Oil Falls, Projects Move

Pipelines, rigs, LNG, and storage kept advancing.

Dear Executives, Traders, Investors, and Friends.

Oil had every excuse to fall this week…and it did.

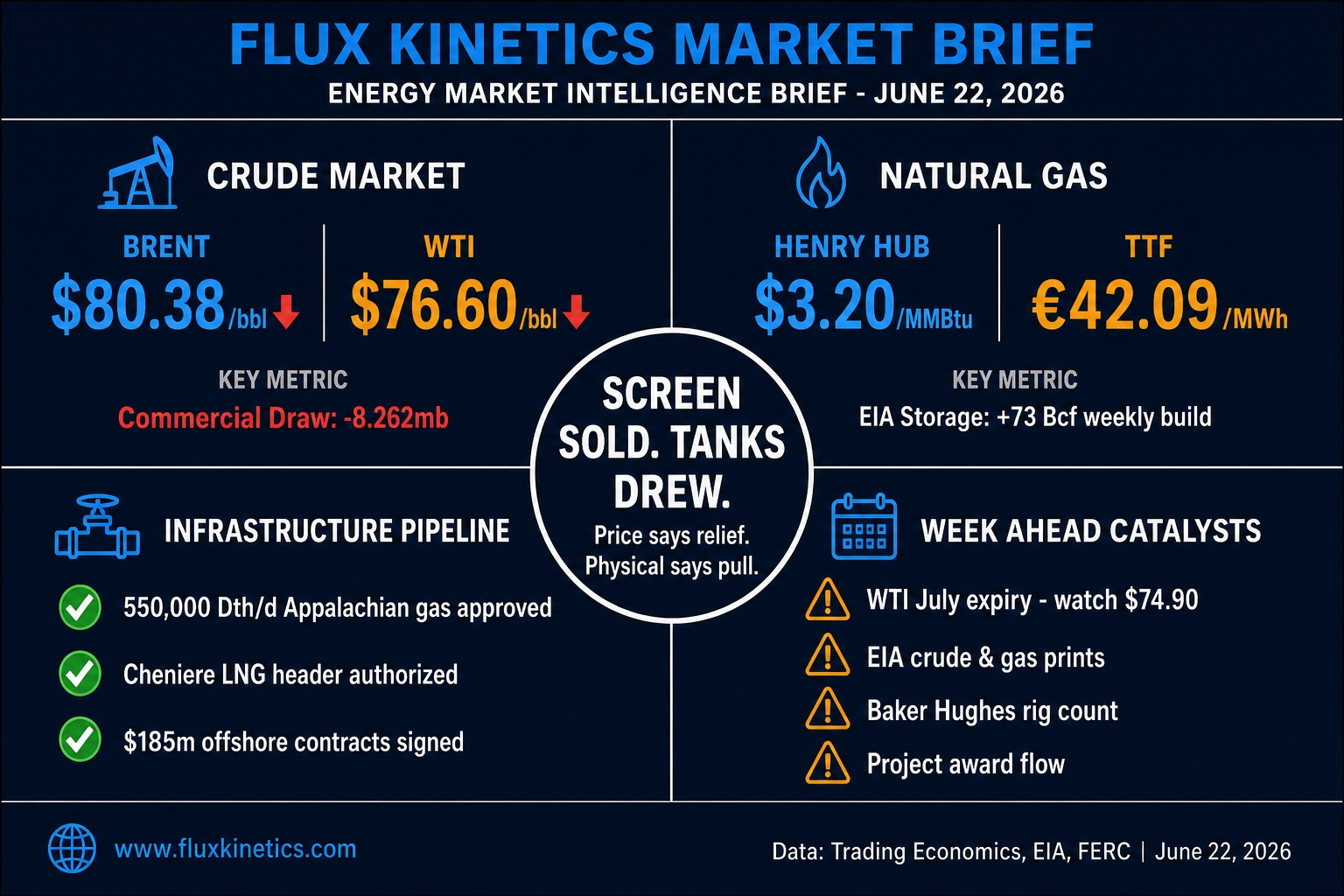

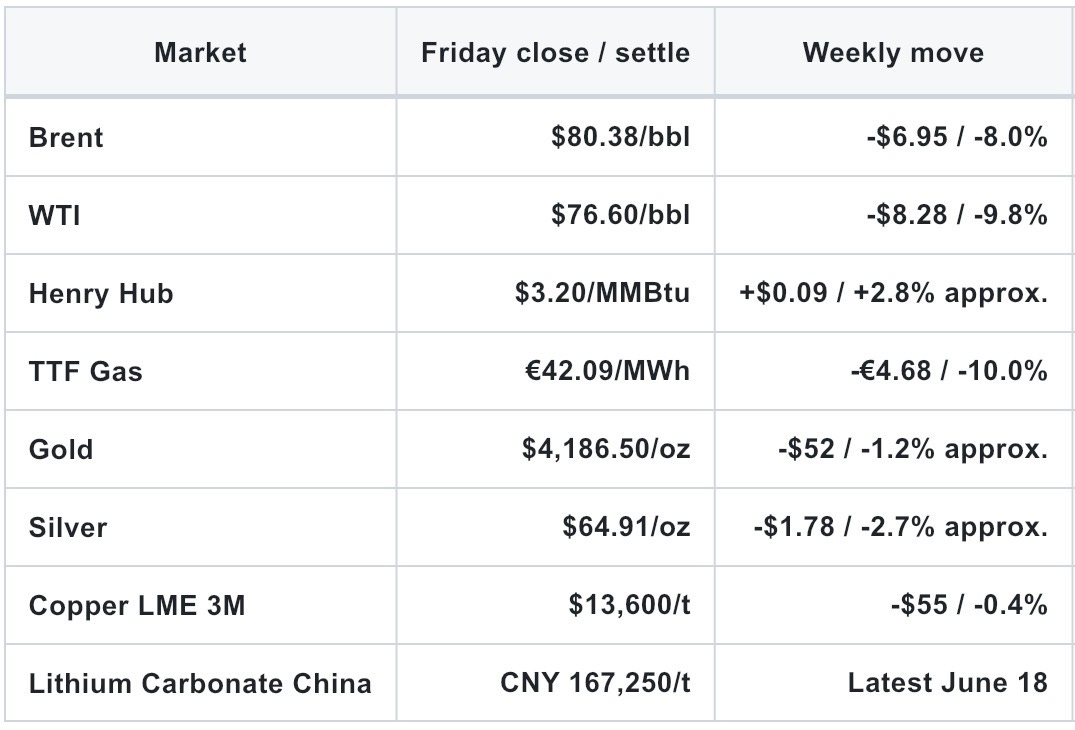

Brent finished near $79.47/bbl. WTI settled at $75.78/bbl.

The screen told one story: risk premium came out, traders cut length and the market moved on.

The tanks were not relaxed, that is not a market drowning in barrels.

That is the week’s gap.

The paper market sold the scare. The physical market kept pulling crud

This Week’s Settle

Brief Contents

Oil tanks beat tape

Refineries stayed hot

Gas pipes moved forward

Project Watch

Metals cooled

Week ahead

THE OIL STORY.

The oil chart looked weak.

The inventory report did not.

U.S. commercial crude stocks fell 8.262mb to 418.222mb. That puts inventories around 6% below the five-year average. Cushing fell to 20.034mb.

Cushing matters. It is not just a storage number. It is where WTI becomes physical.

Imports fell 754kb/d to 5.134mb/d. Exports still ran at 4.327mb/d. Refiners pulled 17.192mb/d of crude into the system, up 230kb/d on the week.

So yes, flat price fell.

But crude still moved.

Gasoline stocks fell 0.906mb. Distillate stocks rose 0.952mb, but distillate remains about 13% below the five-year average. That is still tight enough to matter.

The lazy read was simple: oil sold off.

The Flux Kinetics read: oil sold off while tanks kept draining.

“Paper sold the scare. Tanks kept telling the truth.”

THE NUMBER: 8.262mb.

That crude draw is the number that stops this from being a clean surplus story.

🔁 Found this useful?

Flux Kinetics runs on word of mouth. If this note sharpened how you see the week, one forward to the right person is worth more than any algorithm. 📨

THE REFINING STORY.

The refineries did the talking this week.

U.S. refinery utilization hit 96.7%. That is high. Actually, Very high.

When refineries run that hard, they are not guessing. They are pulling crude because margins, product demand, and logistics tell them to keep heat in the units.

Gasoline output averaged 10.1mb/d. Distillate output averaged 5.2mb/d.

Finished gasoline supplied rose to 9.212mb/d, up 481kb/d from the prior week. Jet fuel supplied rose 413kb/d to 2.081mb/d.

That is why the crude draw matters.

A trader can sell a futures contract in one click. A refinery cannot rewrite its crude slate in five minutes. Once the system is running hot, the barrels have to come from somewhere.

Demand was not dead.

It was uneven.

THE FLUX KINETICS CRACK: If U.S. refinery utilization stays above 95%, crude still has support. If runs fall below that level, crude can back up into tanks quickly.

THE GAS STORY.

Gas was quieter.

Not irrelevant.

EIA reported a 73 Bcf storage build. Working gas reached 2,759 Bcf. Stocks sit 151 Bcf above the five-year average and 29 Bcf below last year.

That is balanced. Not tight enough to chase. Not loose enough to ignore.

The better signal came from pipe.

At its June 18 meeting, FERC issued a certificate for Eastern Gas Transmission and Storage’s Appalachian Reliability Project. The project is designed to move about 550,000 dekatherms per day of firm gas service through Pennsylvania and Ohio.

FERC also authorized Cheniere Creole Trail Pipeline’s Gillis Header Project and kept key approvals alive for Transco’s Southeast Supply Enhancement Project.

That matters.

Not because gas flows tomorrow. It does not.

It matters because this is how the physical market fixes a bottleneck. Not with a headline. With pipe, steel, crews, permits, compression, and time.

THE INSIDER VIEW: The paper market prices relief early. The physical market only feels it when the pipe is full.

PROJECT WATCH.

This is where I spent extra time this week.

Price is one thing. Projects are another. When companies sign contracts, bid work, approve pipe, or move rigs, that is where the market shows what it believes with real money

1. Eastern Gas Appalachian Reliability Project

FERC issued a certificate on June 18 for Eastern Gas to build and operate the Appalachian Reliability Project.

The project is designed for about 550,000 Dth/d of firm gas transport.

That is not a small number. It gives Appalachian gas another path to market. It also tells us something simple: gas demand is still looking for reliable pipe.

2. Cheniere Creole Trail Gillis Header Project

FERC authorized Cheniere Creole Trail Pipeline to build and operate the Gillis Header Project.

Headers do not get much attention outside the gas world. They should.

They are the plumbing behind LNG growth. If liquefaction plants are the mouth, headers are the throat. Without them, the gas does not get where it needs to go.

Small project. Big signal.

3. Transco Southeast Supply Enhancement

FERC also sustained key approvals tied to Transco’s Southeast Supply Enhancement Project.

That keeps another gas path alive into a market where LNG demand, power demand, and industrial demand are all competing for the same molecules.

This is the quiet part of the gas trade.

Demand growth is loud. Pipe work is slow.

4. Transocean adds $185m of rig backlog

Transocean announced $185m of new contract backlog on June 16.

The Transocean Norge won a five-well contract with Harbour Energy in Norway. Around 300 days of work. Start expected in Q1 2028.

The Transocean Equinox won a two-well contract with Santos in Australia. Around 90 days of work. Start expected in Q2 2027.

This is not a spot trade.

This is offshore work being booked years forward. That tells you operators still want high-end rigs for hard barrels.

5. ADNOC Waset gas project bids under review

Upstream reported that ADNOC is reviewing commercial bids for the Waset gas project EPC contract.

The project has been reported at up to 180 MMcf/d of potential gas output.

This is still bidding. Not award.

Bidding matters… Contractors do not waste time on dead projects. If the big EPC names are sharpening pencils, the project has definitely a pulse.

6. Johan Sverdrup Phase 4 being studied

June 15, Johan Sverdrup partners are looking at a possible Phase 4 extension after appraisal wells showed early estimates of 20 to 30 million boe.

That is not huge compared with Johan Sverdrup’s base.

Operators love these kind of Barrels : Nearby, known system, existing infrastructure and lower risk.

The best barrel is often the one you can tie back to kit already in the water.

7. Barber Springs pumped storage gets a path

FERC issued a preliminary permit for Kinetic Energy Storage’s 500 MW Barber Springs Pumped Storage Project in New Mexico.

This is not oil and gas.

It belongs in the energy map. Pumped storage is a battery made of water and gravity. As power demand rises, the grid needs storage that lasts longer than a short battery cycle.

This is where the energy story keeps moving.

Fuel gets the headline. The grid decides what works.

“Projects are where the market stops talking and starts spending.”

THE METALS STORY.

Metals cooled this week.

Gold slipped toward $4,186.50/oz. Silver fell to around $64.91/oz. Copper held better at $13,600/t on LME 3M.

Lithium also pulled back. China battery-grade lithium carbonate fell to CNY 167,250/t on June 18.

The market is still trying to separate real demand from restocking.

Those are not the same thing.

Restocking fills warehouses. A shortage empties them.

THE FLUX KINETICS TRADE:

Similarly to last week, the setup is still the same. I miss this Friday entry at $4,150 and will wait for next one:

Potential long entry would be a second pullback to $4,100 which will hold. Stop Loss below $3,940. Take Profit can be targeted as a first level: $4,300, then $4,500.

Patience over chasing

📬 Never miss a signal

If this is your first time reading Flux Kinetics, every weekly note lands free in your inbox. No noise, no filler, just what actually moved the tape.

Week Ahead: What to Watch

Monday, June 22 : PMI day

Watch the U.S. and global flash PMI numbers. If business activity looks weak, oil and copper may feel pressure. If services and factories hold up, it supports demand.

Thursday, June 25 : PCE inflation + gas storage

PCE is important because it shapes Fed expectations, the dollar, gold, silver, and copper. EIA gas storage will also matter for Henry Hub. A smaller gas build supports prices. A bigger build pressures gas.

The Close

Oil stocks fell, refineries stayed busy, and new gas and power work kept moving.

Watch what is being used, built, moved, and stored.

That is where the market usually tells the truth first.

⚡ One last thing

If this changed how you see the week, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm.

📨 Share • 📬 Subscribe • 💬 Leave a comment

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.