Oil Hit A Hundred. Exit Now

Every spike needs someone to buy the top.

TABLE OF CONTENTS

Executive Summary

This Week’s Key Moves

Deep Dive: Hormuz, Hedging, And The Surplus Story

Week Ahead: What To Watch

Action Items

EXECUTIVE SUMMARY

War premium meets surplus math. Brent and WTI exploded higher, with Brent settling near 92 dollars and WTI around 91 dollars, as the war around Hormuz triggered the sharpest weekly oil rally since the Covid shock while six month backwardation flipped the curve into full crisis mode.

Stocks build into the spike. Crude inventories rose by around three and a half million barrels on the EIA print and more than five and a half million barrels on the API read as gasoline drew and distillates nudged higher, so commercial stocks climbed even while futures priced an imminent shortage and policymakers started hinting at direct futures market intervention.

Metals digest the volatility. Gold held above 5,100 dollars per ounce but logged its first weekly decline in five weeks while silver slipped back toward the mid eighties, leaving precious metals elevated but choppy as funding stress, a stronger dollar, and lingering war hedging forced a volatility reset rather than a full trend break.

THIS WEEK’S KEY MOVES

Oil: Brent settled at 92.69 dollars, WTI at 90.90 dollars, both sharply higher on the week, as the closure of Hormuz, talk of U S futures market measures, and producer hedging flows forced a violent repricing of supply risk and drove the front of the curve into steep backwardation.

Gas: Henry Hub near 3.00 dollars per MMBtu, fractionally softer on the week as mild weather eased residential demand even as feed gas flows into new Gulf Coast LNG capacity climbed and storage stayed above the five year average.

Gold: 5,114 dollars per ounce, lower on the week, as a stronger dollar and higher yields outweighed safe haven demand and turned the Bull Retest Zone into more of a volatility compression band than a trend reversal area.

Silver: Around 84.70 dollars per ounce, down from the recent spike highs, with the gold to silver ratio stabilising after January extremes as industrial buyers quietly rebuilt hedges into softer prices.

Lithium: China battery grade lithium carbonate near 141,000 yuan per tonne and around 16,700 dollars per tonne equivalent, consolidating after a strong second half rally as expectations for tighter balances met still cautious downstream battery demand.

If you trade the headline, you feed the pros.

DEEP DIVE: Hormuz, Hedging, And The Surplus Story

When a war shock hits a market that already expects a surplus, three things happen at once. Paper explodes higher, producers rush to lock in hedges, and the curve tells the truth about where barrels are really scarce. That is exactly what played out around Hormuz this week.

THE INFRASTRUCTURE OR FID STORY

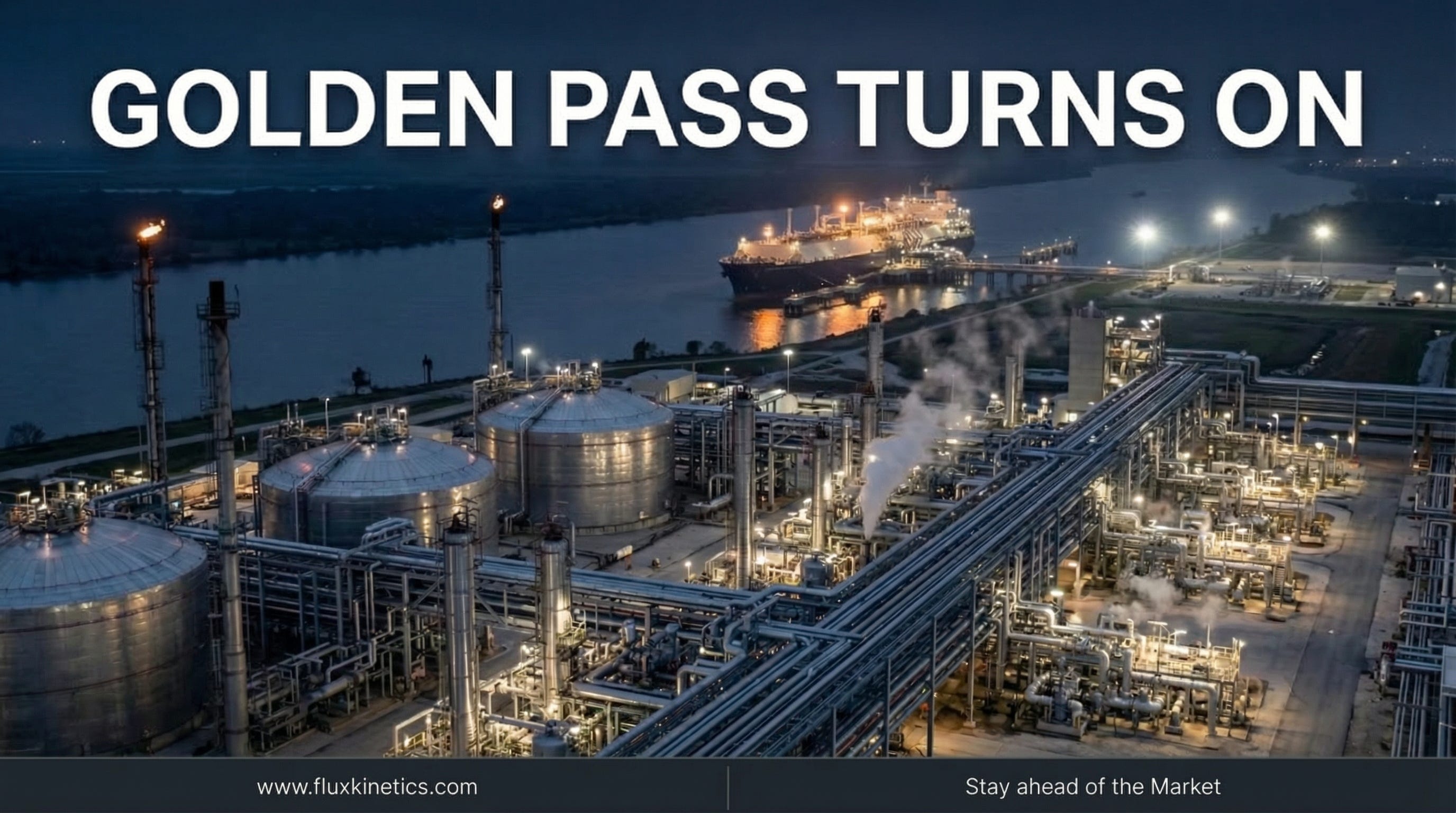

Golden Pass, the large LNG export plant backed by ExxonMobil and QatarEnergy on the Texas Gulf Coast, pulled in hundreds of millions of cubic feet per day of gas as it stepped into first LNG production. Years of delays, a bankrupt contractor, and a fresh export licence extension have turned a once marginal timeline into a live feed gas sink in a tight global gas balance.

The significance is bigger than a single terminal. Golden Pass links cheap Henry Hub molecules to Asian and European buyers exactly as Hormuz closures divert Qatari and other Gulf cargoes, which hard wires a new arbitrage between U S gas and war stressed LNG benchmarks and locks in years of high load factors on Gulf export infrastructure. Every extra cubic foot Golden Pass pulls is one less molecule Europe can count on if Gulf LNG sits behind drones and naval stand offs.

The Insider View: The bifurcation is that LNG equities priced Golden Pass years ago while the physical gas market only now feels the constant pull from new trains. The spread between Henry Hub and war inflated seaborne gas benchmarks is where the real optionality sits, not in the headline flat price of WTI.

THE METALS OR CRITICAL MINERALS STORY

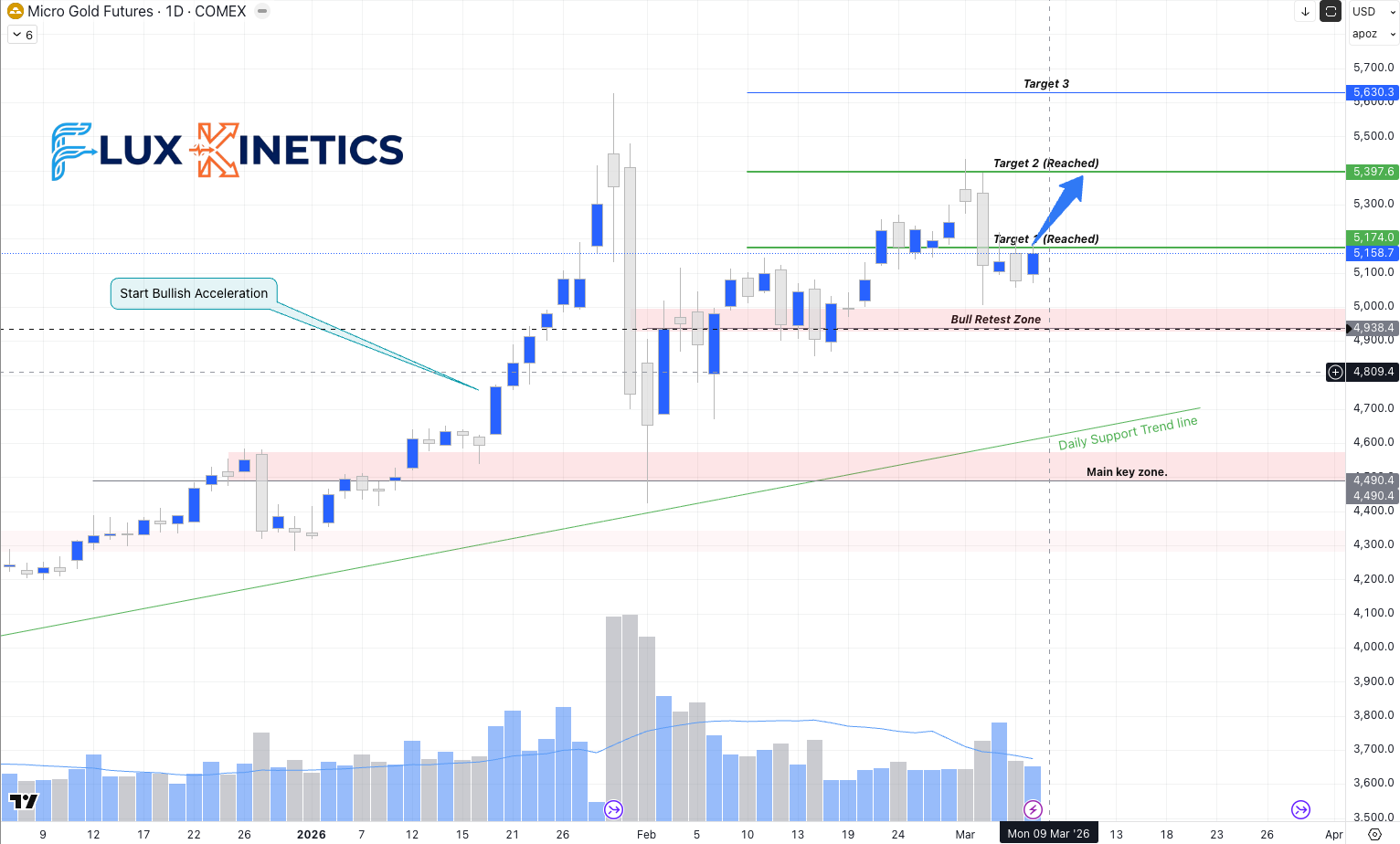

Spot gold traded around 5,114 dollars per ounce on Friday, up on the day after softer payrolls but down on the week, its first loss after a record streak. Silver bounced back into the mid eighties yet still sat below the earlier spike highs after a margin driven flush that had briefly sent it through the triple digit line earlier in the year.

The War Premium Zone on Brent held each intraday pullback and call skew priced in more upside tails, yet the metals complex faded, which tells you that funding costs and dollar strength are now fighting the safe haven bid. The Bull Retest Zone on gold has behaved more like a volatility reset corridor than a breakdown level, with real money demand still anchored in the wide support band carved out by the January melt up.

The driver most coverage missed is that positioning in gold has shifted from pure war hedge to a slow burn stagflation hedge where sticky energy prices meet weakening data. That flips the metals narrative from short term headline insurance to medium term macro defence and keeps upside skew bid even into a red weekly candle.

The Trade: After reaching our Target 2 on 2nd of March, prices has corrected strongly back to Bull Retest Zone which played a perfect support zone. For directional traders, staying long above the Bull Retest Zone keeps the 5,500 area in play while silver needs sustained trade back through the old triple digit zone before any new secular leg higher is credible. The play can be a long trade to enter post daily tested close above Target 1 (5,174$) only, toward Target 2 again first, which is +4% trade.

THE OIL OR GEOPOLITICS STORY

The key print of the week came from US data showing a crude inventory build of around three and a half million barrels alongside a gasoline draw and a small distillate build. Industry data showed an even larger crude build above five and a half million barrels, keeping stocks above last year even as flat price ripped higher.

The Number: 3.5 million barrels. That is a crude build during one of the largest war premiums in years and a Strait of Hormuz effectively shut for normal tanker traffic. Even if Gulf exports are choked for weeks, the market is still structurally long inventory by tens of millions of barrels and trending toward a projected surplus next year, and on top of that Washington is now openly weighing futures market measures, so the pure fear trade that prices permanent scarcity cannot survive that math.

Physical confirmation came from elevated floating storage with large volumes of sanctioned crude parked on tankers and rising inland stocks while Gulf Coast refiners ran hard. Forward spreads blew out into the strongest drift since the last major shock as nearby barrels paid the war premium while the back of the curve still traded a comfortable balance world that surplus forecasts and producer hedging both validate.

PROJECTS, INFRASTRUCTURE, AND POLICY

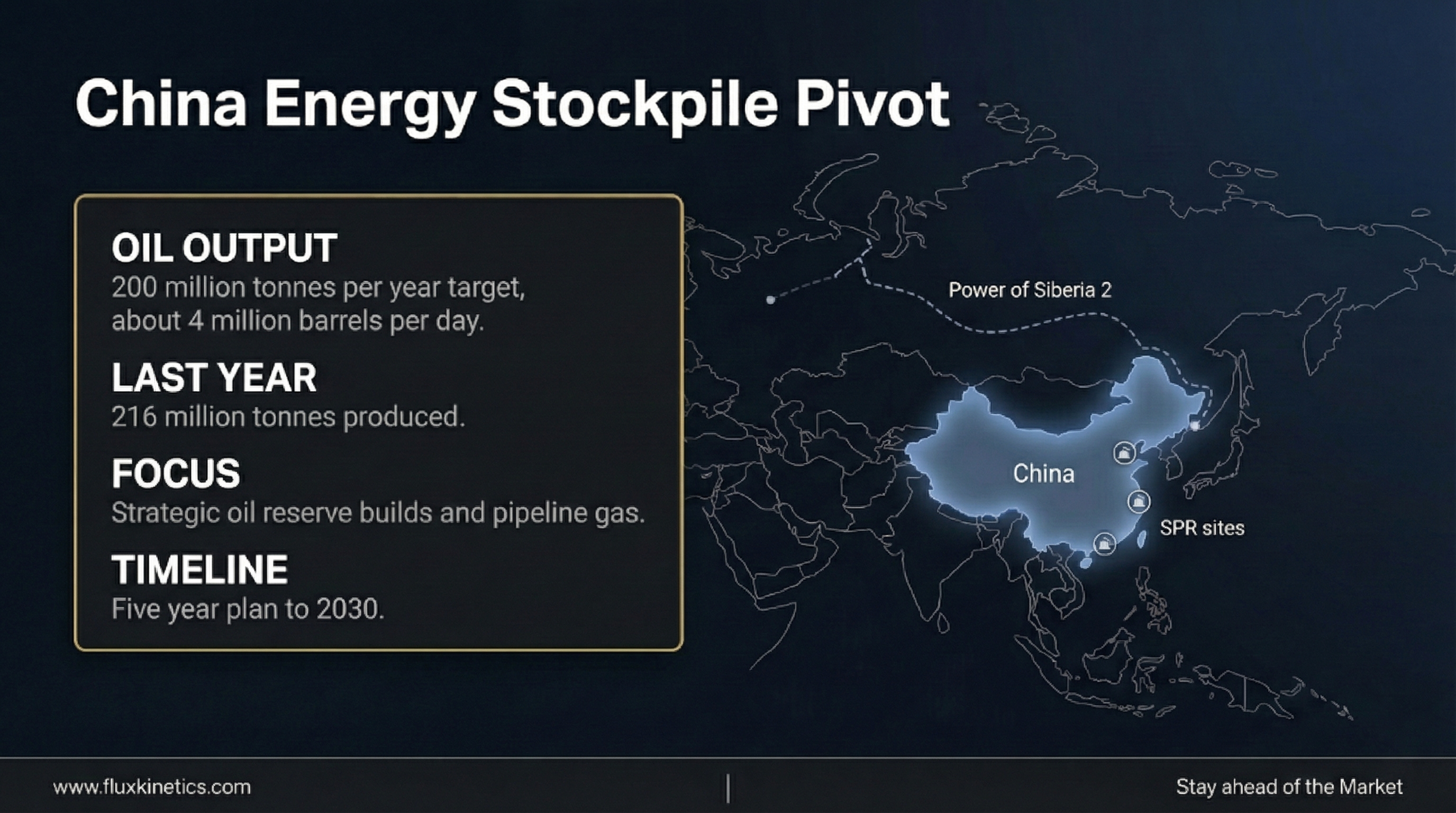

China’s latest five year energy plan set an oil production target around two hundred million tonnes per year, below last year’s record levels, deliberately framing domestic crude as roughly flat while strategic stocks and diversified gas supply do the heavy lifting on security. The blueprint also highlighted more pipeline gas, including preparatory work on the next Siberia corridor, plus expanded coal to gas and coal to liquids projects as a bridge through the decade.

This matters because the largest crude importer is saying that the next barrel of security comes from storage, pipes, and demand management rather than aggressive upstream expansion. It also hardens the surplus narrative at the back of the curve, where non OPEC growth and measured demand combine with a China that prefers to buy and store war discounted cargoes rather than chase new domestic production, which is exactly the world the strip is starting to price.

On the timeline, reserve build and pipeline work play out over years while this week’s Hormuz disruption is an immediate shock, so the policy signal weighs most on 2027 and 2028 pricing rather than the prompt. That locks in a world where front month barrels can trade like a war market while far dated contracts still discount a managed surplus, which is the bifurcation that curve traders live inside.

The Policy Pulse: The strategic angle still underpriced is how China’s commitment to more stockpiling and diversified gas imports shifts the marginal buyer for distressed Gulf cargoes and Atlantic Basin LNG away from Europe and toward Asia in any extended crisis. In volume terms that is worth hundreds of thousands of barrels per day and several billion cubic feet per day of flexible demand that can tighten balances far beyond what top down demand models imply.

Price shouts panic, positioning quietly bets on calm.

If this changed how you see the week, send it one person who needs to see it too.

WEEK AHEAD: WHAT TO WATCH

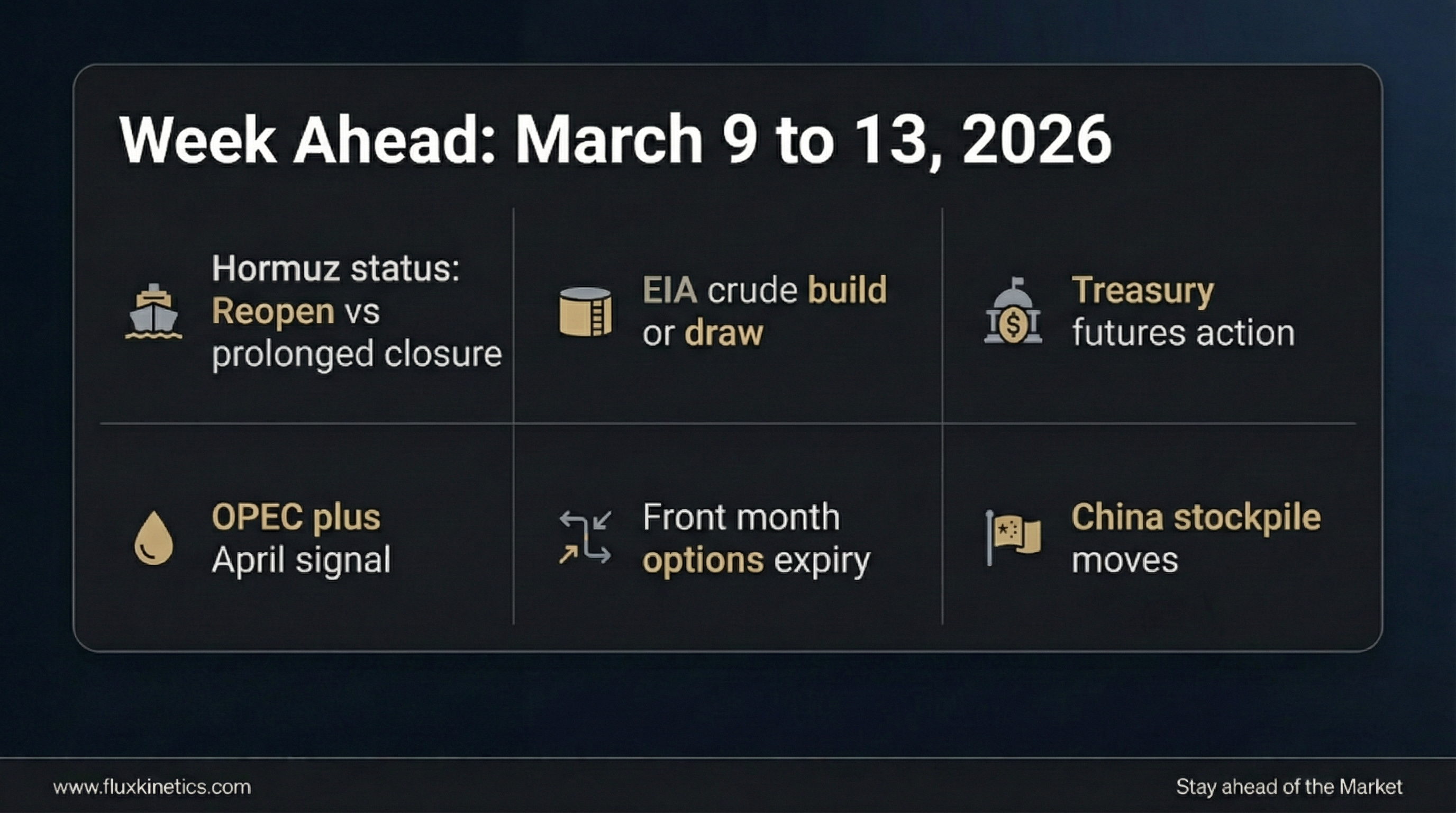

Will naval moves meaningfully reopen Hormuz by mid week and flip Monday’s open from war bid to relief selling in front month spreads.

Does the next EIA crude print follow this week’s build with another increase or a surprise draw, because confirmation caps near dated upside while a draw keeps squeeze dynamics alive.

How OPEC plus formalises its April signal and how quickly physical differentials in Atlantic grades respond once a modest output boost collides with still strong non OPEC growth.

Whether front month Brent and WTI options expiries bleed off the extreme call skew, a volatility crush into expiry would flatten the curve while another upside shock forces a new strip re rating.

Any fresh signals from U S and Chinese policymakers on using or expanding strategic reserves around the 90 dollar zone, because a coordinated draw or accelerated build will reset the balance between prompt and deferred barrels again.

ACTION ITEMS

For traders: Treat 90 to 95 dollars on Brent as the current War Premium Zone defined by this week’s spike and steep six month drift, with intraday failures below that band a signal to fade panic rallies back toward the low eighties while a clean daily close above 95 opens the path to a three figure test at Opening on 9th March. Also, watch carefully the Gold Setup shared above for a swing trade.

For operators: The combination of crude builds, higher refinery runs, and Golden Pass absorbing more gas argues for pulling forward maintenance and procurement on Gulf Coast logistics while freight and capacity are still available. Producers with Gulf exposure should use this window to secure pipe and export slots, recognising that any prolonged Hormuz disruption will keep structural pressure on export infrastructure even if flat price later retreats from the spike.

For investors: The live gap is between surplus projections for next year and a paper market now willing to price a war premium that policymakers are already threatening to lean against, which favours balance sheet strong US producers and LNG infrastructure owners over pure beta names.

Big money is hedging this spike, not marrying it.

In case you’ve missed my previous article about LNG (Liquefied natural gas):

If this briefing helped you think more clearly about the week ahead, send it to the one person on your team or a friend who always asks what actually moved this week and why: That is who Flux Kinetics is written for.

Share this post and bring them into the conversation.

Subscribe to Flux Kinetics and get this briefing every Sunday before the market opens. No noise, no filler, just the signal that energy professionals actually use.

Flux Kinetics - Where energy meets intelligence,

Wassim C.

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.