Solar Isn’t Dead. It’s Just Ruthless.

Why smart money is sprinting while the rest of the market sleeps.

By Flux Kinetics February 11, 2026

IN THIS ISSUE:

The Physics: Why 1.12 eV is the most important number in your portfolio.

The Tech: The war between TOPCon and HJT (and the silver trap).

The Supply Chain: “Clean Poly” vs. “China Poly.”

The Law: Why July 4, 2026 is the new critical deadline.

The Playbook: How to position for the “Safe Harbor” sprint.

If you looked at the headline numbers for 2025, you might think the energy transition is on autopilot. Solar met 61% of U.S. electricity demand growth last year. Batteries are finally smoothing out the jagged edges of intermittency.

But if you are reading this in February 2026, you know the real story isn’t the capacity. It’s the chaos.

Following the passage of the One Big Beautiful Bill Act (OBBBA) last July, the market has bifurcated. We are staring down a hard “cliff edge” for tax credits in 2027 and a “Safe Harbor” deadline of July 4, 2026, that has every developer in the country scrambling to break ground.

The “dumb money” is fleeing the policy uncertainty. The “smart money” is looking past the legislative theater to the physics. Because whether Congress likes it or not, the “photon arbitrage”, the spread between harvesting sunlight and selling electrons to AI data centers, has never been wider.

To know if a utility’s CAPEX plan is viable or if a silver shortage will flatline a project in Arizona, you need to look under the hood. You need to understand the machine.

1. The Physics of Money (And the 1.12 eV Ceiling)

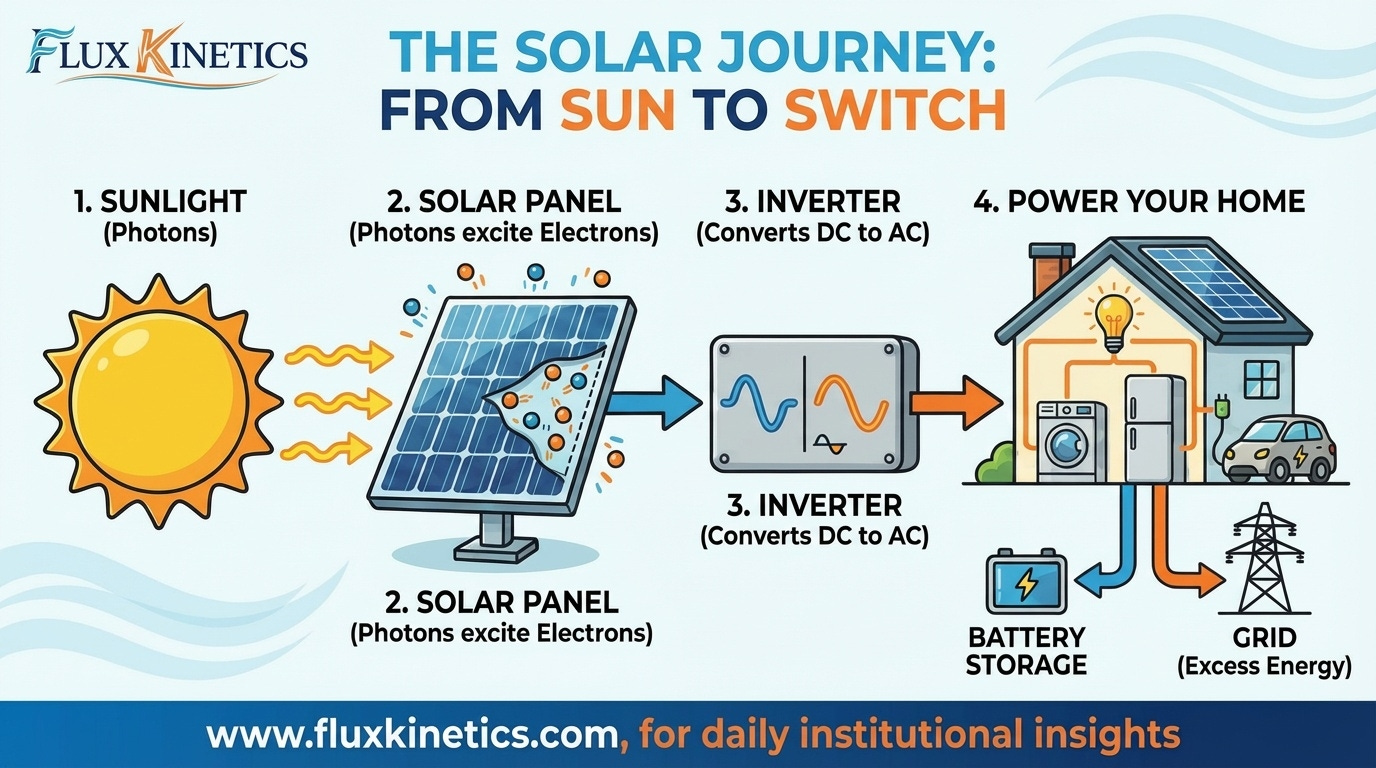

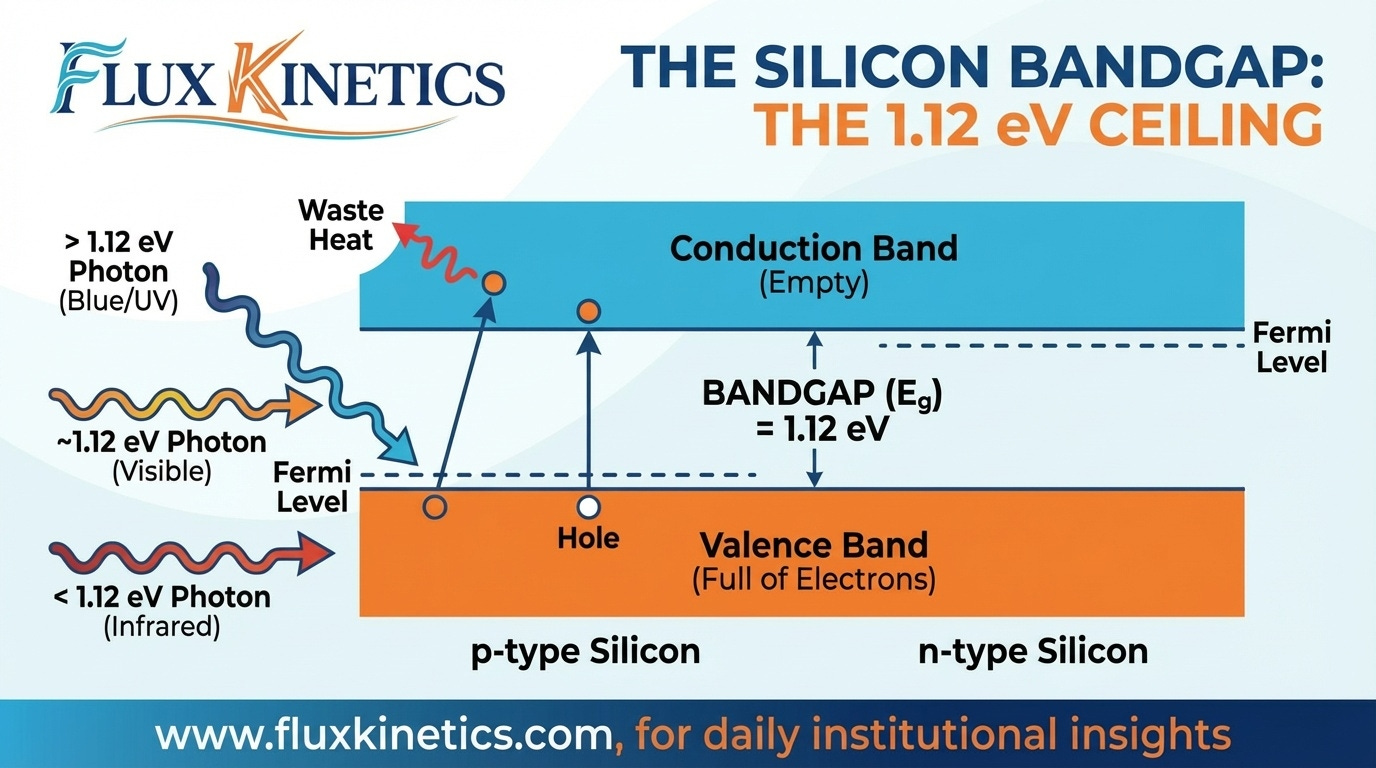

At its heart, solar energy is a game of subatomic billiards dictated by a single number: 1.12 electron-volts (eV).

The fundamental unit of a solar panel is the photovoltaic (PV) cell, typically made of silicon. Silicon is a semiconductor, which means it’s an insulator until you force it to work. We do this by doping: spiking one side with phosphorus (N-Type, extra electrons) and the other with boron (P-Type, extra “holes”).

When you sandwich these layers, they create a p-n junction—a one-way turnstile for electrons.

Here is where the 1.12 eV comes in. This is the Bandgap. To knock an electron loose and create current, a photon must hit the silicon with at least 1.12 eV of force.

Too weak? The photon passes right through. Invisible.

Too strong? The photon knocks the electron loose, but the excess energy turns into waste heat.

This Bandgap is why standard silicon panels hit a theoretical efficiency ceiling of about 33% (the Shockley-Queisser Limit). No matter how good your manufacturing is, you cannot break physics. To get higher returns, we need new materials.

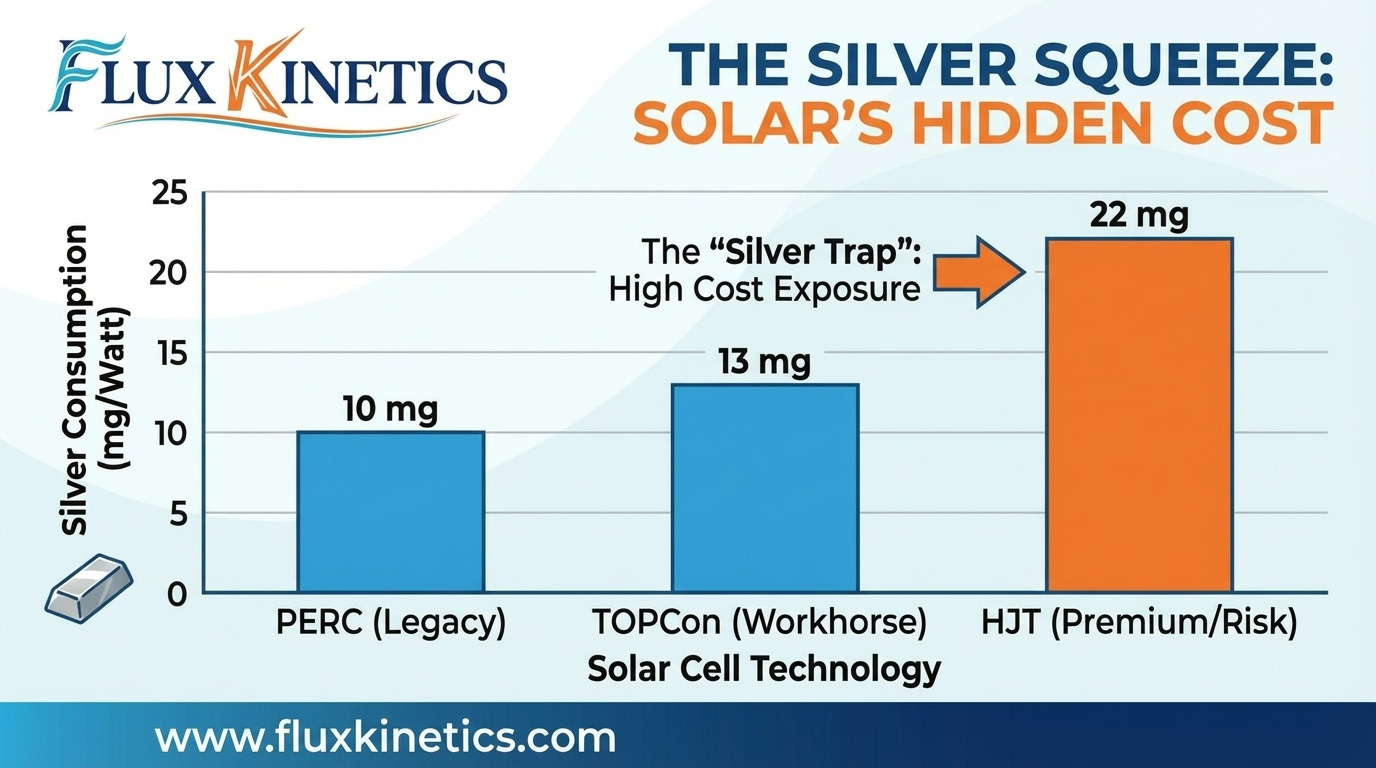

2. The Hardware Wars: TOPCon vs. HJT

Not all solar is created equal. In 2026, the market is fighting a war between two technologies, and the winner depends entirely on the price of silver.

TOPCon (Tunnel Oxide Passivated Contact): The Safe Bet

This is the current workhorse. It adds a microscopic oxide layer to reduce electron loss.

The Economics: It integrates easily into existing factories. It’s what the Chinese majors (Jinko, Trina) are shipping by the gigawatt.

The Cost: It uses about 13 mg of silver per watt.

HJT (Heterojunction) – The Silver Trap

This is the premium challenger. It combines crystalline silicon with thin-film layers. It performs better in high heat, which is crucial for Texas and Arizona projects.

The Catch: Silver. HJT cells guzzle an average of 22 mg of silver per watt.

The Risk: If silver spot prices break $40/oz, HJT margins evaporate. Unless a manufacturer has mastered copper plating (replacing silver with copper), HJT is a dangerous play.

The Holy Grail: Perovskite Tandems

This is the venture capital darling. By stacking a perovskite cell (which catches blue light) on top of silicon (which catches red light), we bypass the 1.12 eV limit. LONGi set a 34.85% efficiency record last year. The race is now on to prove they can last 25 years without degrading in the rain.

3. The Supply Chain: “Clean Poly” vs. “China Poly”

The OBBBA didn’t just change tax credits; it weaponised the supply chain.

We now have a two-tier market for Polysilicon (the refined sand used to make cells):

“China Poly” ($5-8/kg): Cheap, abundant, 80% of global supply. Used by the rest of the world.

“Clean Poly” (Premium): Sourced from the US (Hemlock) or Germany (Wacker).

The Kicker: To qualify for the OBBBA’s tax credits, you generally cannot use components from a “Foreign Entity of Concern” (FEOC). This has created a massive premium for non-Chinese poly-silicon.

If a developer is pitching you a project with “standard costs” but expects “full tax credits,” check their supply chain. They might be lying to themselves.

Geopolitical Alpha: The bottleneck isn’t the panel assembly; it’s the wafer. The US produces almost zero wafers. This is the strategic vulnerability to watch.

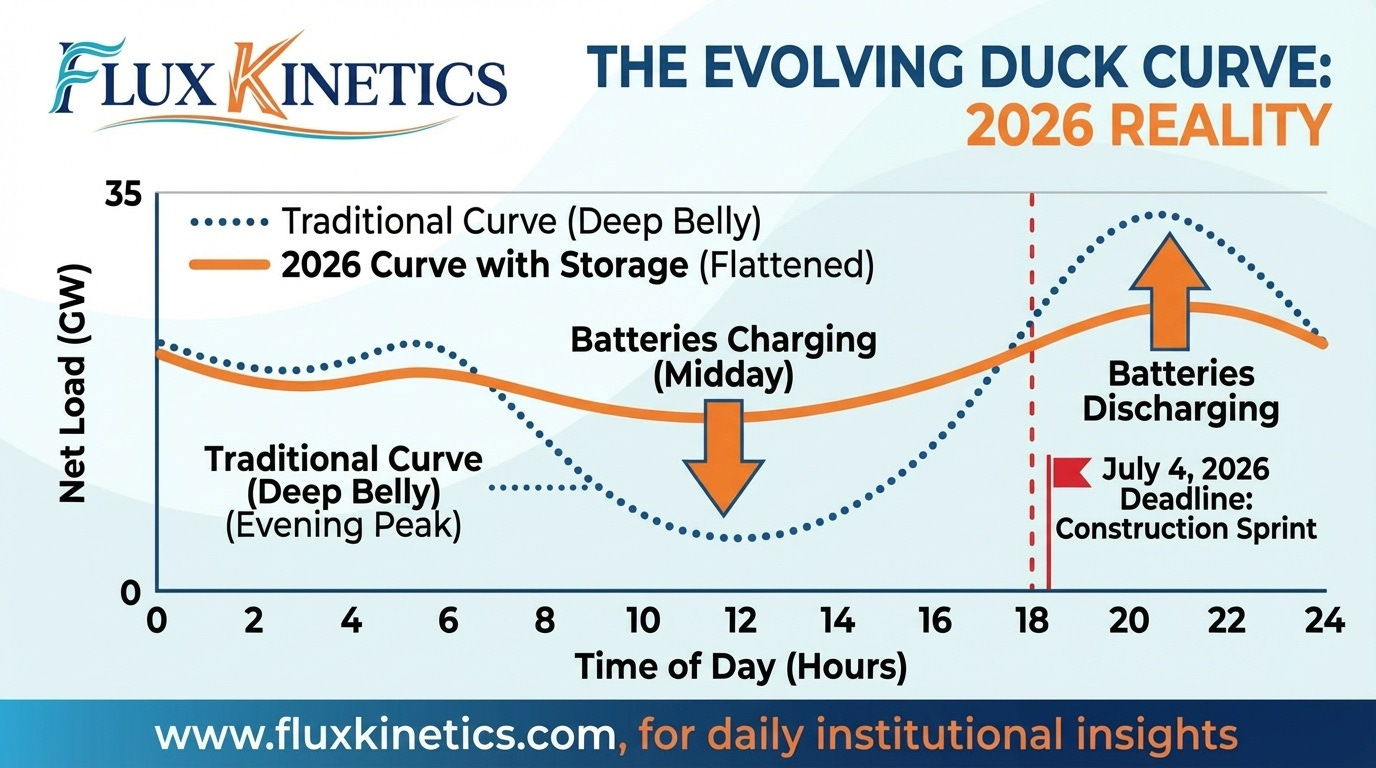

4. The Grid & The Law: The July 4th Sprint

The old problem was the Duck Curve (too much solar at noon). The solution is now standard: Solar + Storage. In 2026, a standalone solar project in California is effectively worthless. The value is in the battery arbitrage.

But the new problem is the calendar.

The OBBBA reintroduced a “Safe Harbor” deadline. To qualify for the current tier of tax credits before the 2027 phase-out, projects must “Begin Construction” by July 4, 2026.

The Rush: We are seeing a frantic sprint to put shovels in the ground in Q1 and Q2 2026.

The Bottleneck: Transformers and Interconnection. You can have the panels, but if you can’t get a transformer delivered to the site to prove “physical work,” you miss the deadline.

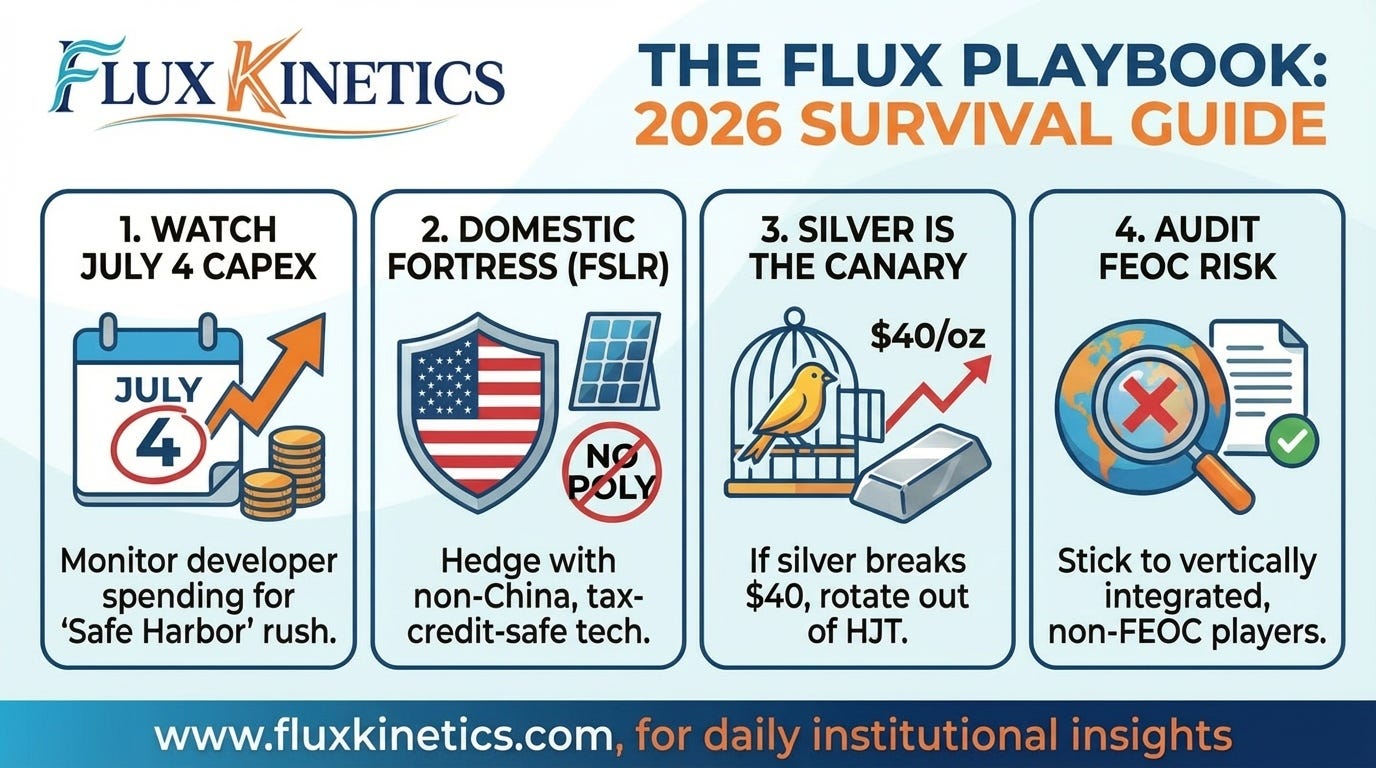

The Flux Playbook: 2026 Survival Guide

The macro environment is messy, but the micro signals are clear. Here is your checklist for Q1:

Watch the “July 4” Capex Spike: Monitor the earnings calls of major US developers (NextEra, AES). Expect massive capital deployment in Q2 to hit the Safe Harbor deadline. High Capex now means a locked-in pipeline for 2027.

The “Domestic Fortress” Trade (FSLR): First Solar remains the hedge. Their thin-film tech uses no poly-silicon, making them immune to the China trade war, and they collect the 45X manufacturing credit that OBBBA left intact.

Silver is the Canary: If silver breaks $40/oz, take profits on HJT manufacturers and rotate into copper-plated tech or thin-film.

Audit the FEOC Risk: If a developer relies on Chinese wafers, their tax credit eligibility is a coin flip. Stick to vertically integrated players who control their own destiny.

Solar isn’t just “green energy” anymore. It is a brutal, low-margin industrial commodity that anchors the global grid. The physics are settled. The risk has moved to the mine, the map, and the US Code.

Stay sharp.

If you get value and more knowledge, please share it to reach and help more readers like you.

Join the Flux Kinetics community. I send thess intels every week in addition to Energy and Commodities market analysis.

Flux Kinetics - Where energy meets intelligence,

Wassim C.

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

This is excellent info. Do you find that the cost to install is coming down at all or still offering credits or rebates?