OPEC Got Smaller. ADNOC Got Bigger.

What you need to know this week

Abu Dhabi left the room. The CAPEX did the talking.

Dear Executives, Traders & Investors, Brilliant minds and Friends,

Friday closed with Brent at $108.17/bbl and WTI at $101.94/bbl.

Both sold off hard into the weekend. Brent fell 2.02% on Friday. WTI fell 2.98%.

Here is the part that matters: both still finished the week up about 2.95%. So no, this was not a clean bearish week. It was messier than that.

Oil fell on Friday. Products tightened. U.S. crude exports hit a record. Gas stayed cheap in America while LNG plants pulled harder and Abu Dhabi did something the oil market will still be pricing long after this week’s candles are forgotten.

Quick word for newer readers. OPEC is the producer group that coordinates oil supply. A quota is the production limit a member agrees to follow. Capex means capital expenditure, the money companies spend on wells, plants and platforms, pipelines, terminals, equipment, and long-life infrastructure. If price is the headline, capex is the commitment.

This week, the commitment was louder than the close.

This Week’s Settle

Brent: $108.17/bbl, down hard Friday but still +2.95% on the week, as crude stayed supported by physical draws and record U.S. exports.

WTI: $101.94/bbl, down hard Friday but still +2.95% on the week, with U.S. inventories falling while exports hit a record.

Henry Hub gas: $2.780/MMBtu, up about 10% on the week, as lower U.S. output met record LNG feedgas demand.

TTF gas: €45.77/MWh, with Europe still paying for imported molecules while U.S. gas stayed much cheaper.

JKM LNG: $16.865/MMBtu, with Asia still active in spot LNG buying.

Gold: $4,630/oz, high but no longer accelerating.

Silver: $76/oz, holding stronger than gold as industrial demand stayed alive.

Brief Contents

The UAE and ADNOC signal

The oil and product story

The gas and LNG split

Metals and battery inputs

SPR and capital flows

Week ahead

Action items

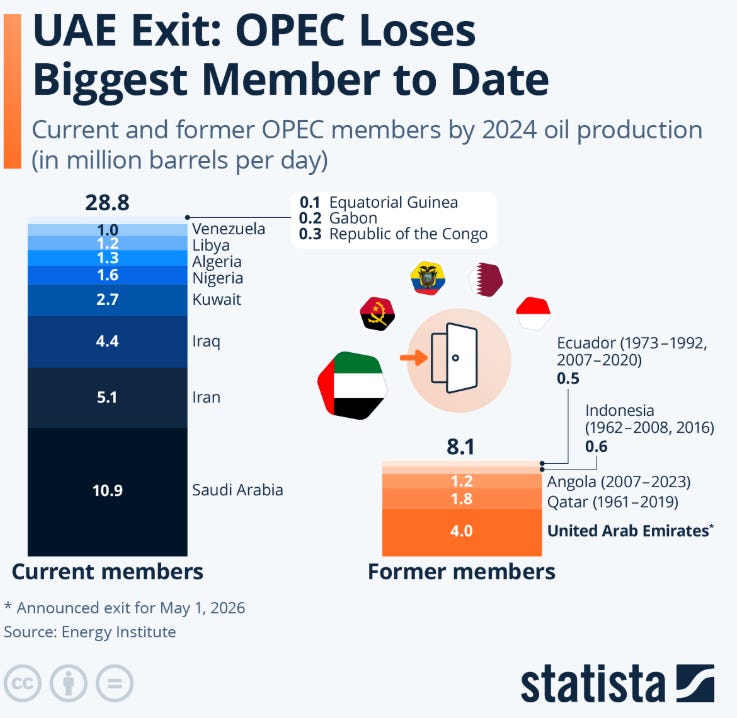

THE UAE STORY: Abu Dhabi Walked, ADNOC Funded The Next Phase.

The UAE announced on April 28 that it would leave OPEC and OPEC+, effective May 1.

For newer readers, here is the simple version. OPEC helps manage oil supply through agreed production limits. Those limits can support prices, but they can also restrict producers that have spent heavily to grow capacity.

That is where Abu Dhabi was sitting.

The UAE had capacity above its allowed output. ADNOC had already been building toward a 5 million barrel per day target by 2027. At some point, if you keep spending billions to build capacity but keep accepting limits on using it, the math starts to argue with the membership card.

This week, Abu Dhabi stopped arguing.

The UAE leaving OPEC is not a diplomacy story for me. It is a barrel-and-capex story. UAE’s exit became effective May 1, which gives Abu Dhabi more room to match production policy with its own capacity buildout. Then ADNOC put numbers behind the move: AED 200 billion, about $55 billion, in project awards for 2026 to 2028, supporting a wider five-year $150 billion CAPEX plan. That is the part that matters. More freedom on output only matters if the steel, rigs, processing plants, pipelines, and contractors are funded. ADNOC is funding them.

In case you missed my previous article on the UAE-OPEC split, I broke it down here:

This is where I want readers to slow down.

A production target is not a barrel.

A board-approved capex plan is not a completed plant.

A project award is not first oil.

But it is the start of the chain.

Money goes to EPC contractors. EPC means engineering, procurement, and construction. Those contractors order valves, compressors, turbines, pipe, steel, electrical systems, control systems, subsea equipment, and fabrication yard capacity. Operators then need crews, commissioning teams, logistics, spares, and uptime.

That is how capex becomes barrels. Not overnight… not imaginary either.

“When a national oil company funds the steel, the market should stop treating capacity as a footnote.”

The old story was quota discipline. The new story is execution discipline.

That is a major shift.

THE OIL STORY: The Draw Was Real. The Reason Matters.

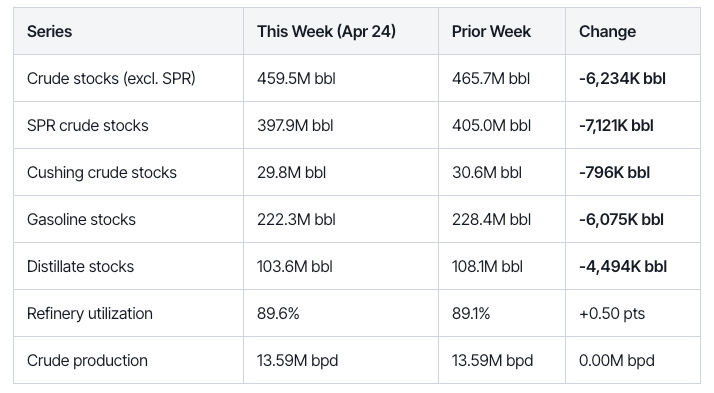

EIA’s weekly petroleum report showed U.S. commercial crude inventories fell 6.23 million barrels for the week ended April 24.

That looks bullish at first glance.

Gasoline stocks fell 6.08 million barrels. Distillates, which include diesel and heating oil, fell 4.49 million barrels. Refinery utilization rose to 89.6%.

For newer readers, inventories are the market’s fuel tank. When the tank drains, the system has less cushion. Less cushion means price becomes more sensitive to refinery problems, export pulls, and demand spikes.

U.S. crude exports rose to 6.438 million barrels per day, the highest on record. That is a massive number. Exports were up about 1.64 million barrels per day week over week.

Translation: a big part of the crude draw came because barrels left the country.

That does not mean the draw is fake. It means it was export-led.

That is different from saying U.S. domestic demand suddenly exploded.

The draw was barrels leaving the tank and moving to buyers. The bullish question is whether that export pace continues. The bearish question is what happens when it becomes normal again...

That is the number I am watching.

“A draw tells you the tank fell. The export line tells you why.”

Products were the tighter story.

Gasoline down 6.08 million barrels matters more to me than a crude chart that sold off on Friday. Gasoline is closer to the consumer. Diesel is closer to freight, industry, farms, mines, and logistics. When product stocks fall while refineries are already running near 90%, I do not call that loose.

I call that a market with less cushion than the headline suggests.

The Flux Kinetics Number: 6.438 million barrels per day →That is the record U.S. crude export print.

Found this useful?

Flux Kinetics grows reader by reader. If this note sharpened how you see the week, send it to one person on your team who still watches only the price chart.

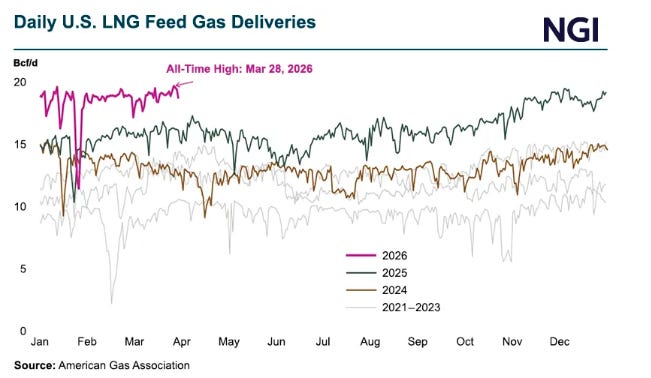

THE GAS AND LNG STORY: Cheap Gas, Expensive Exit Door.

Gas gave us the cleanest split of the week.

EIA reported U.S. working gas in storage at 2,142 Bcf for the week ended April 24. That was a 79 Bcf injection, leaving stocks 116 Bcf above last year and 153 Bcf above the five-year average.

For newer readers, Bcf means billion cubic feet. It is the storage unit for natural gas. If storage is above normal, that usually keeps pressure on prices.

And yet Henry Hub still finished the week around $2.780/MMBtu, up about 10%.

Why?

Because the U.S. has two gas markets living inside one country.

One market is domestic. It looks at storage, weather, power demand, and production.

The other is LNG linked… LNG means liquefied natural gas. Gas is cooled into liquid form so it can be loaded onto ships and sold overseas. Without LNG terminals, U.S. gas stays mostly trapped in North America. With LNG terminals, a molecule in Louisiana can compete for buyers in Europe or Asia.

U.S. LNG feedgas averaged a monthly record 18.8 Bcf/d in April.

Feedgas is the gas sent into LNG export plants.

That is the clean number.

It tells me export plants are pulling harder even while U.S. storage still looks comfortable. A cheap molecule is not useful if it cannot reach the buyer…

The Flux Kinetics Insider View: U.S. gas is cheap because storage is comfortable and some basins are constrained. U.S. LNG infrastructure is valuable because it owns the route out. The producer owns the molecule and the LNG chain owns the passport.

“The signal is not only in Henry Hub. It is in who owns the exit door.”

THE METALS STORY: Gold Paused. Copper And Lithium Still Matter.

Metals were not the main event this week, but I would not ignore them.

Gold stayed high, around $4,630/oz. But CFTC positioning showed managed money reduced some exposure. That does not mean gold is broken. It means some funds took risk off after a strong move.

For newer readers, CFTC positioning shows how different types of traders are positioned in futures markets. It is not perfect. It is not a timing tool by itself. But it helps me see whether big money is adding risk or cutting risk.

Copper stayed firm near $13,090/t on the LME 3M contract.

Copper matters because it is not just a chart. It is cables, transformers, power grids, industrial motors, electric vehicles, data centres, and ofshore platforms. When copper stays expensive, project budgets feel it.

That links directly back to ADNOC.

A $55 billion project award pipeline does not just pull oilfield services. It pulls steel, copper, electrical systems, control rooms, switchgear, compressors, pumps, valves, and fabrication capacity.

Energy capex becomes metals demand.

Not always on day one.

But eventually, through procurement.

My split is simple:

Gold is the financial stress asset.

Copper is the infrastructure asset.

Lithium is the battery-chain asset.

They do not all move for the same reason.

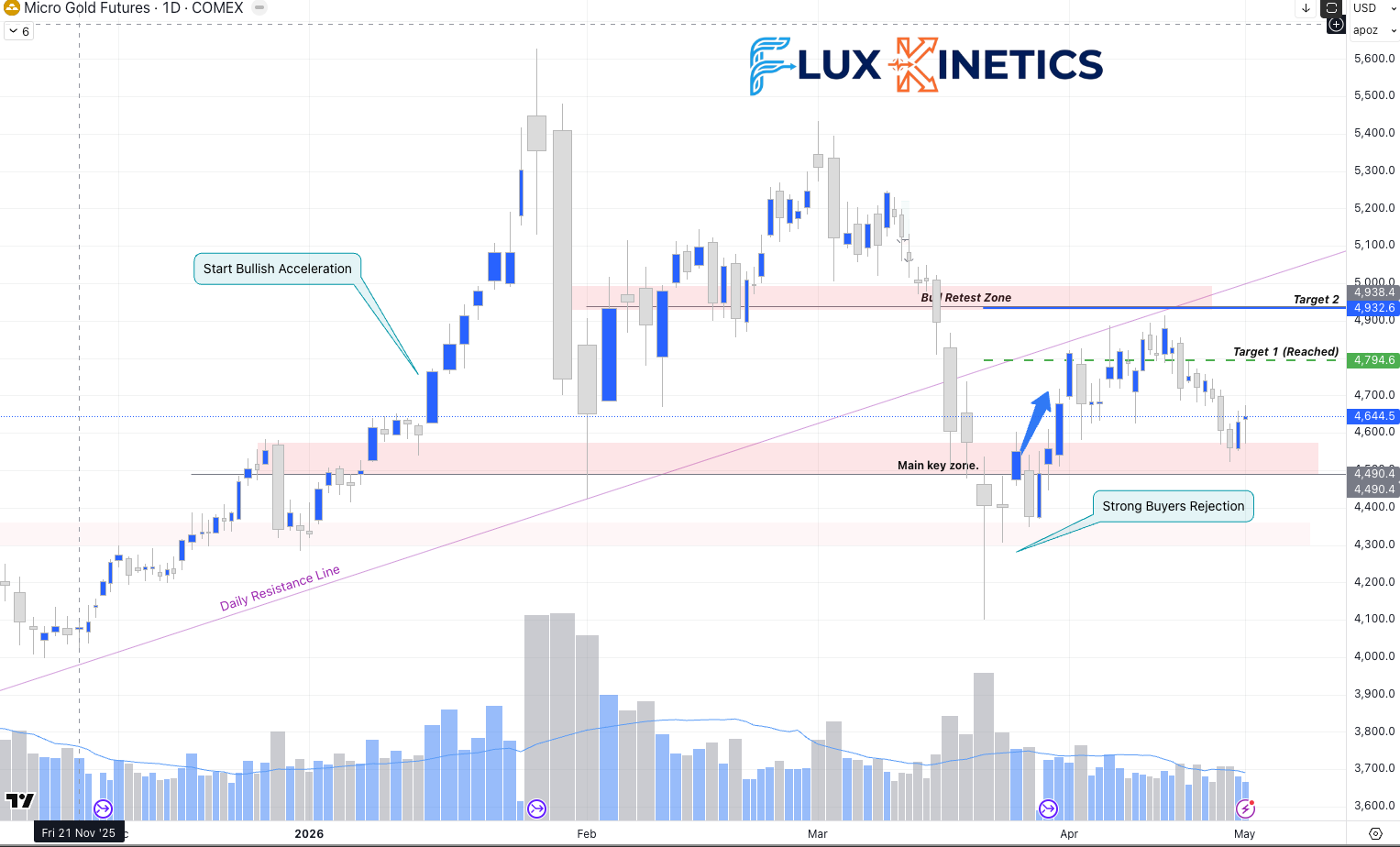

The Flux Kinetics Trade:

Gold didn’t hold the 4,660$ level and went back to the “main key zone” at 4,500. Could this be a good time to re-enter?

Gold has sold off until the Fed day decision, as markets want to be cautious to price any changes. After that, a small recovery toward 4,650 has happened.

The open of the week will be interesting. If we close above 4,700, a good opportunity can be to enter a long trade toward Target 1.

If we come back to the main key zone at 4,500, then I would watch carefully if the zone rejected. If yes, then it can be a good second option to enter to play a long trend. If it broke down, then we can have a short activated toward 4,300.

Never miss a signal

If this is your first time reading Flux Kinetics, this is what I do every Sunday before the market opens. No noise. No filler. Just the physical story behind the price.

POLICY AND CAPITAL: The SPR Chose The Curve.

The U.S. Department of Energy gave the market another important signal this week.

Reuters reported on April 30 that the DOE is seeking to loan companies up to 92.5 million barrels of crude from the Strategic Petroleum Reserve. Companies would return the barrels later, with up to a 24% premium in extra barrels.

For newer readers, SPR means Strategic Petroleum Reserve. It is the U.S. emergency crude stockpile.

A normal purchase would mean the government buys crude and refills the reserve. This was different. This was an exchange loan.

DOE lends barrels now and Companies return more barrels later.

That matters because it weakens the idea that the government is a fixed-price buyer under the market today. It also shows how policy can use the curve…

That is why I prefer infrastructure over pure commodity beta in weeks like this.

A commodity ETF gives you price movement.

An infrastructure owner gives you the toll road.

A contractor gets paid when the steel goes into the ground.

That difference matters.

“The best asset in a tight system is the gate everyone must pass through.”

Week Ahead: light macro week

Wednesday: EIA crude and product data. ADP Employment + ISM Manufacturing PMI

Thursday: EIA gas storage. Initial Jobless Claims

ADNOC project follow-through.

Action Items

For Traders

I would treat Brent around $108 as the pivot.

A daily close above $110.50 opens a move toward $118. I would be wrong below $104.80.

For WTI, $100 is the line. A daily close below $99.50 opens $97. A daily close back above $104.50 brings $110 into play.

Keep it simple. Trade the close.

Do not trade the headline…

For Operators

If you depend on gasoline supply, secure volumes early. Product inventories fell hard this week. Do not wait for another refinery update.

If you are building power, grid, LNG, upstream, or downstream projects, revisit copper and electrical-equipment assumptions. Quotes can move faster than budgets.

For Investors

I would prefer infrastructure over pure commodity exposure. That means:

LNG infrastructure owners

Electrical equipment and grid suppliers

Copper linked supply chains

Gulf industrial suppliers tied to ADNOC’s local manufacturing push

I would be careful with weak balance sheets. High prices can hide poor execution for a while… they do not fix bad assets.

Buy the builders.

Be selective with the barrels. Trugarez!

If this changed how you see the week, send it to one person who needs to see it too.

⚡ One last thing

If this changed how you see the week, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm.

📨 Share • 📬 Subscribe • 💬 Leave a comment

Coming next:

The Gold To Silver Ratio As A Stress Gauge For The Energy Transition

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

I agree with this completely, and I’ll say this upfront these kinds of breakdowns are exactly what people like me need, the pedestrians who are trying to learn more. Not because we don’t understand business or markets, but because the way it’s written cuts through the noise and makes complex global shifts actually usable. That’s rare.

Reading this, what stood out to me is how power is consolidating in a different way than most people realize. Everyone talks about OPEC like it’s still the same force it was decades ago, but this piece makes it clear the structure is evolving. It’s less about the collective and more about who inside that collective is actually executing, scaling, and positioning for the future. Abu Dhabi National Oil Company isn’t just participating, they’re expanding influence while others are managing decline or constraint. That shift matters.

From my world, this feels very familiar. I’ve seen this same pattern play out in product and business over and over. Groups, partnerships, industries they look strong from the outside, but internally, a few players are doing the real building while others are just maintaining position. Over time, the builders separate. They get faster, more aggressive, more forward looking. Then one day it looks like it happened overnight, but it didn’t. It was years of quiet positioning.

What I appreciate most here is how this connects dots without overcomplicating it. It gives guys like me who live in execution a clearer lens on macro movement. Because at the end of the day, whether it’s oil markets or launching a product, the principle is the same. The ones who move, adapt, and invest ahead of the curve end up owning the next phase.

These posts are doing something important. They’re not just informing, they’re building understanding. And for someone like me who came up learning everything the hard way without this kind of access or clarity, I can say this kind of content accelerates how people think. That’s real value.