Japan-US Just Rewired the Global Energy Map

The deal that breaks China's critical minerals grip

In case you’ve missed my previous article about this week summary

The trade deal everyone’s talking about isn’t just numbers on paper. It’s a strategic realignment that shifts how global energy flows for the next decade.

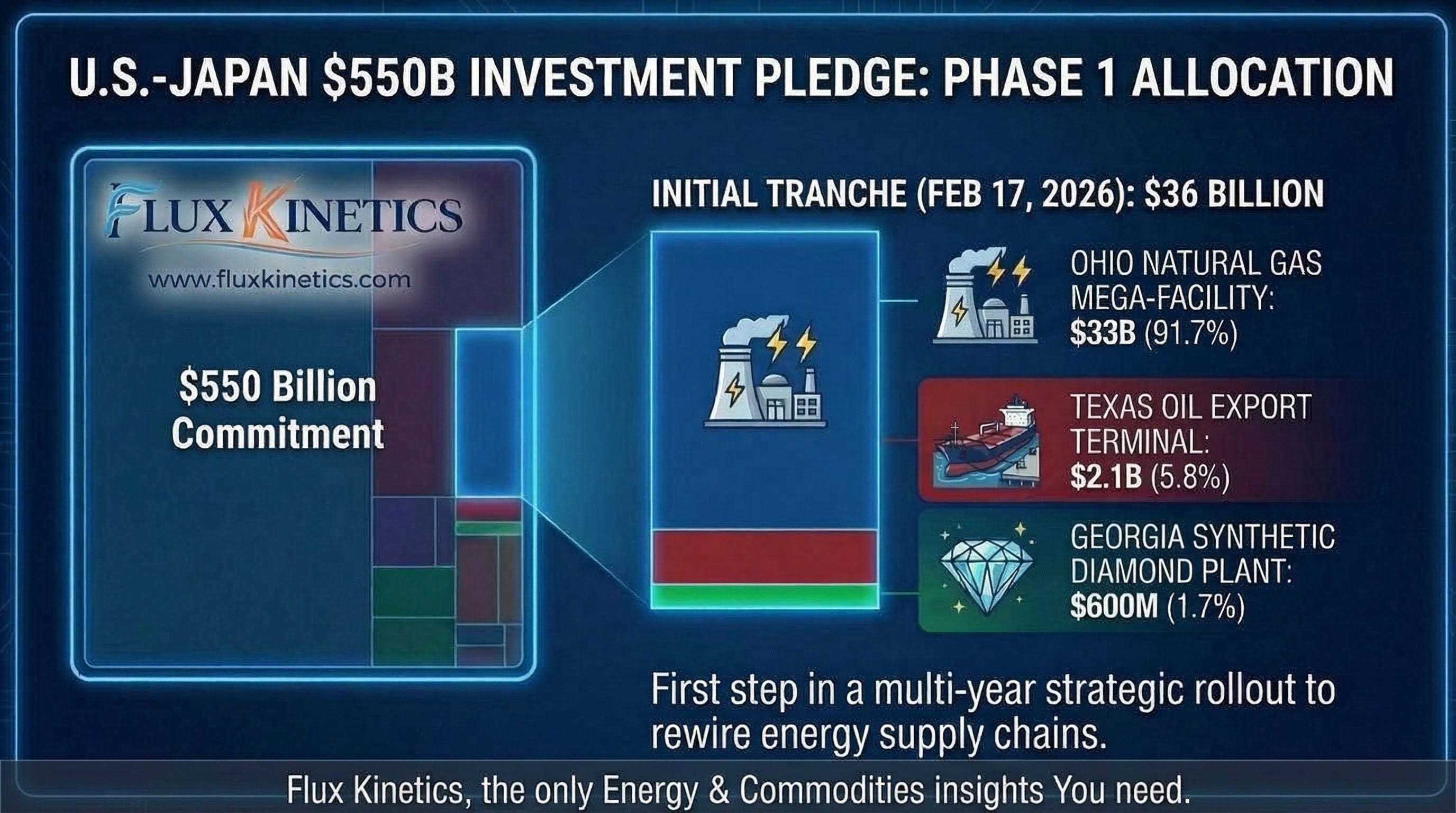

On February 17, 2026, Japan green light the first $36 billion tranche of its $550 billion U.S. investment pledge. Three projects dropped: a $33 billion natural gas mega-facility in Ohio, a $2.1 billion deepwater oil export terminal in Texas, and a $600 million synthetic diamond plant in Georgia. These aren’t vanity projects. They’re calculated moves that challenge China’s commodity grip while locking in U.S.-Japan energy interdependence.

Here’s what most coverage misses: this isn’t about energy alone. It’s about supply chain sovereignty in a world where China controls 98.7% of gallium production, 95% of magnesium, and 82.7% of tungsten. Japan’s betting big that partnering with the U.S. on critical minerals beats relying on Beijing, especially after China slapped rare earth export bans on Tokyo following Prime Minister Takaichi’s Taiwan comments in late 2025.

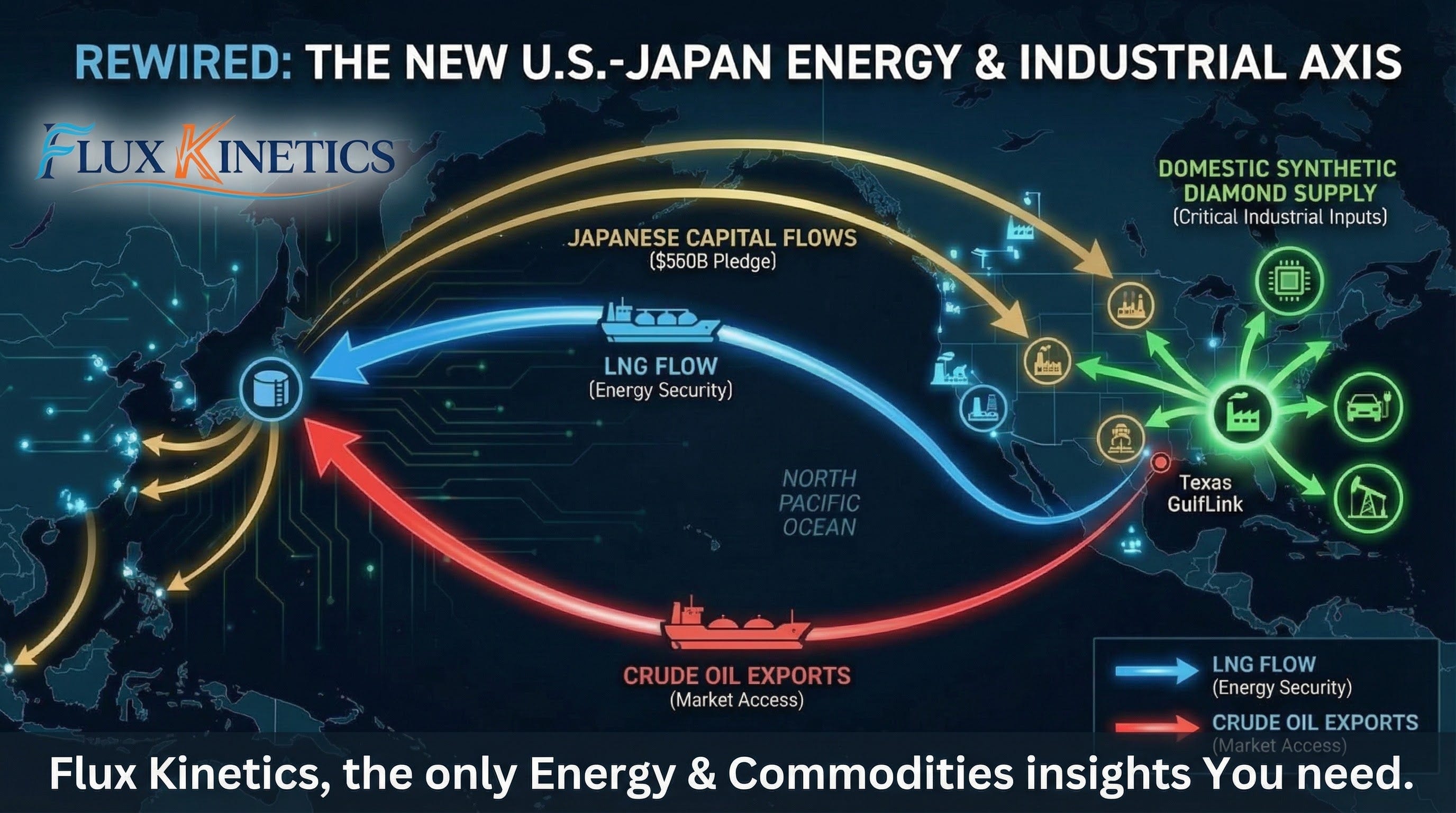

The numbers tell the real story. That Portsmouth, Ohio facility will pump 9.2 gigawatts of natural gas power, enough to supply 7.4 million homes. That’s not just the largest gas plant in U.S. history. It’s baseload power for AI data centers at a time when electricity demand is spiking faster than infrastructure can keep up.

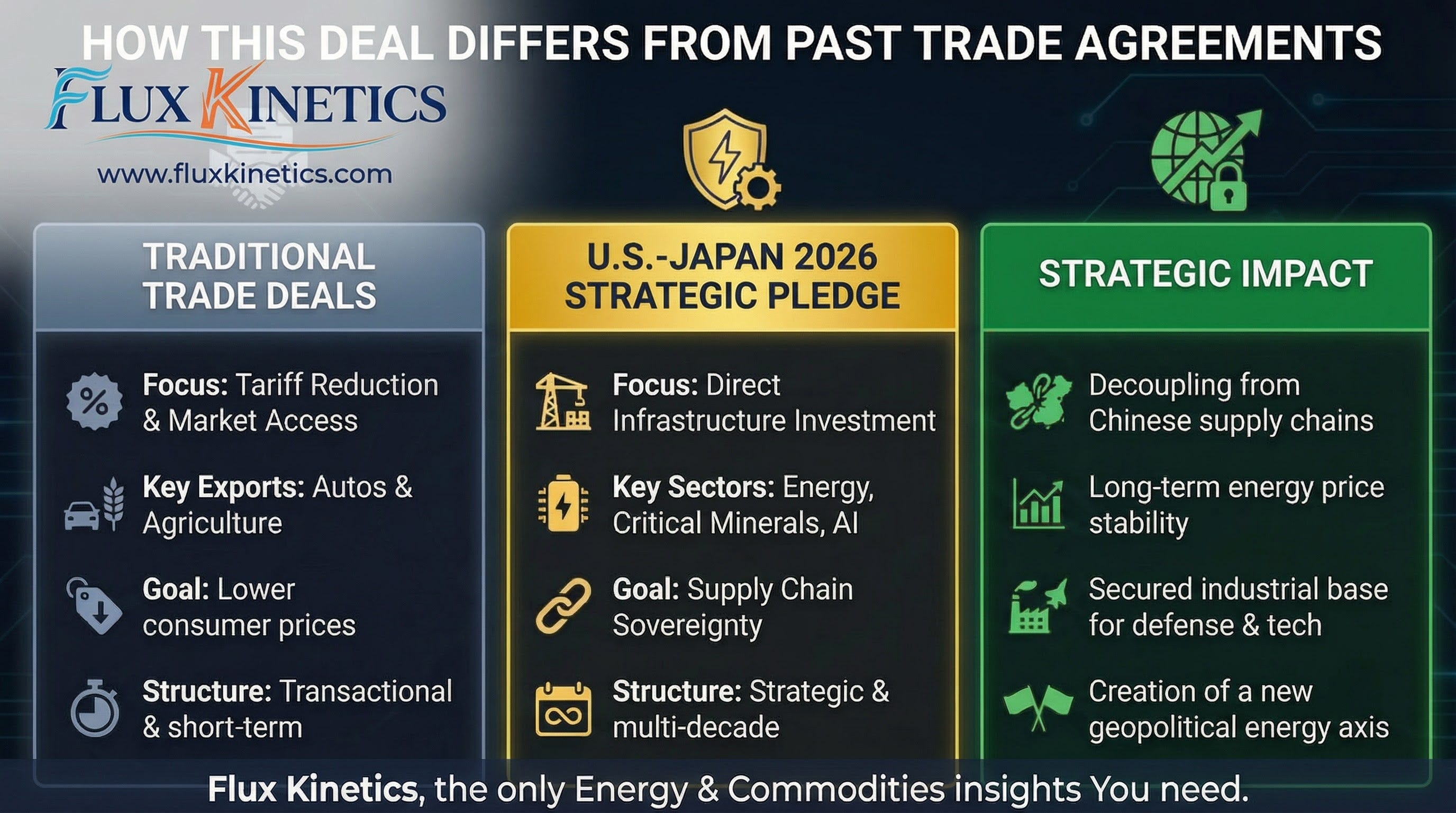

Why This Deal Matters More Than Previous Agreements

Past trade agreements focused on tariff cuts and auto exports. This one weaponizes investment to reshape energy security.

Japan’s getting tariff relief (down to 15% from 25% on key exports). The U.S. is getting foreign capital to build domestic energy infrastructure without federal spending. And both countries are building a firewall against China’s critical minerals monopoly.

Look at the Texas GulfLink project. It’s a deepwater crude export terminal that will generate $20-30 billion annually in U.S. oil exports once it hits full capacity. Over 20 years, that’s $400-600 billion in export value. Sentinel Midstream is developing it with Japanese financing, Japanese logistics partners (Mitsui O.S.K. Lines), and Japanese steel suppliers (Nippon Steel). This isn’t aid. It’s integrated supply chain design.

The Georgia synthetic diamond facility is even more strategic. Diamond grit is critical for semiconductor manufacturing, automotive production, and oil & gas drilling tools. Right now, the U.S. sources most of it from China. Element Six’s new plant will satisfy 100% of U.S. demand domestically. That matters when geopolitical tensions can cut off supply overnight.

Japan’s also hedging against China’s economic coercion playbook. After Beijing restricted rare earth exports to Tokyo in January 2026 over Taiwan tensions, Tokyo accelerated this U.S. partnership. The message is clear: diversify supply chains before they become leverage points.

For energy investors and commodity traders, this creates immediate opportunities. Natural gas demand in the Midwest just got a $33 billion backstop. U.S. crude export capacity is expanding with guaranteed Japanese investment. And domestic synthetic diamond production is about to eliminate China’s pricing power in a critical industrial input.

What Energy Professionals Need to Watch

Three things will determine whether this deal delivers on its promise:

Execution timelines. These are multi-year megaprojects. The Ohio gas plant alone is the largest in U.S. history. Permitting, construction delays, and supply chain constraints could push completion dates and inflate costs.

Profit-sharing structure. Japan’s investment comes with strings. Under the earlier agreement framework, profits split 50-50 until Japan recoups initial costs, then shift to 90-10 in favor of the U.S. That’s attractive long-term, but Japan’s essentially providing patient capital with deferred returns.

China’s response. Beijing won’t sit idle while the U.S. and Japan build alternative supply chains. Expect accelerated Chinese investment in rare earth processing in friendly countries, price wars on critical minerals, and potential export restrictions on more elements.

The broader implication: we’re watching the formation of a U.S.-Japan energy axis designed to counter China’s commodity dominance. This isn’t just about oil and gas. It’s about semiconductors, EV batteries, defense manufacturing, and AI infrastructure. All of it depends on critical minerals that China currently controls.

Done-For-You Action Plan

If you’re tracking energy markets or investing in commodities, here’s what to do:

Monitor Midwestern natural gas pricing. The Ohio project will create sustained demand. Henry Hub spreads to regional hubs could tighten as construction ramps up.

Track U.S. crude export capacity expansion. Texas GulfLink adds significant deepwater export capability. This changes Brent-WTI arbitrage dynamics and gives U.S. producers better access to Asian premium markets.

Watch synthetic diamond pricing. As U.S. domestic production scales, industrial diamond prices could decouple from Chinese supply constraints. This impacts tooling costs for oil & gas operators.

Follow Japan’s next investment announcements. Trade Minister Akazawa confirmed more deals are coming before PM Takaichi’s March 2026 U.S. visit. Expect additional LNG projects, rare earth processing facilities, and possibly battery manufacturing.

Assess your supply chain exposure to China. If your business relies on Chinese rare earths, synthetic diamonds, or other critical minerals, this deal signals a long-term shift. Consider dual-sourcing strategies now before supply gets tight.

This is the beginning, not the end. Japan committed $550 billion. We’ve seen $36 billion announced. The next $514 billion will determine whether this becomes a true alternative to China’s supply chain dominance or just expensive infrastructure with geopolitical optics.

Want deeper analysis on how geopolitical deals reshape Energy and Commodity markets?

Subscribe now to get exclusive insights before they move markets. And if you found this breakdown useful, Share it with your network and energy professionals need to understand what’s actually happening, not just what’s being announced.

What’s your take? Are you positioning for U.S.-Japan energy integration or staying diversified across China exposure? Let me know in the comments.

Join the Flux Kinetics community and be the first to know. I send every week, intels and Energy-Commodities market analysis.

Flux Kinetics - Where energy meets intelligence,

Wassim C.

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

Interesting article Wassim, it’s will be a game changer to see how the other 500B$ from Japan will be spent with US…

A sharp, well-argued breakdown that shows this deal is less about energy projects and more about long-term supply-chain power and geopolitical leverage