The Week the Water Spoke...

What you need to know.

Dear Executives, Traders, Investors, and Friends

Friday closed with Brent around $101.29/bbl and WTI near $95.42/bbl.

Both finished the week softer. Brent eased into the close. WTI followed.

Here is the part that matters:

The Strait of Hormuz, the narrow waterway that ships about one in every five barrels of oil consumed in the world, finished its tenth week effectively closed. Also, on Sunday May 3, OPEC+ raised June output quotas by another 188,000 barrels per day.

The cartel raised supply targets while the route that ships its oil stayed “shut”.

Read that twice.

If price is the headline, the water is the commitment. This week, the water did the talking.

Quick word for newer readers:

OPEC: The producer group that sets oil supply targets for its members.

Quota: The production limit each member agrees to follow.

Floating storage: Crude already loaded onto tankers but not yet delivered. Think of it as a parking lot for barrels at sea.

VLCC: A Very Large Crude Carrier, the standard tanker that holds about 2 million barrels.

The Cape route: Going around the southern tip of Africa instead of through the shorter Suez and Hormuz path. Cape route adds about three weeks to a voyage and changes the freight cost dramatically.

📬 Never miss a signal

If this is your first time reading Flux Kinetics, every weekly note lands free in your inbox. No noise, no filler, just what actually moved the tape.

The Scoreboard

Brent: $101.29/bbl, fractionally softer on the week, with the front-month easing as paper traders sold the OPEC+ hike.

WTI: $95.42/bbl, softer in line with Brent, with the spread between the two staying wide.

Henry Hub gas: $2.75/MMBtu, holding bid as LNG export plants kept pulling hard and the storage refill came in soft.

TTF gas: €44.14/MWh, easing €1.62 on the week, with European storage refilling steady but Asian buyers keeping cargoes pulled east.

JKM LNG: $16.87/MMBtu, with Asia still active in spot LNG buying and the Atlantic-Asia spread structurally wide.

Gold: $4,723/oz, higher on the week as funds covered short positions before the Federal Reserve meeting.

Silver: $80.85/oz, doing the heavier work, with the gold-silver ratio compressing.

Copper (LME 3M): $13,700/t, holding firm, with near-term tightness showing up in the spreads.

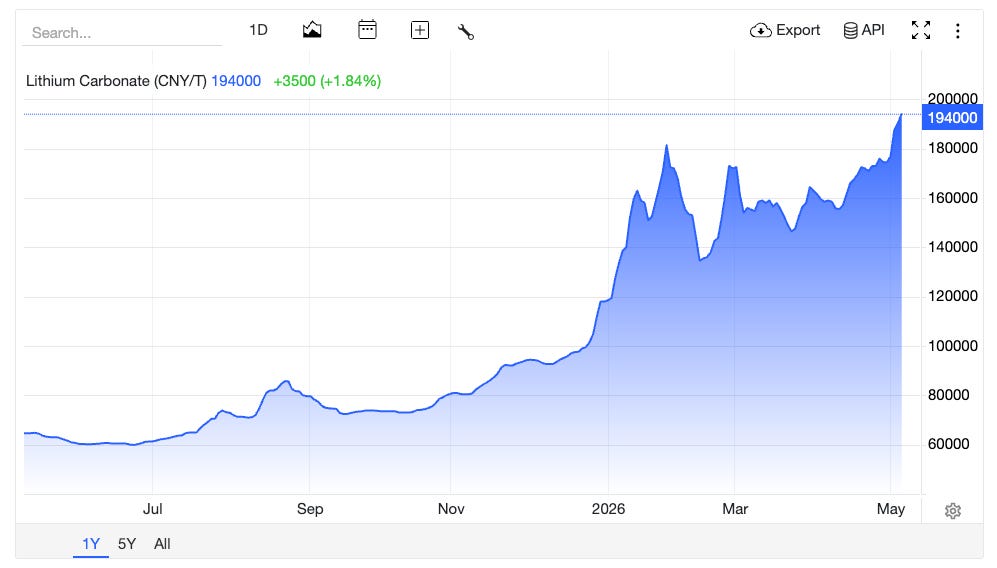

Lithium carbonate (China, battery grade): s194,000 CNY/t.

1. The Hormuz reality

Lloyd’s List had the cleanest math this week. VLCC tonne-miles are up while VLCC tonnes carried are down 36% year-on-year. Translation: the same fleet of tankers is sailing further to deliver less crude. That is what a chokepoint does to physics. It does not stop the steel from moving. It forces the steel to take a longer route.

For newer readers: A chokepoint is a narrow passage where a lot of trade has to pass through. When it closes or slows, every alternative becomes more expensive and slower. Tonne-miles measures the work a tanker fleet does. More tonne-miles for the same fleet means longer voyages. Less tonnes carried means less oil actually delivered.

Day rates tell the same story from a different angle. The tanker market has split into two tiers. Tankers that can take the Cape route are collecting record freight rates because the long way around Africa is suddenly the only way around. Tankers stuck on the Gulf side sit idle and uneconomic. One fleet, two markets, one chokepoint.

Day rates are the price to charter a tanker for one day of voyage. When the same vessel can earn double on a different route, owners reposition fast. When they cannot reposition, the rate collapses on the trapped side and spikes on the available side. That is happening right now.

Floating storage tells the story from the other end. Reporting from El País put combined Gulf floating stockpiles at roughly 30 million barrels at the end of April, up from under 25 million the month before. Those barrels exist on tankers without a clear destination. They are owned. They are loaded. They cannot move at scale until Hormuz clears or until the owners accept the cost of the long way around.

🔁 Found this useful?

Flux Kinetics runs on word of mouth. If this note sharpened how you see the week, one forward to the right person is worth more than any algorithm.

2. The OPEC+ paper barrel

A quota you cannot lift is a sentence on paper. The water decides what it means.

This is where the “Belief vs Reality” Gap opened wide this week… Most of the financial press read the OPEC+ June hike of 188,000 barrels per day as added supply pressure. The shipping data read it as something else. The missing point: most OPEC+ members cannot meet their existing targets while the route is constrained… Adding more on paper does not move a barrel across a closed strait.

Here is the catch: If the Chockepoint reopens in June, the new 188,000 barrels per day arrives on top of a backlog of physical barrels currently sitting in floating storage. That outcome is bearish. If it stays shut, the new quota is a press release and the front of the curve is mispriced low. You can consider either path as a tradeable asymmetry…We are not so sure.

The Flux Kinetics Number: 30 million barrels. That is the floating storage now sitting in and around the Gulf, up roughly 5 million on the month as shared above. It is the biggest physical inventory build the market is not pricing because it cannot reach a delivery point...

When the cartel raises quotas it cannot ship, the press release is louder than the cargo manifest. We watch the manifest.

In case you missed last week’s piece on the UAE leaving OPEC and ADNOC’s $55 billion contractor pipeline, the two stories now read as one sequence :

3. The two US gas markets

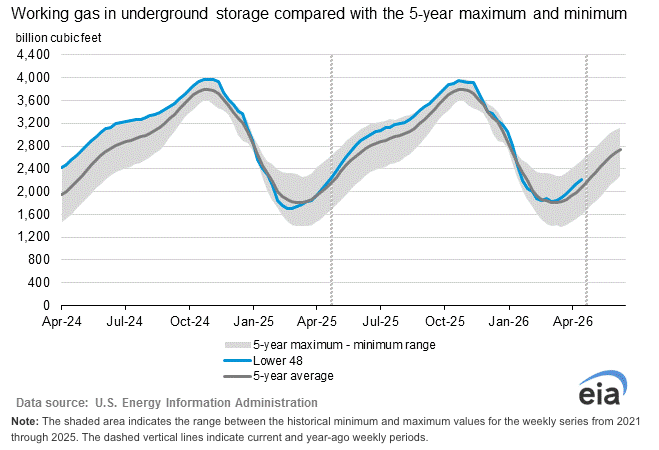

EIA reported a 63 Bcf injection for the week ending May 1, taking US working gas storage to 2,205 Bcf. That is a soft injection for the first week of May. The five-year average for that week is normally higher.

Henry Hub responded by holding the $2.780/MMBtu front-month into Friday’s close. The forward curve steepened. July sits at $3.04. August at $3.10. October at $3.15.

For newer readers: An injection is gas going into storage rather than coming out. Storage typically refills from April through October, then drains November through March. A soft injection during refill season tells you that demand is competing harder than usual with the storage pull. Bcf means billion cubic feet. Henry Hub is the main US natural gas pricing point in Louisiana

The reason is not weather. It is the export door. US LNG feedgas averaged 18.85 Bcf/d year-to-date and briefly touched 20.1 Bcf/d in early April per Natural Gas Intelligence. That is not a peak. That is a floor with new export trains coming on later this year and into 2027.

Domestic US gas is comfortable on storage. LNG linked gas is structurally tight on liquefaction throughput. The same molecule has two prices depending on whether it can reach a ship.JKM, the main Asian LNG benchmark, is sitting at $16.87/MMBtu. The spread between Atlantic and Asian gas is wide. US LNG terminals are pulling hard because they own the route out.

4. The metals triad

Three metals moved for three different reasons this week. Treating them as one trade is the mistake.

Gold closed Friday around $4,723/oz, higher on the week, with most of the move coming late as funds covered short positions before the Fed meeting. Silver did the heavier work at $81.33/oz, outperforming on the day and on the week. The gold-silver ratio compressed.

For newer readers: The gold-silver ratio is how many ounces of silver it takes to buy one ounce of gold. A compressing ratio means silver is catching up, usually because industrial demand is alive (solar, EVs, electronics). Funds covering short positions means traders who had bet on lower prices are buying back to close those bets, which pushes prices up.

Copper held near $13,100/t on the LME three-month contract. The story under that price is the grid. ADNOC’s $55 billion contractor pipeline announced last week is one driver. US data center buildout is another. China’s Q2 industrial restock is the third. All three pull on the same copper book at the same time.

Lithium carbonate in China printed roughly 194,000 CNY/t. The narrative coming into this week was that lithium was structurally oversupplied through 2027…

The Flux Kinetics Trade:

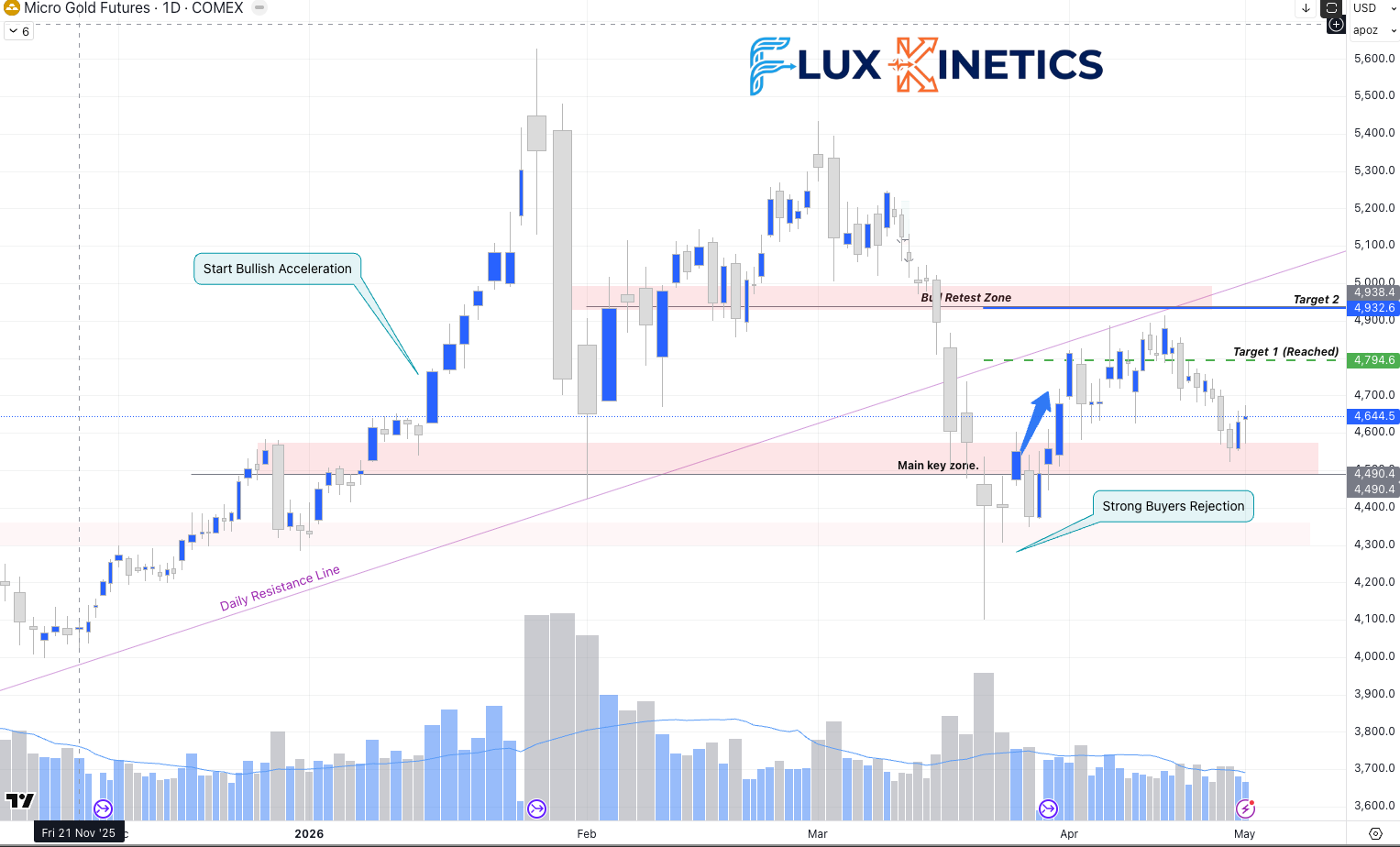

If you followed last week’s trade, congratulations. You should be sitting at +4% for the week. A good idea would be to close your position when the market opens tomorrow...

This week, no trade idea will be given because of the vey high volatility related to the peace deal between the US and Iran, and the key and most weighted visit of Trump to China.

This week, relax and watch what will be the new market direction. Then you can jump in the train.

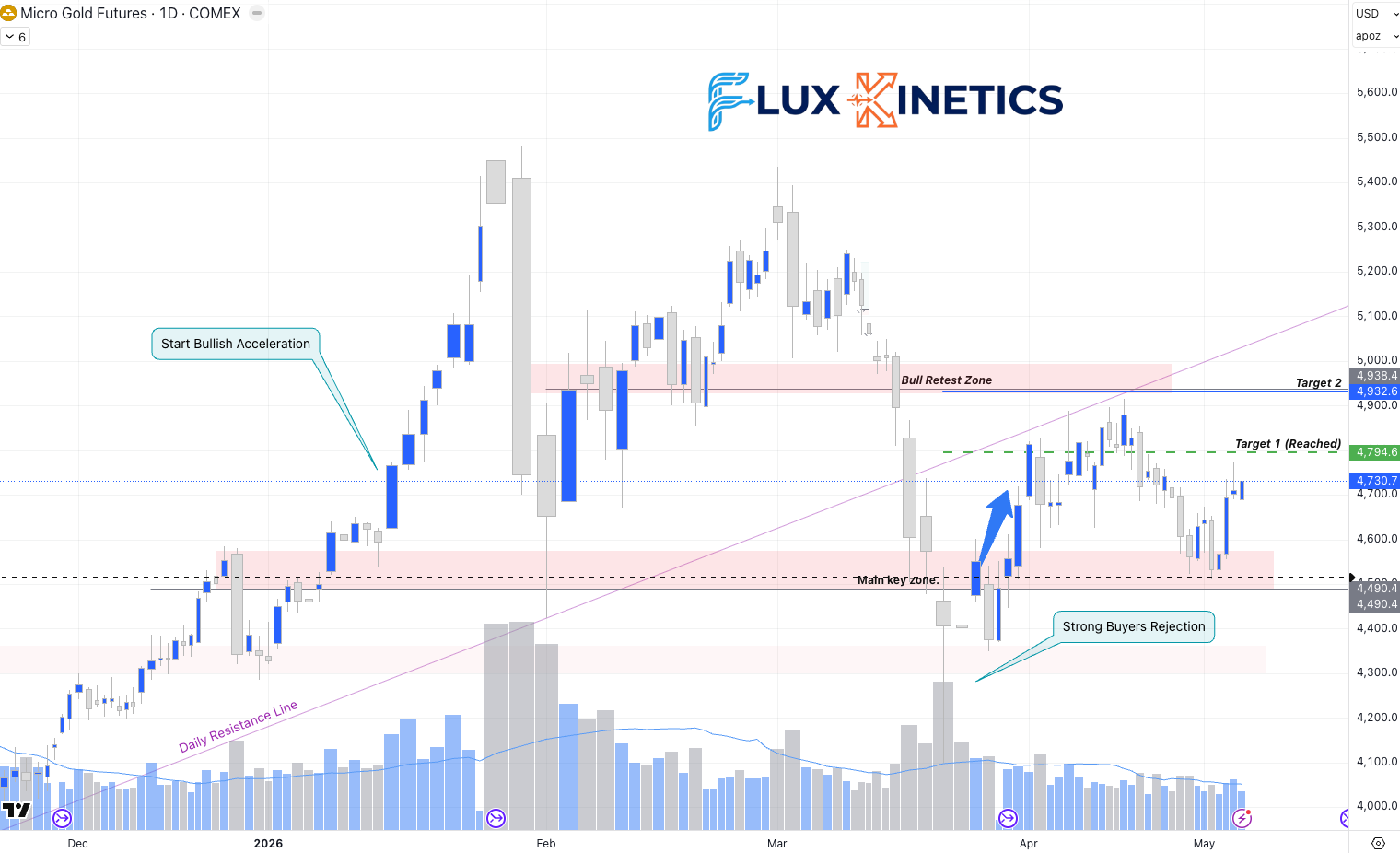

Last week idea, “If we come back to the main key zone at 4,500, then I would watch carefully if the zone rejected. If yes, then it can be a good second option to enter to play a long trend. If it broke down, then we can have a short activated toward 4,300” :

This week, 4,500$ tested and rejected, long trade activated, we’ve almost reaching our previous Target 1 :

Week ahead

Wednesday May 13: EIA crude print. After last week’s 2.3 million barrel draw, consensus is for a small build.

Thursday May 14: EIA gas storage.

Thursday May 14: Trump visit to CHINA-Day1. US PPI print. If services PPI runs hot… the gold-silver bid extends.

Friday May 15: Trump visit to CHINA-Day2. CME options expiry plus Baker Hughes rig count.

Action items

I would prefer infrastructure over pure commodity exposure. That means:

LNG infrastructure owners with operating cash flow now.

Cape-capable tanker operators collecting the two-tier freight premium.

Copper miners with grid and data centers exposure.

Buy the builders. Be selective with the barrels.

If this changed how you see the week, send it to one person who needs to see it too.

⚡ One last thing

If this changed how you see the week, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm.

📨 Share • 📬 Subscribe • 💬 Leave a comment

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.