself changes. The country is no longer a quota-bound member of a producer cartel. With $150 billion in capex and $151 billion of international investment firepower in XRG, ADNOC starts to look more like a vertically integrated oil, gas, LNG and chemicals major, closer in shape to TotalEnergies than to a traditional Gulf national oil company. The first major XRG external acquisition after May 1 will tell the market which segment the UAE is buying into. My working assumption is LNG offtake or downstream chemicals in Asia, where most future demand growth lives.

What kills the thesis

The structural reading breaks if the UAE quietly returns to OPEC inside eighteen months, or if ADNOC’s 5 million barrel capacity claim slips materially past 2028, or if Saudi Arabia announces a coordinated framework reset that turns this from an unwind into a controlled restructuring. Each of those is observable. None is currently visible.

If UAE output remains materially below 3.5 million barrels a day after Hormuz normalises, the market will conclude that capacity, infrastructure, or reservoir management, not OPEC, was the binding constraint.

If Gulf shipping is back to normal by Q3 2026 and UAE production lifts toward 4 million barrels a day within ninety days, the thesis confirms in price action. Murban is already independently priced.

The signal to watch is whether the Murban-Brent spread loosens as Abu Dhabi tests higher volumes outside OPEC+ discipline. That is the first market signal worth watching.

What this means for you, in five steps

For consumers. More UAE barrels in the medium term, once Gulf shipping normalises, points to lower oil prices than a still-coordinated cartel would have produced. Not immediately. Over 12 to 24 months.

The constraint is the pipeline, not the politics

Brent normalization depends on Strait of Hormuz traffic, not the OPEC announcement

For investors in oil majors. Saudi Aramco’s role gets harder. ADNOC, soon less constrained, gets easier.

Watch the June 2026 OPEC meeting for signals on Saudi posture

If Iraq raises a quota grievance publicly, the pattern is alive

For investors in oil services and infrastructure. UAE upstream capex of $150 billion across 2026-2030 is direct addressable spend.

Drilling, completions, subsea, FPSO operators with Gulf exposure benefit

Pipeline expansion announcements are leading indicators

For traders. Start tracking the Murban-Brent spread weekly.

If Murban trades looser than Brent as UAE flexes, the cartel premium is being repriced in real time

For policy watchers. The cartel is not dead, but the architecture of price coordination has lost a load-bearing column.

Saudi spare capacity, around 3 million barrels a day, is now the single point of failure

Angola was a tremor, UAE is the fault line

Closing

The cartel is not dead. It is one column lighter. Saudi Arabia is now defending price discipline alone with finite spare capacity, while one of OPEC’s largest producers is free to pursue market share with $150 billion of capex behind it and a 5 million barrel a day target six years pulled forward.

By Q1 2027 the question will be whether OPEC can manage prices and starts being whether OPEC can manage its own membership. The institutional architecture of global oil price coordination, intact since that five-day meeting in Baghdad in 1960, is now a publicly testable variable rather than a working assumption.

You are no longer reading a wire-service news brief. You are reading the largest load-bearing failure of OPEC+ quota credibility in the modern era, explained from the bottom up.

⚡ One last thing

If this improved how you see OPEC+, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm.

📨 Share • 📬 Subscribe • 💬 Leave a comment

Coming next:

The Gold To Silver Ratio As A Stress Gauge For The Energy Transition

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

Thank you for the clear and straightforward explanation. I have a much better understanding of how OPEC works now.

👍🏻

Amazing one ! Thank you. Let’s see how market will react after straight come back to normal