From Barrel To Power Bill

How shipping costs travel through diesel, freight, industry, and the grid

Dear Executives, Traders, Investors, and friends

Most people read energy prices from the wrong end of the chain.

They see gasoline.

They see electricity bills.

They see inflation headlines.

By the time those show up, the signal is already old.

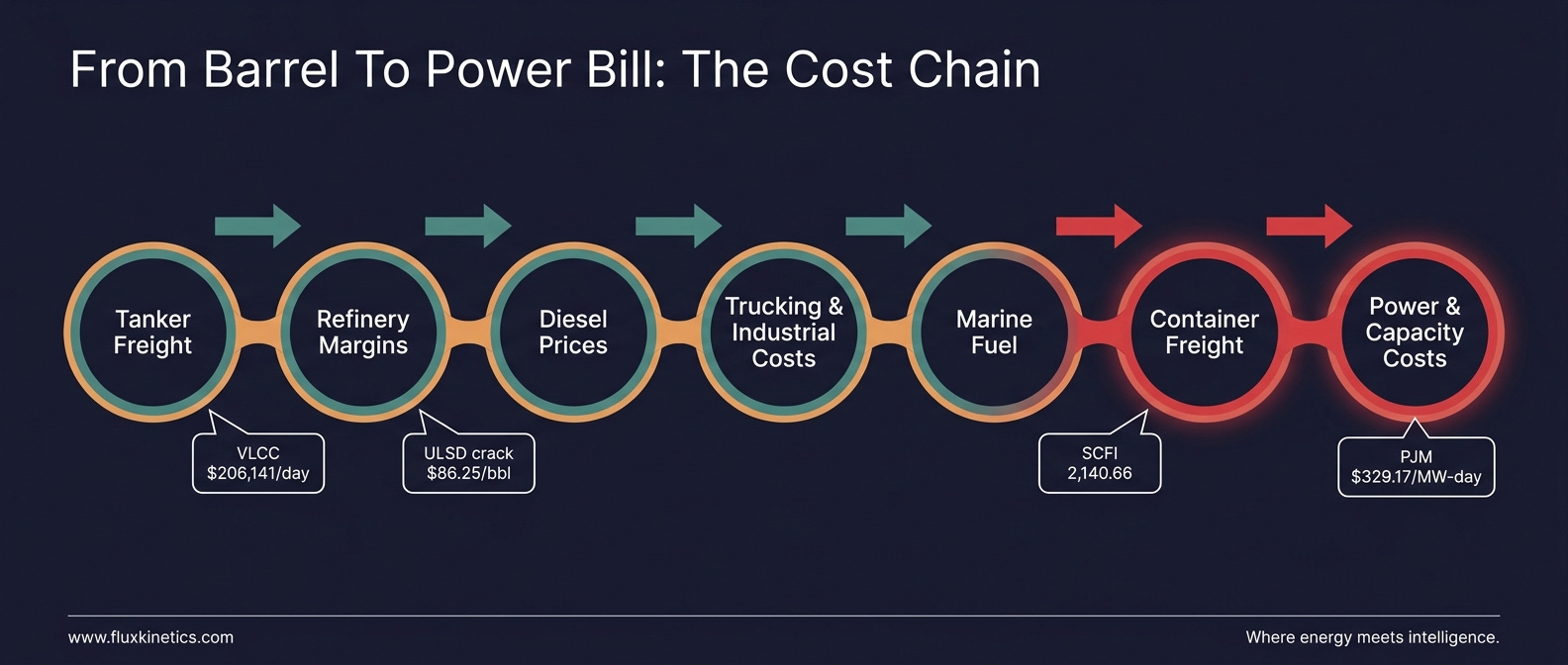

Energy cost pressure usually starts earlier, in the physical system: ships, terminals, refineries, diesel inventories, freight contracts, transformers, and capacity markets. The screen price is only the last translation.

That is the lesson here.

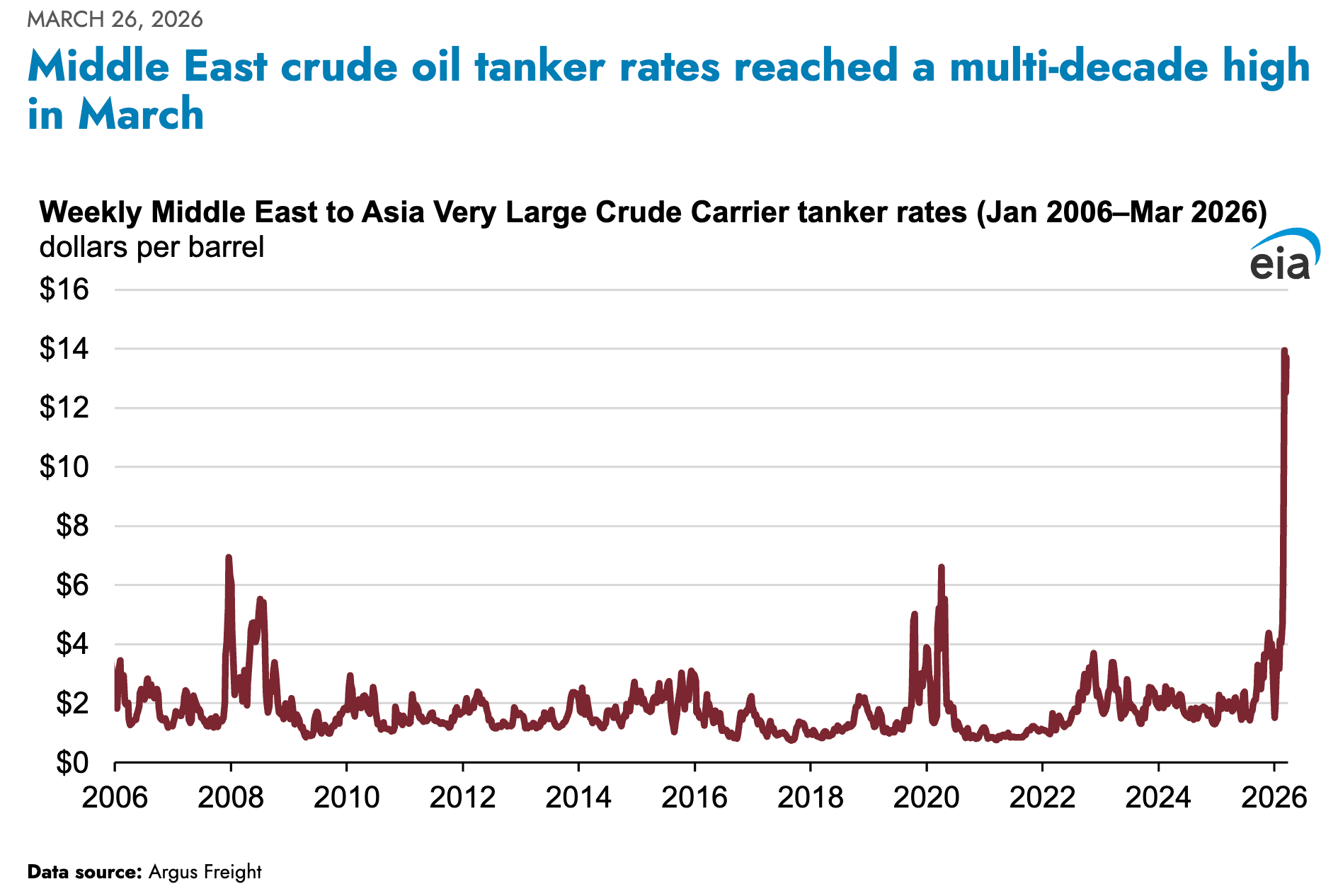

The cost of hiring a very large crude carrier, or VLCC, on a key long-haul crude route reached W218.52, equal to about $206,141 per day. That was nearly four times higher than at the start of the year…

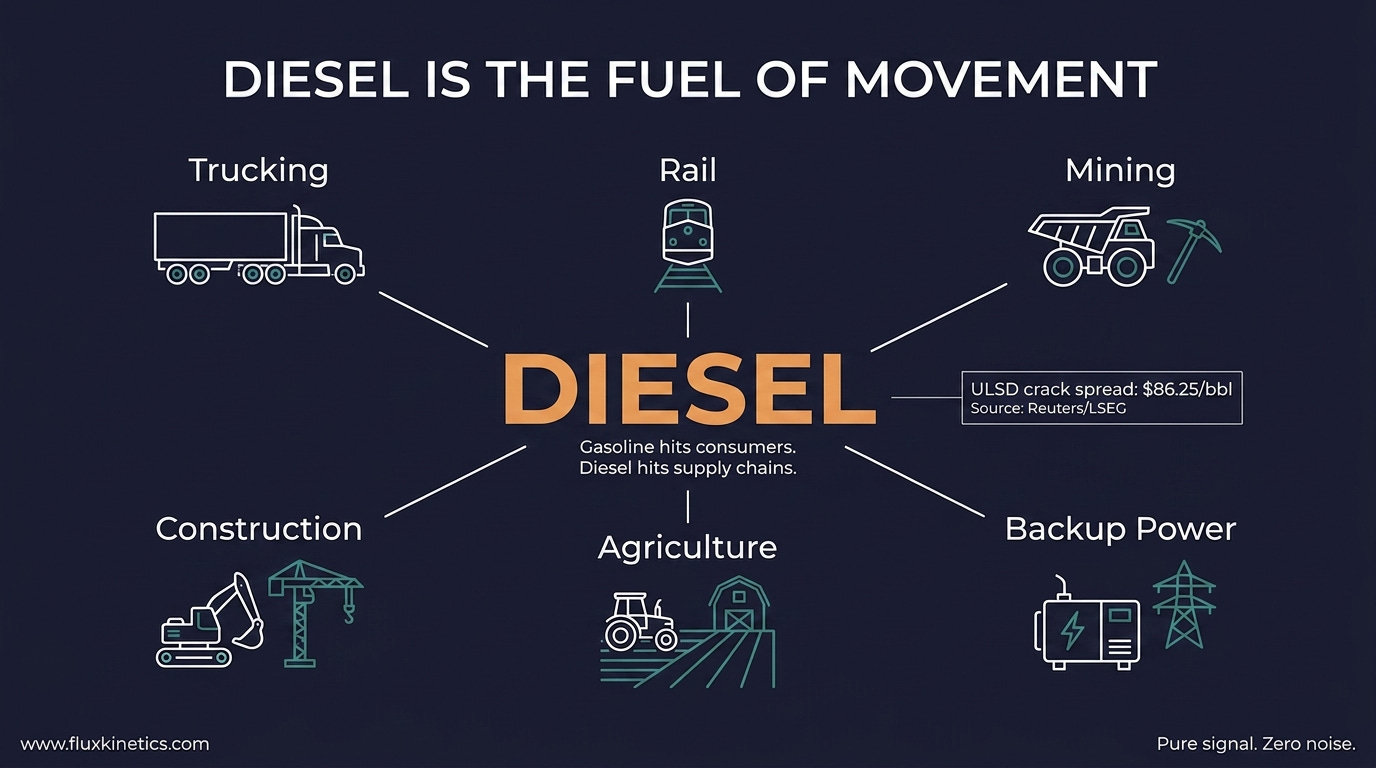

A few weeks later, diesel was sending the same message. The ultra-low-sulfur diesel crack spread hit a record $86.25 per barrel, up 105%. Gasoline cracks also rose, reaching $37.62 per barrel…

For a beginner, a crack spread is simple. It is the rough margin refiners earn when they turn crude into products like diesel, gasoline, and jet fuel.

When cracks rise, refiners usually make more money.. which comes from somewhere.

It comes from the buyer of the refined product !

That buyer may be a trucking fleet, mining company, railway, construction contractor, farmer, shipping line, utility, or data centers operator.

Refiners feel the benefit first and the physical economy feels the cost later.

That delay is where the market often misses the story.

What this piece covers:

Oil does not move itself

Refiners get paid first

Diesel is the industrial fuel

The container leg comes next

The grid is the slowest link

Oil does not move itself

A barrel sitting at an export terminal is not useful to a refinery until it arrives.

That means freight matters.

Think of buying a machine part. The part may cost $1,000. If transport costs $100, your landed cost is $1,100. But if transport jumps to $400, the same part now costs you $1,400 delivered.

Oil works the same way.

A higher tanker rate does not always show up as a clean headline in crude prices. Sometimes it appears inside delivered crude differentials. Sometimes inside refinery margins. Sometimes inside product cracks. Sometimes inside working capital.

This is why physical markets are different from financial markets.

Financial markets can reprice in seconds, traders can change their mind and act fast in front of there screen…

Physical markets move at the speed of ships, storage tanks, refinery runs, truck fleets, and contract resets.

That is slower… it is also more powerful.

🔁 Found this useful?

Flux Kinetics runs on word of mouth. If this note sharpened how you see the week, one forward to the right person is worth more than any algorithm.📨

Refiners get paid first

The first obvious winner from a product squeeze is the refiner.

Refiners buy crude and sell usable fuels. If diesel and gasoline rise faster than crude, refinery margins expand. That is why the refiner trade was easy to see.

Major U.S. refiners including Valero, Phillips 66, and Marathon Petroleum were up more than 20% year-to-date as investors priced stronger margins.

That is the visible trade.

Refiner’s margin is not free money. It is a cost transferred downstream.

If refiners earn more per barrel of diesel, someone else pays more per barrel of diesel. That is not a moral statement. It is just the chain.

The equity market usually prices the refiner benefit quickly. It prices the downstream cost slowly.

That is where the opportunity, and the risk, usually sits.

Diesel is the industrial fuel

Gasoline is mostly a consumer fuel.

Diesel is different.

Diesel powers or supports trucks, rail, mining equipment, construction machinery, agricultural equipment, backup generators, emergency systems, marine fuel markets, and remote operations.

That makes diesel one of the cleanest signals for the physical economy.

When gasoline rises, households feel it at the pump.

When diesel rises, the whole supply chain feels it through freight, production, and reliability costs.

A high diesel crack is not only a refinery margin story. It is also an industrial cost warning… Diesel is the fuel of movement.

When movement gets expensive, everything in the downstream gets tested.

The container leg comes next

Now move from oil tankers to container ships.

Container ships carry finished goods: electronics, appliances, furniture, machinery, parts, clothing, and industrial components. Those ships also burn fuel.

Precision matters here. Marine gasoil is directly linked to distillates like diesel. Very low sulfur fuel oil, or VLSFO, is not the same as diesel. It is usually a blended marine fuel. But when low sulfur blending components get tight, VLSFO can also move higher with a lag.

Shipping companies do not absorb that forever. Fuel costs move into freight rates through contract resets, bunker adjustment factors, and surcharges.

The Shanghai Containerized Freight Index reached 2,140.66 in mid-May, up 13.47% over the trailing month.

That was not a 2021-style freight explosion but it was a warning light.

Importers usually feel it later: Contracts reset, inventory turns, freight invoices roll through cost of goods sold. Then the margin hit appears.

The cost moves before the earnings call explains it.

📬 Never miss a signal

If this is your first time reading Flux Kinetics, every weekly note lands free in your inbox. No noise, no filler, just what actually moved the tape.

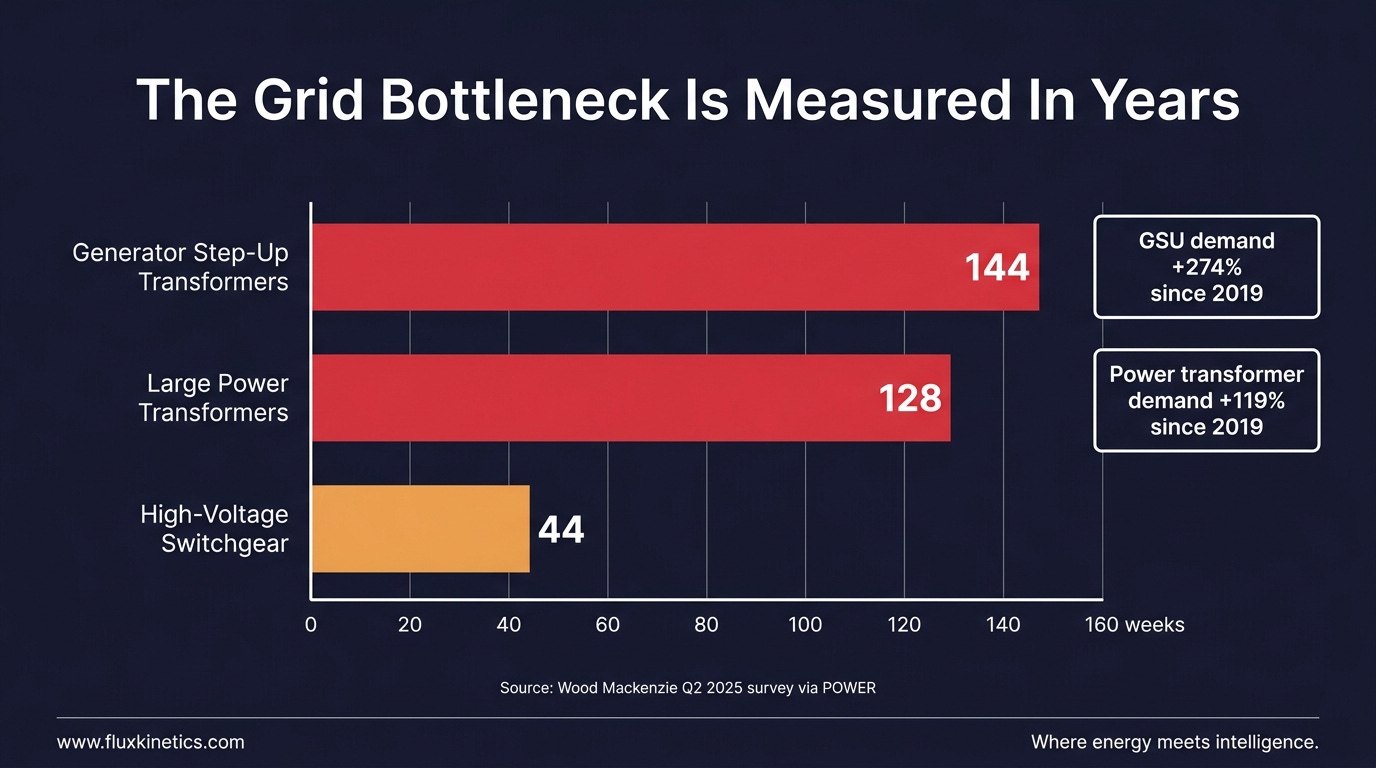

The grid is the slowest link

The power grid does not run mainly on diesel. That is not the point.

The point is that power systems are already tight, and tight systems are expensive to manage.

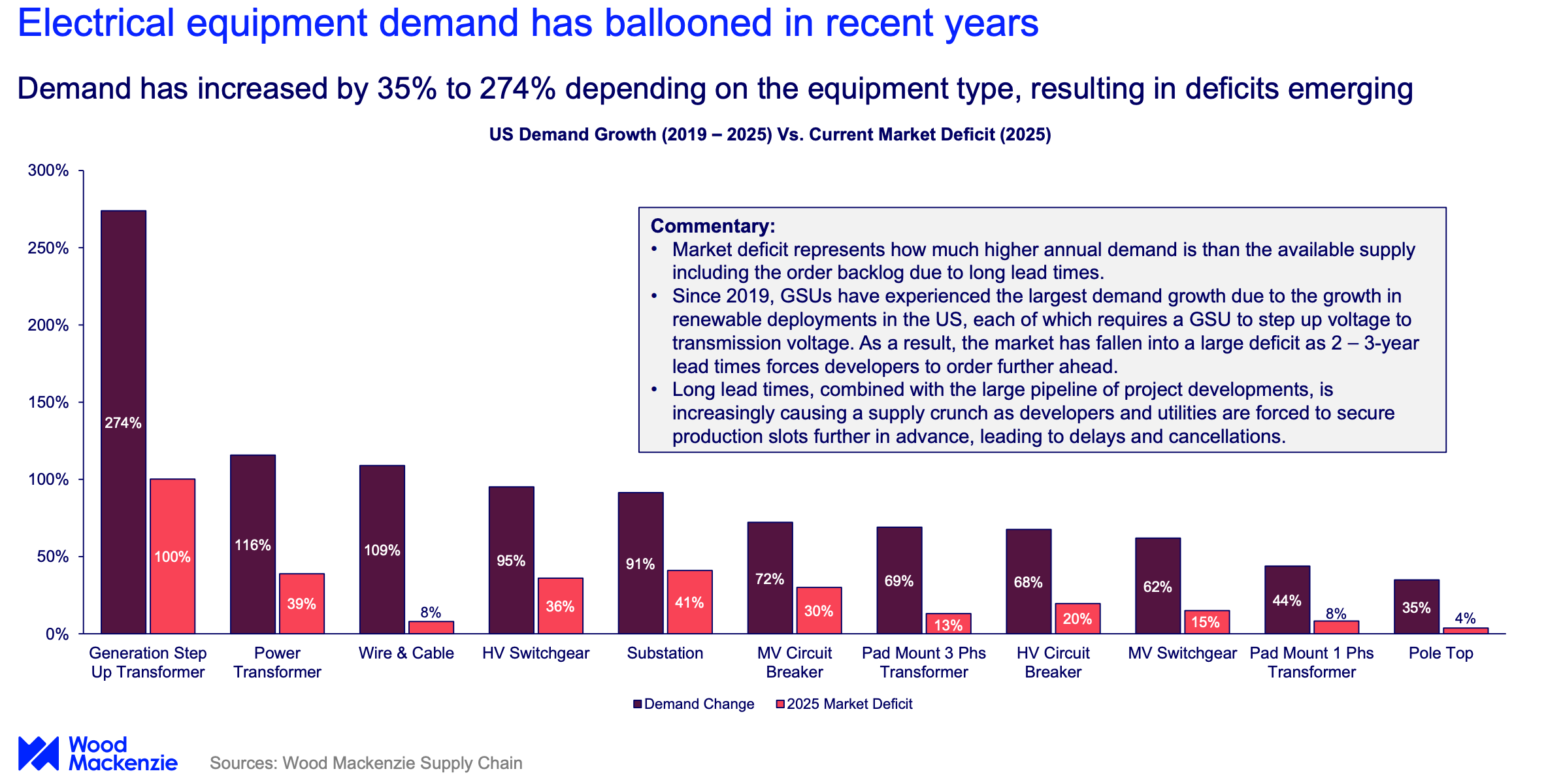

The grid is dealing currently with major data-center growth, industrial electrification, aging infrastructure, delayed generation projects, and long equipment lead times.

The biggest bottleneck is often not fuel. It is equipment.

A transformer allows electricity to move safely between voltage levels. Without transformers, large new loads, substations, power plants, and renewable projects cannot connect on schedule.

Average lead times of roughly 144 weeks for generator step-up transformers, 128 weeks for large power transformers, and 44 weeks for high-voltage switchgear.

That is not a minor delay. That is two and a half to three years for critical equipment.

generator step-up transformer demand up 274% since 2019, and power transformer demand up about 119%.

If a data centers or industrial project cannot get grid equipment on time, it has only a few options: wait, move, pay more, build behind-the-meter power, or rely more heavily on backup systems.

None of those options are cheap.

Final takeaway

Energy inflation does not always start at the gas pump.

Sometimes it starts with the cost of moving a barrel. Then it moves into refinery margins, diesel prices, shipping costs, industrial expenses, power-market capacity prices, and eventually the bills paid by businesses and households.

The market usually prices the first step.

It is slower to price the second, third, and fourth.

That is why the chain matters.

Where does the barrel move?

Who pays to move it?

Who refines it?

Who burns the product?

Who absorbs the cost?

Who can pass it through?

Who cannot?

That is where the signal is, the one most energy investor models ignore. That is your edge now.

⚡ One last thing

If this changed how you see the week, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm.

📨 Share • 📬 Subscribe • 💬 Leave a comment

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

Thanks for reading Flux Kinetics

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

This is exactly the kind of thinking that gets overlooked because most people only see the monthly power bill, not the entire system behind it.

What I found most interesting is that waste is often only waste because nobody has figured out how to create value from it yet.

Throughout my career, whether developing products, building companies, or creating new business models, the opportunities were rarely hiding in plain sight. They were usually buried inside inefficiencies everyone else accepted as normal.

The idea of turning byproducts into energy is bigger than energy. It is a mindset.

Look at any industry and ask one question:

"What are we throwing away that still has value?"

Sometimes it's materials.

Sometimes it's data.

Sometimes it's time.

Sometimes it's human potential.

The people who ask that question consistently are often the ones who create the next generation of innovation.

As we continue to search for cleaner, more efficient ways to power our future, I believe the winners will be those who learn how to extract value from what others dismiss.

Great article, Jay. It is a reminder that innovation is not always about inventing something new. Sometimes it is about seeing value where everyone else sees a cost.

The article explores how energy can be generated from waste streams and overlooked resources, challenging conventional assumptions about where value originates in our energy infrastructure. It highlights the broader principle that inefficiencies and byproducts can become assets when viewed through the lens of innovation and systems thinking.