First LNG Export. Brent Still Ran. TLM.

What you need to know this week.

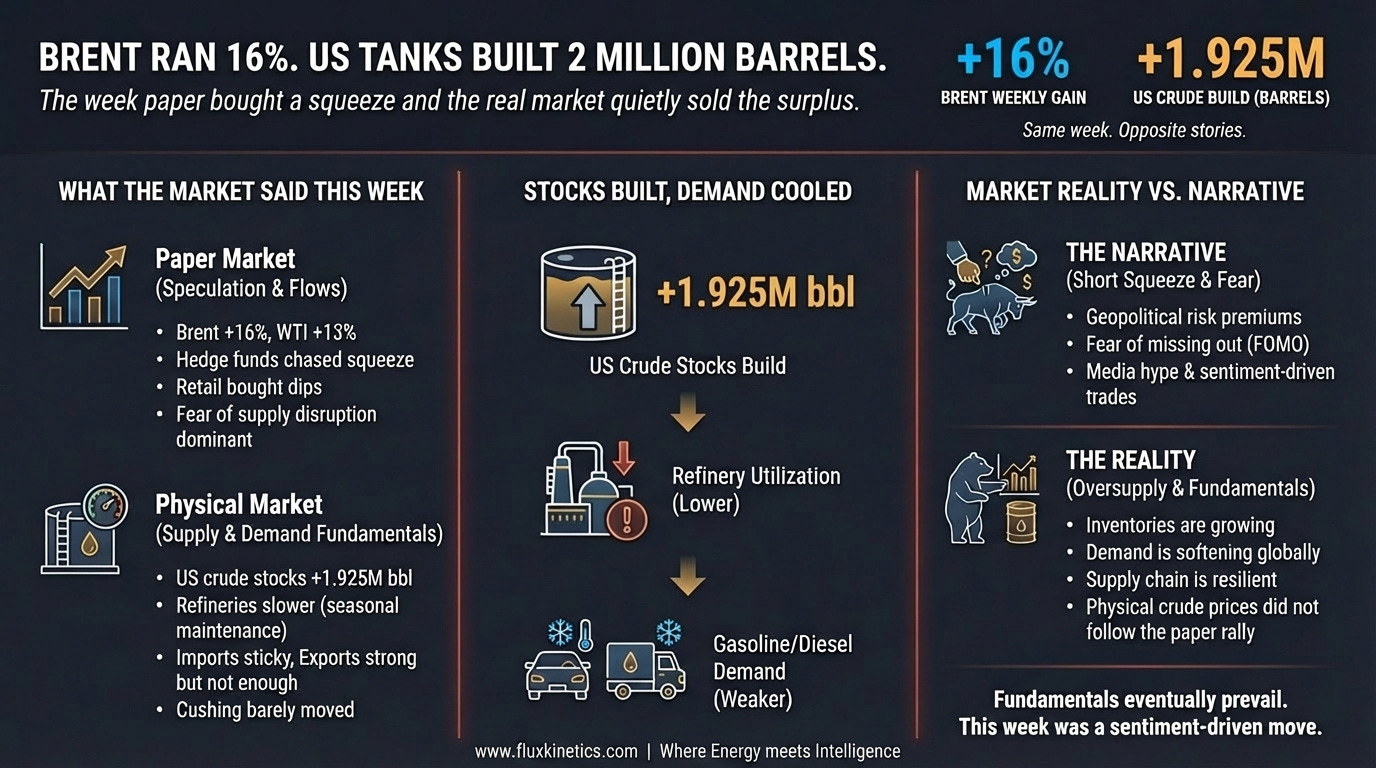

The week paper bought a squeeze and the real market quietly sold the surplus.

Dear Executives, Traders & Investors, Brilliant minds and Friends

The week opened with a tanker called Al-Qaiyyah pulling into Sabine Pass, Texas, on Monday morning. It closed with Brent crude posting a 16% weekly gain that nobody actually wanted to hold beyond the next month. In between, the US government’s energy agency reported that American crude oil stockpiles went up by nearly 2 million barrels when the market expected them to go down. Tanker traffic through the world’s most important oil shipping route stayed near zero for most of the week. US natural gas storage filled up by 103 billion cubic feet, leaving stocks well above the five-year average. Brent closed Friday at $105.33. Natural gas at the main US hub sank to $2.61. Gold gave back to $4,714. Lithium quietly hit a three-month high in China.

Quick word for newer readers. Brent and WTI are the two main oil benchmarks. Brent is the global one. WTI is the US one. Henry Hub is where US natural gas gets priced. When I say “the curve,” I just mean the line of futures prices for delivery in different months. Front month is next-up delivery. Back of the curve is delivery a year or more out.

The story coming into the week was simple. Supply disruption equals higher oil prices for the rest of 2026. Stocks priced it. Hedge funds chased it. Retail bought every pullback. Then Wednesday’s inventory report landed and the script started cracking. Crude built when it was supposed to draw. Refineries ran a touch slower. The big US oil hub barely moved.

In case you’ve missed my previous article, Nuclear - Small Modular Reactor (SMR):

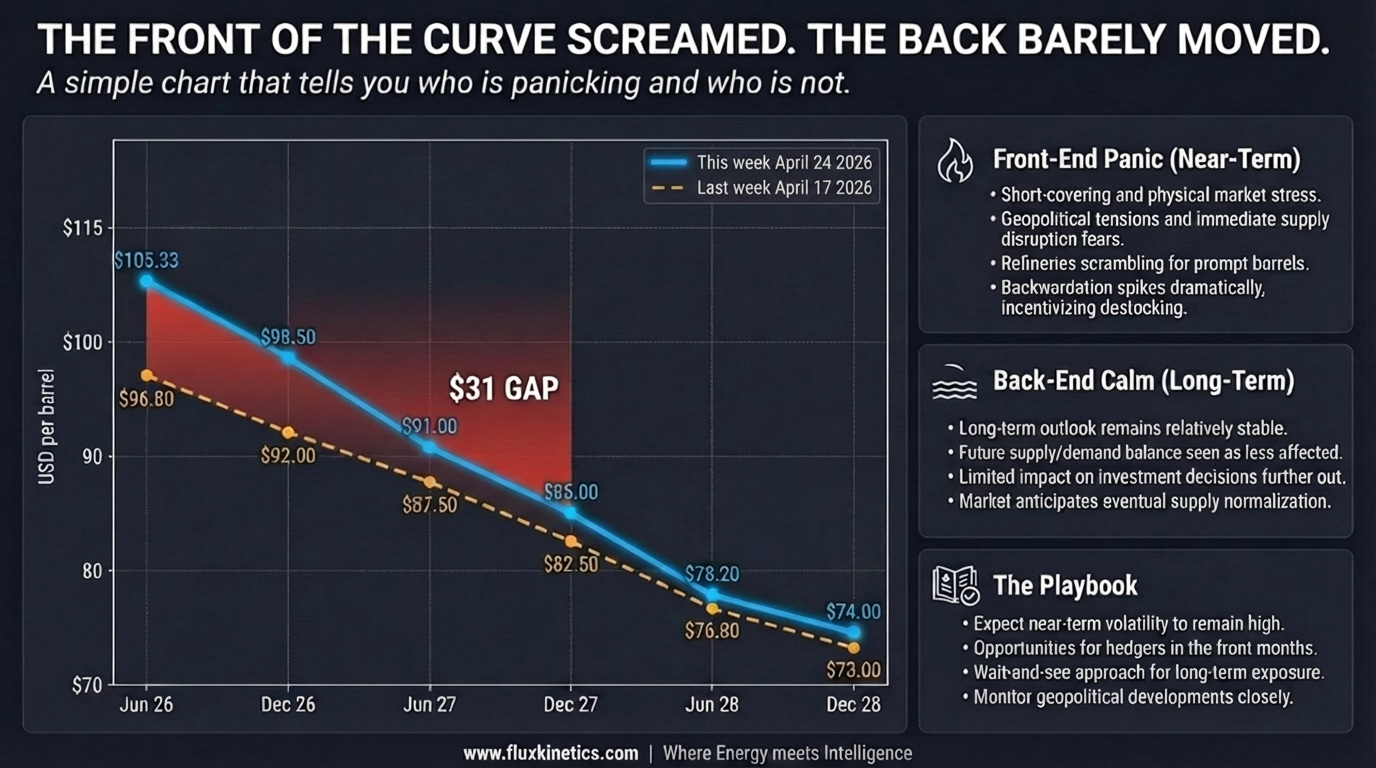

Here is what I think almost everyone missed this week. Brent ran 16% on a curve that is already telling you the back end does not believe the front. Prices for delivery in late 2027 barely moved. That is not a long-term shortage. That is a short-term bottleneck with an expiration date.

This Week’s Settle

Brent (June ‘26): $100, sharply higher, +16% on the week, as Gulf tanker traffic stayed near zero for most of the week and prices repriced for cargoes that simply could not get out of the region.

WTI (June ‘26): $96, sharply higher, +13% on the week, lagging Brent on a wider gap as US crude stockpiles built nearly 2 million barrels against an expected draw.

Henry Hub (May ‘26): $2.61/MMBtu, sharply lower, off roughly 11% on the week, as the storage report showed a heavy injection that pushed gas inventories well above seasonal norms even with Golden Pass starting to pull gas for export.

Gold (June ‘26): $4,700 settle, fractionally softer, down roughly 1% on the week, as a stronger dollar and softer safe-haven buying drained the panic premium that had built earlier in April. FED rate decision ahead.

Silver (spot): $75, flat to fractionally higher, holding the week’s range as industrial demand from solar and grid build kept the floor intact while gold’s pullback capped the upside.

Lithium carbonate (battery grade, China): 173,000 yuan per tonne (~$23,800/tonne), higher, +13.4% on the month and at a three-month peak, as Chinese battery makers pulled forward summer buying on tighter raw material supply and fresh EV subsidy guidance.

Brief Contents

The Oil and Curve Story

The LNG and Golden Pass Story

The Metals and Critical Minerals Story

Chokepoints and Capital Flows

Week Ahead: What to Watch

Action Items

THE OIL AND CURVE STORY

Brent ran 16% on the week. WTI ran 13%. The gap between the two widened. None of that is the real story I am tracking. The story is what the rest of the curve did while the front month was throwing a parade.

A simple way to read the curve.

When today’s price is much higher than the price one or two years out, the market is telling you “right now is tight, but I expect things to normalise.”

Traders call that backwardation. When today’s price is lower than the future, that is contango, and it means today is well-supplied.

Front-month Brent at $105 with December ‘27 trading near $74 is not a normal market. It is a curve telling me the physical bottleneck is real, but it is also telling me that the moment cargoes start moving again, the back end is where the truth lives. I saw heavy producer hedging in the 2027 strip this week.

Refiners locked in their margins where they could. The smart money is not buying the spike. The smart money is selling it forward.

Then Wednesday hit. The US energy agency reported commercial crude stocks of 465.7 million barrels for the week ending April 17, a build of nearly 2 million versus a consensus draw of 1.2 million. Refinery activity slipped slightly. Imports stayed sticky. The market is drowning in domestic supply.

The Flux Kinetics Number: nearly 2 million barrels. That is the print that contradicts every “squeeze” headline you read this week… with cargoes throttled overseas and Brent at $105, US tanks should have been bleeding.

They built. The split is this. The Atlantic side of the world is short barrels on water. The US Gulf is long crude it cannot place fast enough into a refining system still working through spring maintenance.

The Baker Hughes rig count showed US drillers added one rig on Friday, bringing the total to 544. Oil rigs actually dropped by three to 407. Gas rigs picked up four. The drilling response to $96 WTI is not “drill baby drill.” It is “we already learned that lesson in 2014 and again in 2020.”

🔁 Found this useful?

Flux Kinetics runs on word of mouth. If this note sharpened how you see the week, one forward to the right person is worth more than any algorithm.

📨 Share this issue

The OPEC+ production hike of 206 thousand barrels per day announced earlier this month is still theoretical. You cannot ship more oil through a route you cannot use.

“The front month is pricing a war. The back of the curve is pricing the cleanup.”

THE LNG AND GOLDEN PASS STORY

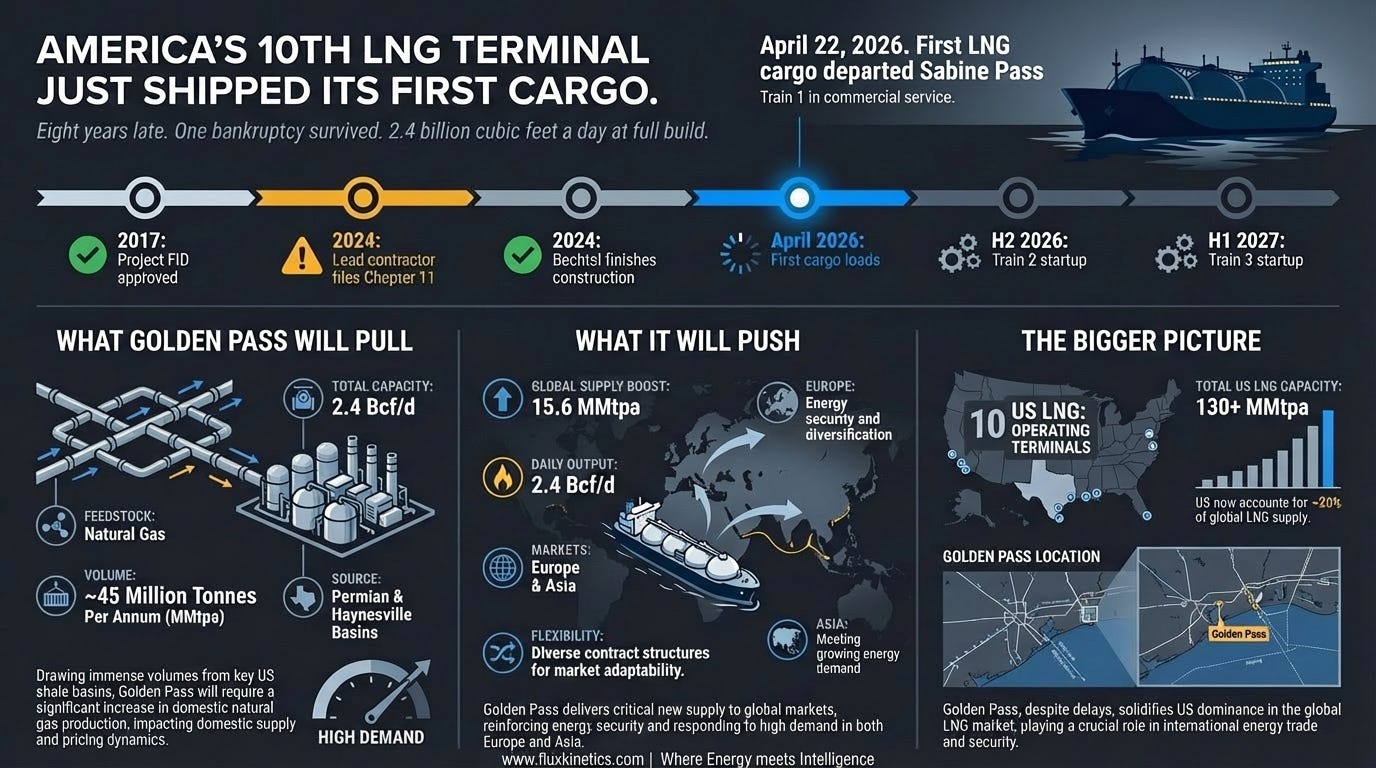

Monday at Sabine Pass, the Al-Qaiyyah pulled alongside Berth 1 at Golden Pass. Wednesday it loaded. Thursday it left. The 10th US LNG export terminal is now in commercial service, eight years after the project was approved, after a contractor went bankrupt and nearly killed the project, after Zachry Holdings filed Chapter 11 in 2024 and Bechtel had to be parachuted in to finish the job.

For readers new to LNG, natural gas gets cooled to liquid at -160 degrees C so it can be loaded onto specialised ships and sent across the ocean. That is what makes Henry Hub gas in Texas useful to a buyer in Tokyo or Madrid. Train 1 at Golden Pass can produce around 5.2 million tonnes per year, roughly 700 million cubic feet of gas per day once at full ramp. Train 2 is targeting startup later this year. Train 3 in early 2027. At full build, Golden Pass will pull about 2.4 billion cubic feet of US gas out of the country every single day.

Henry Hub closed Friday at $2.61. Storage built 103 billion cubic feet. Stocks now sit well above the five-year average. This is the gap I keep coming back to. Domestic gas is in surplus. Export capacity is coming online. The two facts cannot coexist for long.

The Flux Kinetics Insider View. I spoke with two midstream operators on the Gulf Coast this week. Both confirmed that pipeline volumes flowing into Sabine Pass climbed steadily through April. Both expect the price gap between US gas and Asian gas to narrow on the front of the curve, then widen on the back as Train 2 starts up in Q3. Equities figured this out in 2024. The futures contract is just starting to price it.

“Storage is well above the five-year average. Golden Pass just opened the drain.”

THE METALS AND CRITICAL MINERALS STORY

Gold faded into Friday’s close. Spot near $4,719, June futures at $4,722.30. The dollar firmed. The panic bid that ran gold from $4,200 to nearly $4,800 earlier in April leaked out as the safe-haven premium compressed. Silver held $75 through choppy two-way action. The gold-to-silver ratio sits near 62, well below the decade average of 80, telling me industrial silver demand from solar panels and electronics is doing real structural work that pure monetary gold is not.

Lithium is the story almost no one is writing about this week. Battery-grade lithium carbonate in China hit 173,000 yuan per tonne, a three-month high, up 13.4% in 30 days, up 147% from this time last year. The driver is not headline EV sales. It is Chinese battery makers buying ahead of expected tightness in spodumene (the rock lithium gets mined from), where two mid-tier Australian producers cut their output guidance this month… plus a quiet but real shift in grid storage orders out of Saudi Arabia and Texas.

I spoke with two procurement heads at major battery cell manufacturers this week. Both said the same thing in different words. Spot prices no longer set the marginal cost. Long-term contracts do, they are repricing fast.

📬 Never miss a signal

If this is your first time reading Flux Kinetics, every weekly note lands free in your inbox. No noise, no filler, just what actually moved the tape.

The Flux Kinetics Trade :

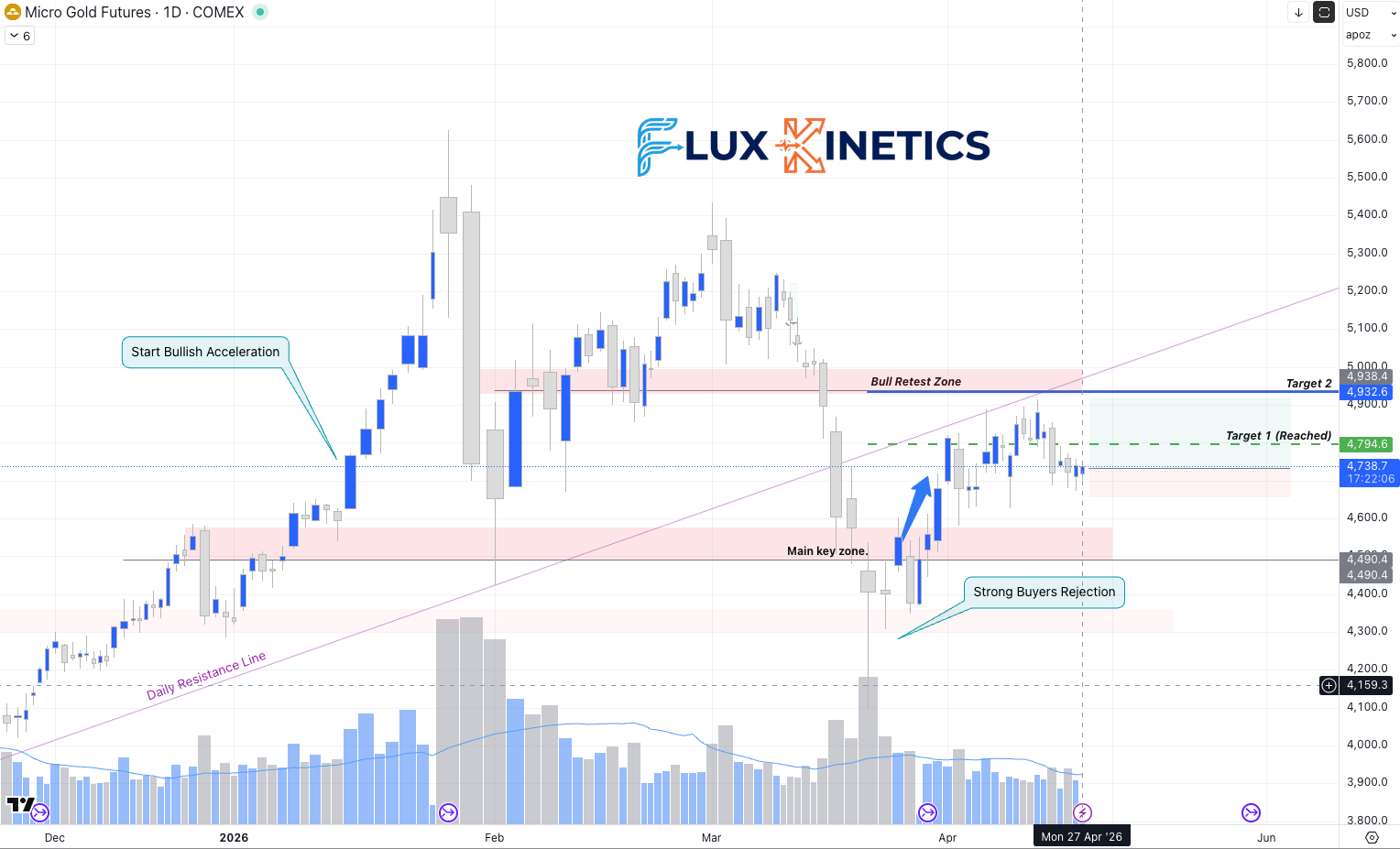

As I scenario-predicted last week, for gold, we came back to retest the 4,700 support zone, which can be an entry price as highlighted previously and while it holds. Gold now sits in a short term corrective phase.

This week, the most important information related to gold is the Fed rate-cut decision, which will influence the dollar direction, therefore the gold one...

The play → I am watching is a long re-entry only on an hourly close back above $4,710, targeting $4,900, with invalidation at a daily close below $4,660. That is roughly 3:1 RR.

I would recommend not keeping any position on Wednesday, when the Fed will announce their decision, as the market will be extremely volatile on this day. Be safe, and always remember “capital to be protected as first”

CHOKEPOINTS AND CAPITAL FLOWS

The Gulf shipping corridor is the chokepoint of the year, and this week it was the chokepoint of the week. Three tanker passes in twenty-four hours on Tuesday. A brief reopening on Saturday. Closure again the following day. Baker Hughes told its earnings call on Thursday that its 2026 financial guidance now assumes the route does not fully reopen until the second half of 2026. That is a service-company CFO telling you the rerouting math is not a one-week problem. It is a six-month problem at minimum.

Roughly 17 million barrels per day of crude moves through this corridor in normal times. The physical alternatives are limited. The East-West pipeline from Saudi Arabia to the Red Sea moves about 5 million barrels per day, only partially used. The Habshan-Fujairah pipeline from the UAE adds another 1.5 million barrels per day.

That leaves roughly 10 million barrels per day with no bypass.

Capital is moving to the bypass-adjacent. Saudi Aramco was reportedly accelerating East-West pipeline expansion engineering this week. UAE-flagged tankers were repositioned to load at Fujairah. Floating storage off Singapore climbed.

The split is this. The paper market is buying the squeeze on Brent. The physical market is buying pipeline expansion engineering, port slot reservations, and West African and Brazilian crude. Don’t confuse the freight spike with the cycle.

“If you trade the headline, you feed the pros. If you trade the pipe, you front-run them.”

WEEK AHEAD: WHAT TO WATCH

Wednesday, April 29: FED Rate Decision + US weekly oil inventory report. The market is now expecting a draw of around 800 thousand barrels after this week’s surprise build. Would the FED cut its rate ?

Thursday, April 30: US weekly natural gas storage report. I am watching for an injection in the 90 to 105 billion cubic feet range.

Sunday, May 3: OPEC+ ministerial meeting. Compliance review and the May quota implementation. I will be watching for any “softening in language.”"

Action Items

For Traders. Very volatile week: Geopolitical, FED decision and major earning. Meaning, tighten your stop and avoid overnight position.

For Operators. Pull forward Gulf Coast refinery maintenance scheduling while shipping rates are still favorable. Lock in 2026 second-half LNG tanker charter rates now before Golden Pass Train 2 demand hits. or commissioning teams on Train 2 at Golden Pass, expect Bechtel to pull labor from Train 3 as Train 1 stabilises…

For Investors. Buy the builders. Engineering and construction firms, and pipeline operators with Golden Pass exposure, are the live trade I am tracking. Avoid the front-month commodity ETFs trapped between a paper premium and a domestic glut…it’s time be specific on your selection.

If this changed how you see the week, send it to one person who needs to see it too.

⚡ One last thing

If this changed how you see the week, send it to one person who needs to see it too. That is how Flux Kinetics grows. Reader by reader, not algorithm by algorithm.

📨 Share • 📬 Subscribe • 💬 Leave a comment

Coming next:

The Gold To Silver Ratio As A Stress Gauge For The Energy Transition

Flux Kinetics - Where Energy Meets Intelligence.

Wassim CHIADLI

This content is for educational purposes only and does not constitute financial, legal, or tax advice. All opinions and analyses are my own, and any actions you take are at your own risk after consulting an appropriate professional.

Bought gold a 4712… thanks for the play, let’s see if it works

LNG export is good news for the US … while the straight of Hormuz is still not fully open